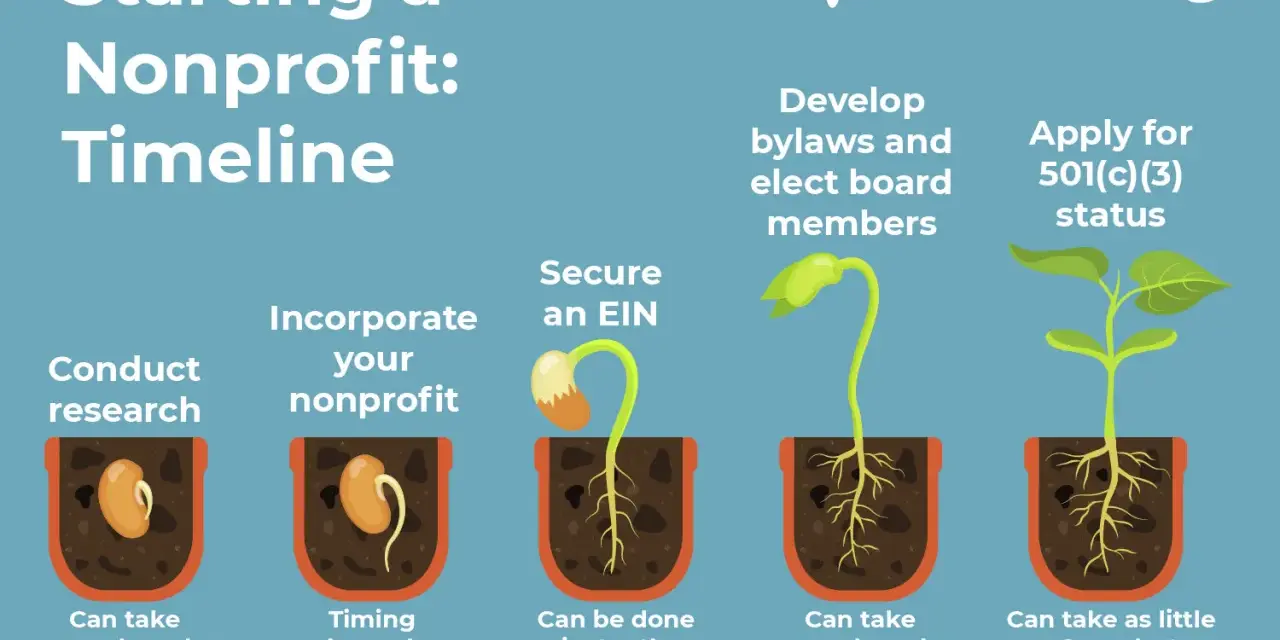

Setting up a nonprofit in the United States is really a sequence of decisions, not a single form. To set up a nonprofit well, I treat it as three layers: the state entity, the federal tax status, and the operating system that keeps both of them compliant. In this guide, I walk through the steps, the usual timing, the real costs, and the operational details that matter after the paperwork is filed.

The first year is mostly about getting the structure right

- A nonprofit corporation is not the same thing as tax-exempt status. You usually need both the state entity and the IRS approval.

- The mission should drive the structure. A charity, an advocacy group, and a membership organization do not always fit the same tax category.

- Do not apply for an EIN until the organization is legally formed. That sequence matters with the IRS.

- The current IRS user fees are $600 for Form 1023 and $275 for Form 1023-EZ, and the application is filed electronically.

- Annual compliance is not optional. Most organizations must file a 990-series return or notice and keep clean internal records.

