A foundation endowment is not just a pool of invested assets; it is the engine that lets a nonprofit plan beyond the next grant cycle. The real work is in preserving capital, setting a defensible spending rule, and keeping the board aligned when markets move or cash needs change. This article breaks down the legal guardrails, governance choices, and operating habits that make long-term support durable.

What matters most before the board commits capital

- An endowment is meant to support mission work over many years, not to function as day-to-day cash.

- Boards need a written spending policy, an investment policy, and a clear rule for who approves exceptions.

- Private foundations face a different federal framework than public charities, including payout and excise-tax rules.

- A strong policy balances three pressures at once: mission spending, inflation protection, and liquidity.

- The biggest failures usually come from weak governance, not from a single bad market year.

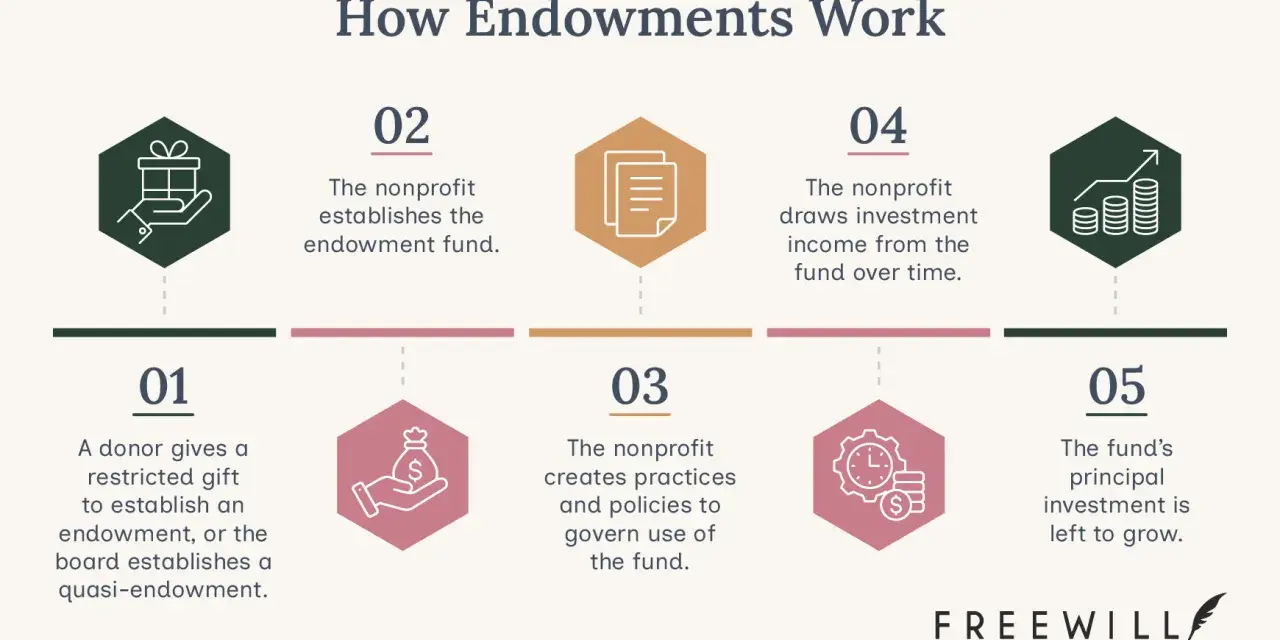

What an endowment actually does for a foundation

I think the cleanest way to understand an endowment is to treat it as permanent or long-horizon capital with a rule for how much can be used each year. The principal is invested, a portion of the return is spent, and the rest stays in place so the fund can keep supporting the mission over time. That is very different from simply parking surplus cash in an account and hoping it lasts.

For a foundation, the practical question is not whether money is set aside. It is whether the money is governed well enough to survive downturns, inflation, and shifting program demand. I usually separate four buckets in conversations with boards:

| Bucket | Main purpose | Liquidity | Who typically controls it |

|---|---|---|---|

| Permanent endowment | Long-term mission support with principal preservation expectations | Low to medium | Donor restrictions and board policy |

| Quasi-endowment | Board-designated long-term support | Medium | Board, because it can redesignate funds |

| Operating reserve | Rainy-day buffer for disruptions or timing gaps | High | Board and management, under reserve policy |

| Working cash | Payroll, bills, and routine operations | Very high | Management, with board oversight |

That distinction matters because too many organizations call every surplus dollar “endowment” and then wonder why the balance sheet feels tight. An endowment should create discipline and continuity, not confusion. Once that distinction is clear, the next issue is the legal framework that decides how much can be spent and how the board must account for it.

How U.S. rules shape spending and oversight

In the United States, the rules depend on the type of organization. For private foundations, the IRS generally requires a minimum investment return of 5 percent of the relevant asset base, and the foundation must file Form 990-PF each year. Those organizations also live with excise-tax rules on net investment income and prohibited transactions, so governance is not optional paperwork; it is part of the asset strategy.

