I usually tell founders that startup taxes are less about one annual return and more about a system: the entity you choose, the money you pull out, the people you hire, and the states you touch. Get those pieces wrong early and the bill gets noisy fast; get them right and compliance becomes routine. This article breaks down the federal and state rules that matter first, plus the deductions and filing habits that save time later.

The first year is about setting the tax system, not just filing once

- Entity choice changes whether you pay self-employment tax, run payroll, or face corporate-level tax.

- Estimated taxes matter fast when profit is not covered by withholding; for many owners, the threshold is $1,000 of expected tax due.

- Payroll brings withholding, Social Security, Medicare, unemployment, and year-end forms the moment you hire.

- Startup costs can often be partly deducted, but only if you separate launch spending from ordinary operating expenses.

- State rules can add income, sales, withholding, or unemployment filings even when the federal side looks simple.

What startup taxes actually cover

When I map a new company’s obligations, I start with five federal buckets: income tax, estimated tax, self-employment tax, employment taxes, and excise tax. That sounds broad, but in practice it just means one thing: the way the business is structured determines how the profit is taxed and who is responsible for paying it.

| Tax bucket | What it means for a new business | Why founders miss it |

|---|---|---|

| Income tax | Business profit is reported on the return that matches the entity type. | Owners assume every structure is taxed the same way. |

| Estimated tax | Tax is paid during the year instead of waiting for filing season. | New founders expect withholding to cover everything, but many do not have wages yet. |

| Self-employment tax | Owners of pass-through businesses can owe Social Security and Medicare tax on business earnings. | People focus on income tax and forget the payroll-style layer on profit. |

| Employment taxes | Once you hire, you may need to withhold income tax and pay Social Security, Medicare, and unemployment taxes. | The first employee turns tax compliance from personal to operational. |

| Excise tax | Relevant only for certain products, services, and activities. | Most startups never see it, so it is ignored until a regulated model makes it unavoidable. |

Most startups never deal with excise tax, but if you are in fuel, transport, certain goods, or another regulated category, it can show up quickly. Once you see the stack, the next question is which legal structure puts those taxes in the right place.

How your entity choice changes the bill

I see too many founders treat an LLC as a tax answer. It is not. An LLC is a legal wrapper; the tax result depends on how it is classified, and that classification can make a meaningful difference in cash flow, paperwork, and audit risk.

| Structure | Typical tax treatment | Main advantage | Main tradeoff |

|---|---|---|---|

| Sole proprietorship or single-member LLC default | Income is generally reported on the owner’s return. | Simple compliance and low admin cost. | The owner usually pays self-employment tax on profit. |

| Partnership or multi-member LLC default | Business income passes through to the partners. | Flexible for cofounders and investor-friendly operating agreements. | Distributions, allocations, and capital accounts need discipline. |

| S corporation | Income passes through, but owner-employees must usually take payroll wages and may take additional distributions. | Can reduce self-employment tax exposure on part of the profit. | Reasonable compensation rules and payroll compliance matter. |

| C corporation | The company pays corporate income tax; dividends can be taxed again at the owner level. | Useful when reinvesting profits or aligning with certain funding plans. | Potential double taxation and heavier formalities. |

That table hides an important detail: pass-through owners may also qualify for the qualified business income deduction, which can reduce taxable income in some cases, but it is limited by income level and business type. My rule is simple: I do not choose an entity for a tax trick alone; I choose it when the tax result, investor expectations, and compliance burden all make sense together. Once that decision is made, the next layer is registration and filing.

The first tax registrations and filings to handle

The IRS checklist for starting a business begins with the basics: get an EIN if you need one, pick a structure, choose a tax year, and set up employee forms before anyone is paid. That sounds administrative, but it is where many later problems begin. A startup that skips the setup stage usually spends more time cleaning up notices than actually running the business.

- Get an EIN early. Most businesses need one even without employees, and the application is free. A single-member LLC without employees or excise tax liability may not need one federally, but banks and state agencies often make the practical answer different from the legal minimum.