Choose the right nonprofit structure before you file

When I help founders think this through, I start with the activity, not the paperwork. The legal shell, the tax status, and the fundraising model need to fit each other. If they do not, the organization can end up with a mission that sounds good on paper but is awkward to govern, fund, or defend later.

| Structure | What it is | Best for | Main tradeoff |

|---|---|---|---|

| State nonprofit corporation | A legal entity formed under state law | Most mission-driven organizations that want a formal board and clear governance | It does not automatically create federal tax exemption |

| 501(c)(3) | IRS tax-exempt status for charitable, educational, religious, scientific, and similar purposes | Public charities, schools, relief organizations, arts groups, and grant-seeking programs | Lobbying and political activity are limited, and private benefit is tightly restricted |

| 501(c)(4) | IRS status for social welfare organizations | Advocacy-heavy groups and policy organizations | Donations are usually not deductible, which can make fundraising harder |

The practical takeaway is simple: if you want deductible donations, foundation support, and a charity-style public mission, 501(c)(3) is usually the default. If advocacy is central to the work, I would look carefully at whether a different tax status, or a separate affiliate, makes more sense. Once that choice is clear, the state filing becomes much easier to shape.

File the state entity and lock in the founding documents

This is the part where many founders move too fast. The state filing is not just administrative; it is the document set that tells regulators, banks, donors, and future board members what the organization actually is. I would not improvise here.

- Check the name and reserve it if your state allows it. You want a name that is available, distinguishable, and easy to use consistently on filings, banking documents, and donor materials.

- Write a purpose clause that matches the mission. If you plan to pursue 501(c)(3) status, the organizing language must point to exempt purposes, not a vague commercial idea dressed up as a cause.

- Include a dissolution clause. If the organization ever closes, remaining assets should go to another qualified nonprofit or a government entity, not to insiders.

- Appoint a registered agent and initial directors. This gives the state and the IRS a real point of contact and establishes who has authority at the start.

- Adopt bylaws and conflict rules at the first meeting. Bylaws explain how the board works, how officers are chosen, and how decisions are approved. A conflict-of-interest policy keeps the mission from drifting into private benefit.

Some states also ask for additional language, signatures, or publication steps, so I always check the state-specific filing instructions before submitting. Once the entity exists, the next step is getting the federal tax pieces in the right order.

Get your EIN and IRS exemption in the right order

Do not apply for an EIN before the organization is legally formed. The IRS is explicit about that sequence. Form the entity first, then apply for the EIN, then move to the tax-exemption application. That order keeps the record clean and avoids preventable delays.

| IRS form | When it fits | Current user fee | What to expect |

|---|---|---|---|

| Form 1023 | Most organizations that need full 501(c)(3) recognition or have more complex facts | $600 | More detail, more attachments, and usually a slower review, but it gives you more room to explain the organization |

| Form 1023-EZ | Only organizations that meet the eligibility rules for the streamlined filing | $275 | Faster and lighter, but not available to everyone and not ideal if your model is unusual or nuanced |

The IRS expects the exemption application to be filed electronically on Pay.gov. I would also expect the form to ask for your organizing documents, a mission narrative, budget information, and details about governance and compensation. That is not busywork; it is how the IRS checks whether the entity is organized and operated for exempt purposes.

For a straightforward organization, the EIN may be issued quickly and the exemption filing can move in weeks or a few months. The more unusual the mission, the more helpful a full explanation becomes. That is why the next step is not fundraising, it is governance.

Build the governance and money controls before the first donation

I see this mistake constantly: a founder gets excited about the mission, launches a donation page, and only later discovers that there is no real operating system behind the money. That is a bad way to start. The board, the controls, and the records are what make the organization trustworthy.

Give the board real work

The board should not be decorative. It should approve the budget, oversee the executive, review the mission, and make sure the organization is not drifting into private benefit. I like to see clear officer roles, defined voting rules, and a board calendar that forces regular review rather than crisis-driven decisions.

Separate money immediately

Open a bank account in the organization’s name as soon as the legal entity and EIN are ready. Do not let program money sit in a personal account. Set up accounting software, choose a chart of accounts, and decide in advance who can approve payments, reimbursements, and transfers. A simple dual-approval rule is often enough at the start.

Read Also: Nonprofit Press Release - Get Media Coverage That Matters

Keep the records that matter later

- Signed bylaws and board resolutions

- Conflict-of-interest disclosures

- Meeting minutes and written consents

- Donation records and restriction tracking

- Payroll files if you hire staff

- Grant agreements and reporting deadlines

One operational rule I never skip: every restricted dollar should be tracked separately from unrestricted operating money. If a donor gives for a specific program, that restriction needs to be visible in the books. Once those controls are in place, fundraising becomes safer and the annual filings become much easier to survive.

