A well-built risk scoring framework only works when it changes decisions. In U.S. compliance work, that means the score has to help me decide what deserves enhanced due diligence, tighter monitoring, faster escalation, or a lighter touch. In 2026, the pressure is less about collecting data and more about proving that the method is defensible, repeatable, and tied to real control actions.

The practical takeaway in one glance

- A score should help prioritize action, not replace human judgment.

- In compliance programs, the strongest inputs usually come from customer, product, geography, channel, and behavior data.

- The best models are simple enough to explain to management, auditors, and regulators.

- Documentation matters as much as the math behind the number.

- A score stays useful only when it is tested, refreshed, and connected to control intensity.

How I think about risk scoring in compliance

I treat the number as a triage tool, not as a verdict. NIST SP 800-30 frames risk assessment as input for executive decisions, and the FFIEC's BSA/AML Manual uses the same logic for bank compliance programs; in both cases, the point is to prioritize action, not to hide judgment behind math.

That distinction matters because a score should answer a narrow question: where should limited attention go first? It should not pretend to eliminate uncertainty, and it should not be so vague that every case still needs an argument. When the model is useful, it gives me a repeatable way to separate routine activity from cases that need deeper review. Once that role is clear, the next step is choosing the inputs that deserve weight.

| What the score is | What the score is not |

|---|---|

| A structured way to compare relative exposure | A legal safe harbor |

| A trigger for review, monitoring, or escalation | A substitute for due diligence |

| A way to standardize decisions across teams | A promise that every case is equally understood |

| A documentation tool for audit and oversight | A black box that no one can explain |

When the model is built well, the business logic is visible. When it is built poorly, the number becomes decorative. That is why I prefer simple, explainable methods before anything more complex.

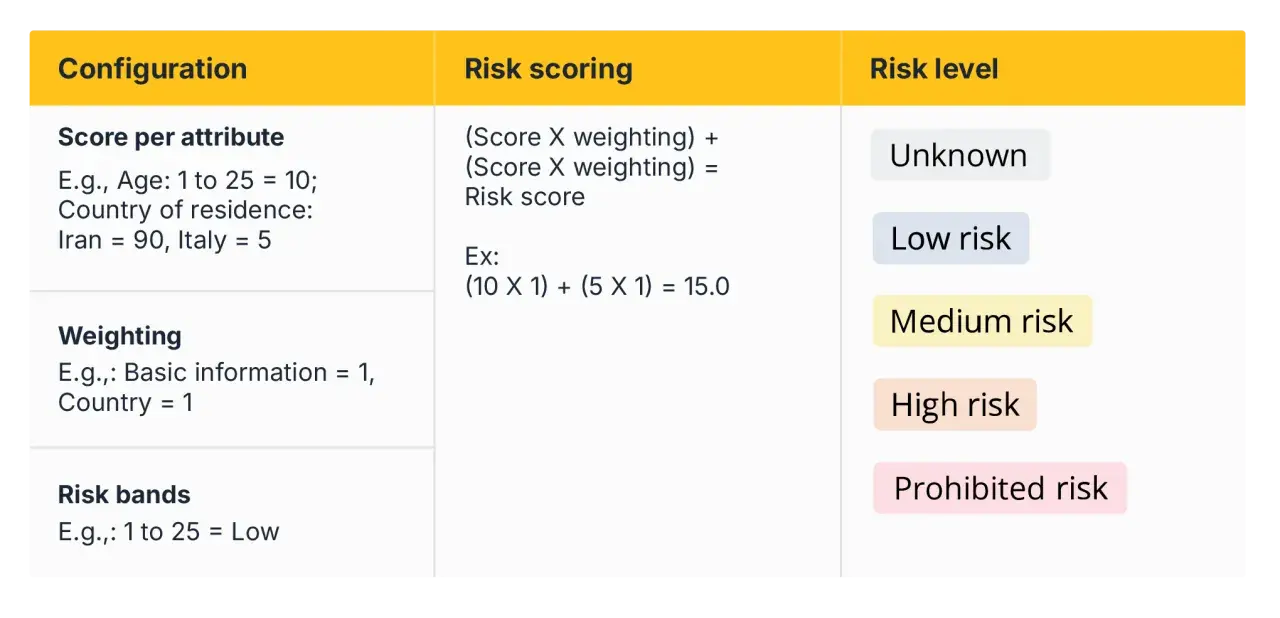

The inputs that matter most in U.S. compliance

Most scoring systems become more reliable when they focus on a small set of factors that actually move risk. In practice, I start with the elements that regulators, examiners, and internal audit teams already expect to see reflected in the program.