That is why I tell boards to think in terms of compliance plus stewardship. A private foundation cannot treat its investment pool as a personal portfolio with charitable branding. Self-dealing, excess business holdings, jeopardizing investments, and taxable expenditures all sit in the background as real risks, not theoretical ones. If the fund is structured as a private operating foundation, the spending mechanics can differ again, because the foundation must actively carry out its exempt work and satisfy separate operating tests.

Public charities and many donor-restricted charitable funds operate under a different legal lane. In many states, UPMIFA gives boards a prudence framework for investing and spending endowed funds. The board is expected to weigh the purpose of the fund, economic conditions, the duration of the fund, expected total return, and the organization’s other resources before appropriating money for spending.

That legal split creates a very different operational posture. A private foundation often starts with a federal payout requirement. A public charity usually starts with donor intent, state law, and board judgment. Both can support long-term mission work, but they are not governed the same way, and conflating them is where many organizations get sloppy. The next step is translating those rules into written controls the board can actually live with.

What the board should put in writing before the first dollar is invested

If I were building a new fund from scratch, I would not begin with asset selection. I would begin with the documents that define behavior when conditions get messy. A strong investment policy statement and a matching spending policy do more to protect an endowment than almost any “smart” market call.

- Investment objective - Is the priority capital preservation, real growth, mission spending, or a blend of the three?

- Spending formula - Will distributions be based on a rolling average, a fixed percentage, or board discretion?

- Risk tolerance - How much volatility can the organization accept without threatening operations?

- Asset allocation bands - What mix of equities, fixed income, and alternatives is allowed?

- Liquidity rules - How much must stay accessible for grants, operating needs, or downturns?

- Delegation and oversight - Who monitors performance, rebalances, and reports to the board?

- Exception authority - When can the board override the normal spending rule, and how is that documented?

I also recommend written language for donor restrictions, because vague intent becomes expensive later. If a contribution is meant for a named purpose, a specific time horizon, or a program that may change over time, that should be captured up front. A well-drafted policy does not eliminate judgment; it makes judgment auditable. From there, the real challenge is deciding how much to spend without eroding the fund’s future purchasing power.

How to set a spending rule that still protects purchasing power

A spending rule should answer one basic question: how much can be used this year without forcing the next board to start over? That sounds simple until market values swing, inflation rises, and program demand increases at the same time. A sensible rule has to be boring in good years and resilient in bad ones.

As a practical benchmark, I see boards start around a 4 percent to 5 percent spending range, usually applied to a smoothed market value rather than a single year-end snapshot. NACUBO’s endowment example uses a 4 percent spending rate, which is a useful anchor because it forces the board to connect spending to long-term return expectations instead of short-term optimism.

- Estimate the annual mission commitment the fund is expected to support.

- Choose a smoothing method, such as a multi-quarter or multi-year average.

- Test the rule against a down market, not just a normal year.

- Build in an underwater policy so the board knows what happens if value falls below prior levels.

- Revisit the rule at least annually, even if you do not change it.

The most common mistake here is spending based on paper gains that have not been stress-tested. Another is pretending inflation is someone else’s problem. If the fund spends 5 percent but the portfolio only earns 3 percent after fees over time, the organization is slowly liquidating itself. The spending policy has to be tied to a realistic return assumption, not a hopeful one. That is also why the operational mistakes matter so much.

The mistakes that quietly damage long-term support

When an endowment underperforms, the cause is often less dramatic than people expect. I usually find one of five issues underneath the surface:

- Confusing endowment with reserve money - This creates bad liquidity decisions and weak board discipline.

- Overloading the portfolio with illiquid assets - Private equity, private credit, or real estate can work, but only if the board can tolerate slower access to cash.

- Skipping rebalancing - A portfolio that drifts too far from policy can take on more risk than the board intended.

- Using the fund to patch recurring operating deficits - That may solve one year and weaken the next five.

- Failing to document donor intent and board action - This becomes a reporting and governance problem fast.

I also watch for a subtler problem: boards that celebrate asset growth but ignore distribution quality. A fund can look healthy on paper while still producing erratic support for programs. If grantmaking or program delivery depends on predictable annual draws, the board needs to measure stability, not just return. Once those errors are visible, the final question is what to put in place if the fund is still being built.

What I would build first if the fund is starting now

If an organization is early in the process, I would build the operating system before I scale the assets. The first version does not need to be fancy. It needs to be clear, repeatable, and defensible under board scrutiny.

- A one-page purpose statement that says exactly what the fund is meant to support.

- A board resolution that authorizes the fund and names the decision makers.

- An investment policy statement with target ranges, benchmarks, and review dates.

- A spending policy that explains the formula, the smoothing period, and the exception process.

- A quarterly dashboard that shows market value, spending, fees, liquidity, and variance from policy.

The organizations that do this well usually have one thing in common: they treat the endowment as a governed asset, not a symbol of maturity. That mindset keeps the fund useful when markets wobble and keeps the board from improvising under pressure. If you want long-term support to stay credible, the policy architecture has to be as strong as the portfolio itself.