Compliance only works when it survives contact with real operations. In practice, that means policies, controls, training, monitoring, and remediation stay active after launch, not just during an audit. I treat ongoing compliance as the discipline of keeping those controls current as laws, vendors, systems, and business models change.

What matters most when compliance has to last

- Think in terms of a control system, not a binder of policies.

- Owners, cadence, and evidence matter as much as the rule itself.

- Third-party risk and change management are where many programs drift.

- Regulators care about monitoring, testing, and timely remediation.

- The strongest programs are built to absorb change without losing traceability.

What compliance over time actually means

I think of compliance as a lifecycle. A company can file the right forms, publish the right policy, or pass a first review and still fall out of step three months later if no one owns updates. In the U.S., that risk looks different for a public company, a bank, a nonprofit, and a private operating business, but the pattern is the same: the obligation does not stop once the document is signed.

A living program does four things well: it maps obligations, turns them into controls, tests those controls, and updates them when something changes. In regulated teams, people often call this a CMS, short for compliance management system, but the label matters less than the operating reality. I want a program that can prove what it knows, what it tested, what it fixed, and what still needs attention.

That is why I prefer to talk about compliance as a managed process rather than a one-time event. Once you accept that, the next question is what the program should actually contain.

The control elements I expect to see

Across mature U.S. programs, I keep seeing the same control layers. They are not fancy, but they are durable when they are owned and tested.

| Control area | What it should do | How often I would review it |

|---|---|---|

| Board and management oversight | Set tone, approve priorities, and review exceptions | Quarterly |

| Policies and procedures | Translate legal obligations into day-to-day instructions | At least annually, and whenever rules or operations change |

| Training | Make requirements real for the people doing the work | Onboarding plus annual refreshers |

| Monitoring and testing | Check whether the controls are actually working | Monthly or quarterly, depending on risk |

| Issue management and remediation | Assign an owner, a due date, and proof of fix | Ongoing, with aging reviewed regularly |

| Third-party oversight | Keep vendors, agents, and contractors inside the risk picture | At onboarding and at periodic intervals |

If one of these layers is missing, the program may look complete on paper but feel brittle in practice. Third-party oversight deserves special attention because external partners often expand risk faster than internal teams notice. I want to see due diligence, contract language, monitoring, and periodic recertification or review where the exposure justifies it.

That leads straight to the practical question: how do you turn these layers into a rhythm that people can actually follow?

How I would build the operating rhythm

If I were setting up the program from scratch, I would start with a plain-language obligations map. List every rule, contract clause, license, filing, or internal standard that matters; assign one owner to each item; and give it a review cadence. The point is not to create more paperwork. The point is to make drift visible before it becomes a finding.

Read Also: KYC Onboarding - Build Defensible Identity Verification

A cadence that works in practice

- Weekly: exception reviews, incident follow-up, access checks, or transaction alerts.

- Monthly: control testing, issue aging, license tracking, and vendor checkpoints.

- Quarterly: leadership reporting, risk refreshes, and a review of open remediation items.

- Annually: full risk assessment, policy review, training refresh, and control redesign if needed.

I also keep evidence simple. If a reviewer cannot see who did what, when they did it, and what changed afterward, the control is weaker than it looks. A shared repository, a dated issue log, and a short escalation path usually work better than a pile of disconnected PDFs.

Good rhythm matters because the most common failures are not dramatic scandals. They are slow slippage and delayed correction.

The mistakes that break programs fastest

The weakest programs usually fail for ordinary reasons, not exotic ones. I see the same patterns again and again.

- Treating compliance as an annual clean-up rather than a routine operating task.

- Using generic policies that do not match the company’s actual workflows.

- Ignoring state, local, or sector-specific filings until a deadline is already missed.

- Leaving vendors outside the scope even when they handle sensitive data, payments, or regulated activity.

- Closing issues without root-cause analysis, which lets the same failure come back in a different form.

- Reporting metrics that look tidy but do not reveal risk, such as completion counts with no aging or exception detail.

The cost is not limited to fines. Weak controls can delay financing, slow acquisitions, complicate audits, trigger customer loss, or force management to spend time explaining problems instead of running the business. Once that happens, the question is no longer whether the company has a policy. The question is whether the policy changed behavior.

That is also why the same compliance model does not fit every organization.

How the requirements change by business type

The framework is similar across industries, but the pressure points are not. A public company, a nonprofit, and a private operating business all face different calendars and different failure modes.

| Business type | Main pressure points | Practical focus |

|---|---|---|

| Public company | Disclosure controls, insider access, audit committee reporting | Quarterly close discipline, material issue escalation, document retention |

| Financial institution or fintech | Consumer compliance, transaction monitoring, vendor and model risk | Testing, complaints, third-party oversight, rapid remediation |

| Nonprofit | Tax-exempt status, public disclosure, employment tax, donor records | Filing calendars, governance minutes, public document management |

| Private operating company | Entity filings, licenses, employment rules, privacy, contracts | Calendar control, owner accountability, and a clean issue log |

The wrong move is copying a template from another sector. A California employer and a Texas manufacturer will not share the same exact obligations, and a vendor-heavy business will have a very different risk profile than a company that performs everything in-house. The right framework is the one that matches the company’s actual footprint.