| Input | Why it matters | What I look for |

|---|---|---|

| Customer profile | Different customer types create different exposure levels | Ownership structure, source of funds, occupation, expected activity |

| Geography | Some jurisdictions carry higher sanctions, fraud, or AML exposure | Countries, states, corridors, and cross-border activity |

| Products and services | Some offerings are harder to monitor than others | Wire activity, cash intensity, account complexity, transfer speed |

| Delivery channel | Remote or intermediated onboarding can weaken visibility | Non-face-to-face onboarding, third-party introduction, digital only flows |

| Behavior and activity | Actual use often matters more than the stated profile | Volume spikes, unusual counterparties, transaction drift, review exceptions |

| Third parties | Partners can add hidden exposure and control gaps | Agents, resellers, vendors, introducers, and nested relationships |

The mistake I see most often is overvaluing one visible signal, then ignoring the context around it. A high-volume customer is not automatically high risk, and a low-volume customer is not automatically safe. The relationship between factors is what matters, which is why bank and compliance teams should always test whether the score still makes sense after a few real cases are reviewed. After the inputs are defined, the real work is turning them into a method that can be explained and repeated.

A build process that stays auditable

I usually want the first version of the model to be boring in a good way. If a method is too clever to explain, it is usually too fragile to defend.

Six steps to get the first version right

- Define the use case clearly. A customer onboarding score is not the same thing as a vendor or transaction score.

- Choose a small set of factors. Five to eight meaningful inputs are usually easier to validate than twenty vague ones.

- Set a scale. Many teams start with a 1-5 scale because it is simple to understand and easy to map into a matrix.

- Assign weights. Heavier weights should reflect actual impact, not just a manager’s preference.

- Test against real cases. I want to see whether higher scores actually align with higher review burden, more exceptions, or more suspicious patterns.

- Document the rationale. If the model cannot be explained in plain English, it is not ready for broad use.

Read Also: Sanctions Screening in KYC - Build an Effective Program

Which method fits which team

| Approach | Best for | Main strength | Main trade-off |

|---|---|---|---|

| Rules-based checklist | Smaller programs or early-stage designs | Fast to build and easy to explain | Can be too coarse to separate borderline cases |

| Weighted matrix | Most compliance teams | Balanced and auditable | Weights can become subjective if not tested |

| Quantitative model | Mature programs with strong data quality | More consistent scoring over time | Needs validation and better governance |

| ML-assisted model | Large datasets and high case volume | Can surface patterns humans miss | Harder to explain, challenge, and defend |

For most U.S. compliance teams, the weighted matrix is still the sweet spot because it balances simplicity with enough nuance to matter. Once the model is live, though, the focus shifts from design to failure modes. That is where a lot of otherwise solid programs lose credibility.

Where models fail in practice

The biggest failures are rarely mathematical. They are usually operational.

- Stale inputs - The model keeps using old customer or product data after the business changes.

- Hidden overrides - Staff keep changing outputs manually, but no one tracks why.

- Too many factors - The model becomes noisy because every possible variable gets a point value.

- Weak documentation - No one can explain why one factor matters more than another.

- False precision - A score of 72 looks scientific, but the underlying data may be rough.

- No challenge process - There is no formal way to question a score when the result looks wrong.

I also watch for a more subtle problem: teams sometimes design the score to satisfy reporting needs rather than operational needs. That produces a neat dashboard and a weak control. If the number does not change review depth, monitoring frequency, or escalation behavior, it is not doing enough work. Once the failure modes are obvious, the score can be connected to real operational actions.