- Register for state tax accounts. If you hire workers, you may need state withholding and unemployment accounts. If you sell taxable goods or certain services, you may need a sales tax permit.

- Choose your tax year and bookkeeping method. Calendar-year reporting is common, but the key is consistency. Your accounting method should match the way you actually operate.

- Set up payroll before the first paycheck. Do not wait until a contractor becomes an employee or a founder starts taking wages.

- Use electronic payment tools from day one. Federal payments can be made through EFTPS, IRS Direct Pay, or a Business Tax Account, which is a lot easier than scrambling at a deadline.

Read Also: Cash Flow vs. Profit: Why Profitable Businesses Fail

If you hire employees

The tax picture changes immediately. For 2026, Social Security tax is 6.2% for the employee and 6.2% for the employer on wages up to $184,500, and Medicare is 1.45% each with no wage base limit. Add income-tax withholding, Form 941 filings, year-end W-2s, W-3s, and usually federal unemployment reporting, and payroll becomes a system, not a side task. Once that foundation is in place, the focus shifts to the costs you can legitimately deduct.

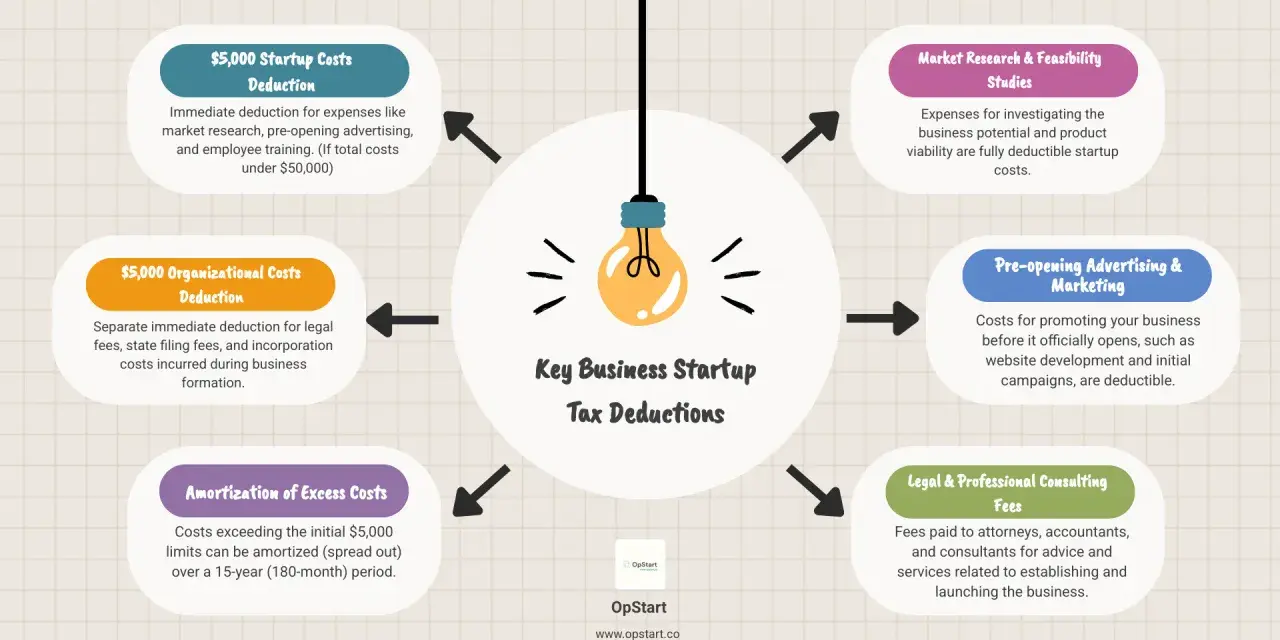

What you can deduct before and after launch

I like to separate spending into three buckets: pre-opening costs, ordinary operating expenses, and capital purchases. That distinction matters because not every dollar is deductible in the same way, and startup founders often blur the categories when the business is still small.