Once the program is tailored, I want proof that it is producing useful information instead of just busywork.

How to tell whether the program is actually working

I look for evidence that the program finds issues early and closes them cleanly. If most problems are discovered by external auditors, customers, or regulators, the internal monitoring loop is too weak.

These are the signals I pay most attention to:

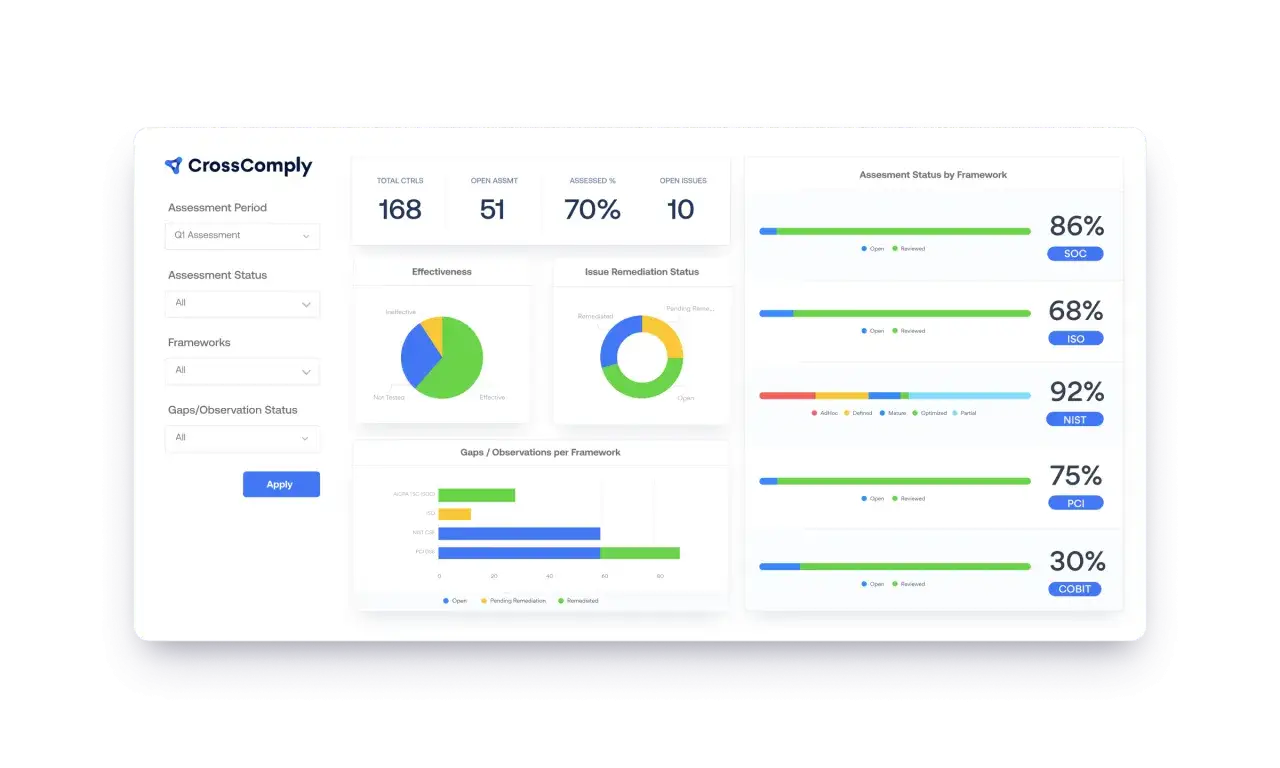

- The percentage of controls tested on schedule.

- The average time to close open issues.

- Whether repeat findings are decreasing or just re-labeled.

- How quickly policy updates follow regulatory or operational change.

- Whether training completion is tracked with exceptions, not just totals.

- Whether third-party reviews are current for the vendors that matter most.

I also care about root-cause analysis. If the same failure keeps appearing under different headings, the program is probably fixing symptoms instead of the control gap itself. A clean metric is useful only when it leads to a better decision.

That is the standard I use before I call a program durable.

The standard I use before I call a program durable

Before I would trust a compliance program, I want to answer five questions without digging through a folder tree: who owns each obligation, what changed since the last review, what was tested this quarter, what remains open, and which third parties are still in scope. If those answers are easy to produce, the program has momentum. If they require a scramble, it is still a paper system.

- Every obligation has an owner and a backup.

- Open issues have dates, priorities, and evidence of follow-up.

- Policies are updated after legal, operational, or vendor changes.

- Testing results are reported in a form leadership can act on.

- Third-party reviews are treated as part of the program, not an add-on.

That is the difference between a binder and a control environment that can handle growth, scrutiny, and change. If I had to reduce the whole topic to one rule, it would be this: build the habit of review, not the habit of repair. That is what makes ongoing compliance practical instead of performative.