How scores should drive different compliance actions

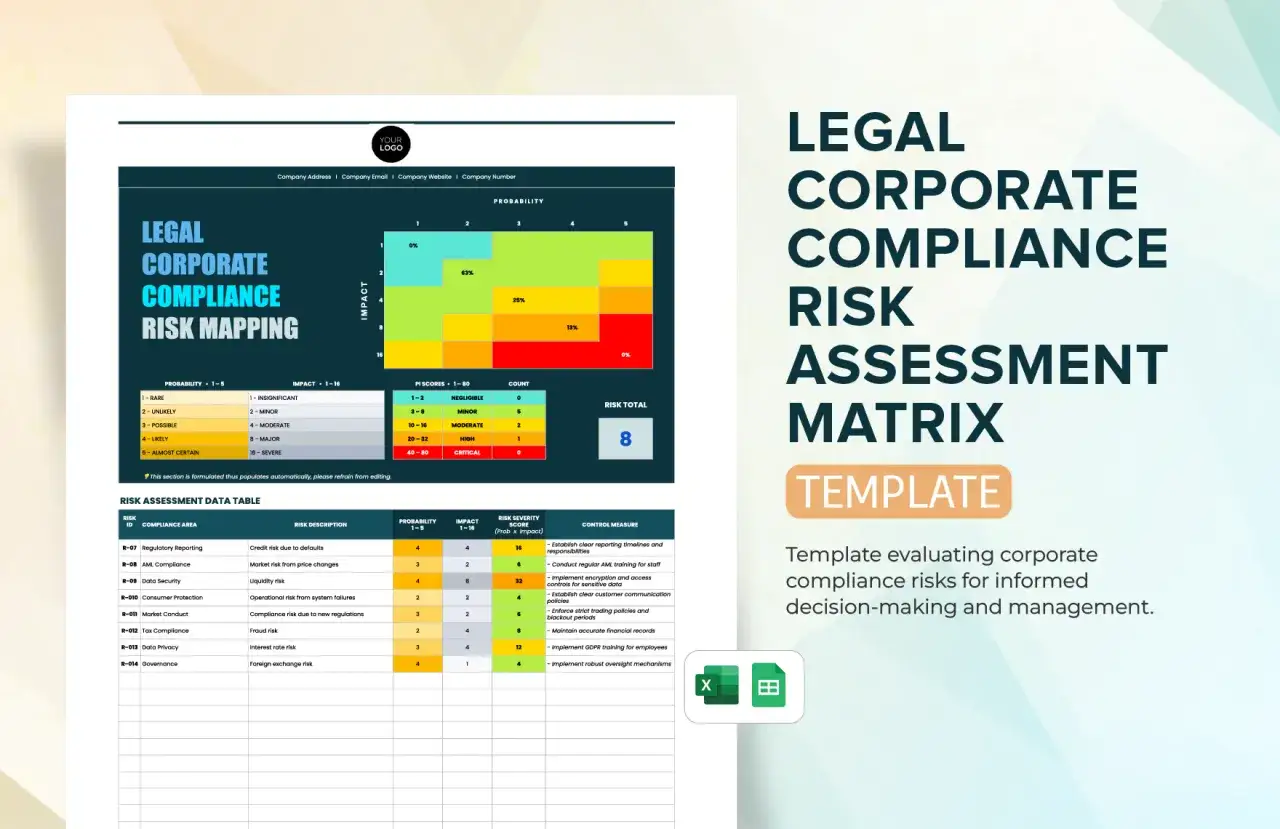

If you use a 5x5 matrix, the score range is 1 to 25. I would treat the bands below as an example, not as a universal rule; the right cutoffs depend on your actual risk profile and case history.

| Score band | Typical treatment | What to document |

|---|---|---|

| 1-8 | Standard onboarding and routine monitoring | Why the case stays in the low-risk band |

| 9-15 | Periodic review plus targeted alerts | Which factors pushed the score upward |

| 16-25 | Enhanced due diligence, senior review, tighter monitoring | Why the case needs stronger controls and who approved them |

The important part is not the exact cutoff. It is the link between the score and the action. A high number should mean more scrutiny, more documentation, or faster escalation. A low number should mean the opposite only if the underlying facts still support it. The best programs keep that link visible enough that a reviewer can trace every decision back to a specific reason.

The controls I would not skip before trusting the score

Before I let a scoring model drive real compliance work, I want a few controls in place that make the output defensible.

- A written methodology that names each factor, its weight, and the owner of the model.

- A change log that records threshold shifts, overrides, and exceptions.

- A sample-testing routine that checks whether high scores line up with higher-risk cases in practice.

- A refresh cadence tied to product launches, channel changes, geography shifts, and major customer mix changes.

- A clear escalation path for borderline cases and a documented reviewer sign-off process.

Those controls are what turn a score into a real compliance asset. Without them, the number looks precise but behaves like an opinion. With them, it becomes a practical tool for governance, monitoring, and better decision-making across the program.