Plan for fundraising, state registrations, and tax filings from day one

Fundraising is where the nonprofit stops looking like a concept and starts behaving like a regulated organization. The IRS rules matter, but state charitable solicitation rules matter too, and those state rules vary. If you are asking for donations across state lines, I would not assume your home-state approval is enough.

| Compliance item | What it means in practice | Why it matters |

|---|---|---|

| Charitable solicitation registration | Some states require registration before you solicit donations there | Missing it can create fines, delays, or a forced pause on fundraising |

| Annual IRS return | Most exempt organizations file Form 990, 990-EZ, or 990-N | The return is due on the 15th day of the 5th month after the fiscal year ends |

| Unrelated business income | If the organization has $1,000 or more of gross income from an unrelated business, it must file Form 990-T | Tax-exempt status does not shelter unrelated commercial activity |

| Public disclosure | The exemption application and annual return are generally public | You should write everything as if a donor, reporter, or grantmaker may read it |

On the filing side, smaller organizations generally may use Form 990-N if gross receipts are normally $50,000 or less, while many larger organizations file Form 990-EZ or Form 990. The right form depends on financial activity and eligibility, so I always map the reporting threshold early instead of waiting for year-end. That calendar discipline also helps when staff and volunteers start handling reimbursements, event revenue, and grant draws.

One more practical point: if you plan to run a telefundraising campaign or use outside vendors, review the rules carefully before the campaign starts, not after it goes live. That is the difference between a controlled launch and a compliance clean-up. From there, the last thing to budget is the startup itself.

Budget the launch realistically and avoid the mistakes that waste months

The cost to get started is usually lower than people fear, but the expensive part is bad sequencing. A clean filing is cheaper than a correction. A good board packet is cheaper than a governance dispute. And a proper exemption application is cheaper than a rejected or incomplete one.

| Cost item | Typical range | What drives it |

|---|---|---|

| State formation fee | $25 to $300+ | Varies by state and filing method |

| Registered agent service | $100 to $300 per year | Useful if you do not want a founder’s home address on record |

| IRS exemption fee | $275 or $600 | Depends on whether the organization qualifies for Form 1023-EZ |

| Legal drafting or review | $500 to $5,000+ | Complexity of the mission, governance, and state requirements |

| Accounting setup and bookkeeping software | $300 to $2,000+ | Chart of accounts, payroll setup, and reporting structure |

| Insurance | $500 to $2,500+ | Depends on staff, volunteers, events, and risk exposure |

For a simple volunteer-led organization, the first year can stay relatively lean. Once you add staff, insurance, outside fundraising, or legal review, the budget rises quickly. I usually tell founders to plan for a few months of setup time and a real operating reserve before they promise anything public.

The mistakes that cost the most are predictable: vague purpose language, filing the EIN too early, mixing personal and organizational money, choosing the wrong tax status for an advocacy-heavy mission, and ignoring state fundraising rules. If you avoid those, the launch is usually smoother than people expect. The final step is turning the organization into something that can run without constant founder intervention.

What I would lock in during the first 90 days

If I were starting a nonprofit today, I would spend the first 90 days making the organization legible, fundable, and auditable. That means anyone who looks at it later should be able to understand who controls it, how money moves, what it does, and how it stays compliant.

- Days 1 to 30: finalize the board, adopt bylaws, open the bank account, set up bookkeeping, and confirm the budget.

- Days 31 to 60: file the IRS exemption application, complete any state charitable registrations, and prepare donor acknowledgment language.

- Days 61 to 90: build the compliance calendar, set up document storage, review insurance, and map the first annual reporting deadlines.

The real test is not whether the nonprofit exists on paper. It is whether the organization can accept money, document decisions, and keep operating without improvising its way through every obligation. If you get the legal setup and the operational controls right early, the mission has room to grow instead of constantly backtracking to fix avoidable mistakes.