| Expense type | Typical tax treatment | What to watch |

|---|---|---|

| Startup and organizational costs | The IRS generally allows up to $5,000 of each type to be deducted, with the deduction reduced once total costs exceed $50,000; the rest is amortized over 180 months. | Keep launch expenses separate from day-to-day operations so the paper trail is clean. |

| Ordinary operating expenses | Usually deductible when they are ordinary and necessary for the trade or business. | Software, rent, insurance, professional fees, supplies, and advertising are common examples. |

| Equipment and other capital items | Often recovered through depreciation or other capitalization rules. | Do not treat every large purchase as an immediate write-off. |

| Home office and travel | Can be deductible if the requirements are met. | Home office rules are stricter than many founders expect, and mileage logs matter. |

I am conservative with launch receipts because tax treatment is easier when invoices are documented before money gets mixed into general spending. Product development, software build-out, and other pre-commercial work can also fall into special buckets, so I never assume the tax answer is “just expense it.” Knowing what is deductible is useful, but knowing when to pay the tax is what protects cash.

Estimated tax payments and payroll are the cash-flow trap

New businesses do not usually fail because the tax rate is mysterious; they get squeezed because the cash leaves before founders expect it to. Estimated tax is the classic example. If profit is not covered by withholding, the IRS expects you to pay during the year, not months later when the return is filed.

| Situation | What usually applies | Typical timing |

|---|---|---|

| Sole proprietor, partner, or S corporation shareholder | Estimated tax payments are generally due if you expect to owe $1,000 or more after withholding and credits. | For calendar-year taxpayers, payments are generally due April 15, June 15, September 15, and January 15 of the following year. |

| C corporation | Estimated tax payments are generally due if you expect to owe $500 or more. | Payments are generally due on the 15th day of the 4th, 6th, 9th, and 12th months of the corporation’s tax year. |

| Business with employees | Payroll deposits and employment tax filings become ongoing obligations. | Deposits and returns follow the payroll schedule and the filing calendar. |

I recommend a separate tax account and automatic transfers because founders are almost always more optimistic about free cash than their ledger is. The IRS gives several electronic payment options, but the real win is not the payment method itself; it is building a habit that makes each quarter predictable. Once the federal cash cycle is under control, the final layer is state and local tax exposure.

State and local taxes rarely fit one federal rule

The SBA’s basic split is useful: state and local obligations usually show up as income and employment taxes, but sales tax, franchise taxes, and gross-receipts-style taxes can appear depending on where you operate. In other words, a business can be perfectly fine at the federal level and still be under-registered in its home state.

- Sales tax can apply to physical goods and, in some states, to digital products or services.

- Nexus can be created by an office, inventory, employees, contractors, or sales volume, depending on the state.

- Payroll tax obligations often start the moment you hire across state lines.

- Local taxes may apply in cities or counties even when the state filing looks simple.

- Incentives and credits can exist too, which is why location planning belongs in the tax conversation, not after it.

My practical advice is to treat each new state as a separate compliance project. If the company sells online, keeps inventory outside its home state, or hires remote workers, the tax footprint can expand faster than the legal footprint. That is why a clean first-year setup matters more than any late-stage tax fix.

The boring setup that saves the most money in year one

- Separate business and personal accounts before the first payment lands.

- Save every launch invoice with a short note explaining the business purpose.

- Calendar estimated tax dates before revenue becomes uneven.

- Register payroll early if there is any chance the first contractor becomes an employee.

- Review entity choice again once revenue is stable enough that tax savings are measurable, not hypothetical.

- Check state registrations whenever you add a new state, warehouse, or employee.

If I had to reduce the first year to one principle, it would be this: tax compliance is cheaper when it is built into the launch, not patched on later. A founder who gets the structure, payroll, records, and state registrations right usually has more room to focus on growth, fundraising, and hiring instead of answering avoidable notices.