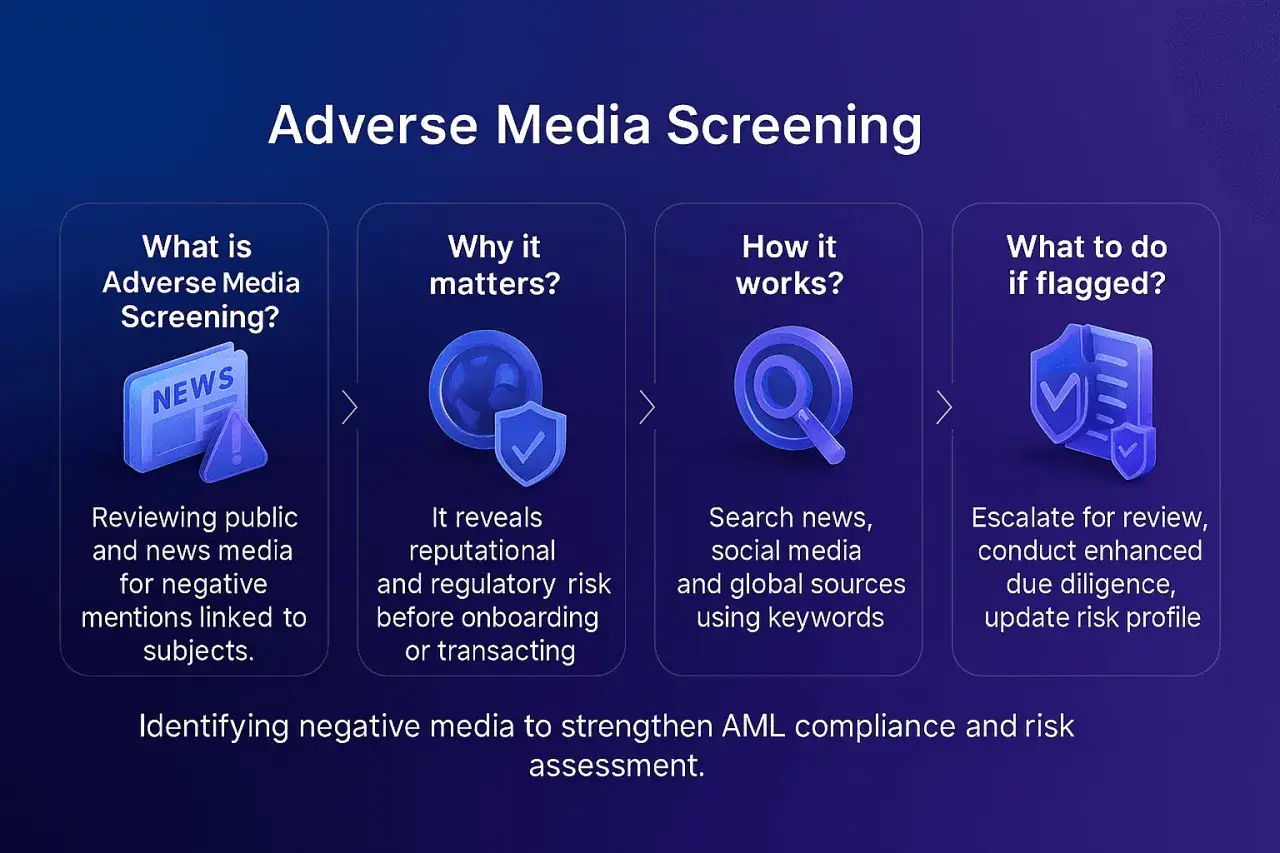

Adverse media screening has become a practical part of modern anti-money-laundering work: it helps teams spot negative news, connect it to customer risk, and decide when more review is warranted. In U.S. programs, adverse media AML checks are most useful when they sit inside a broader risk-based process rather than as a blunt yes-or-no filter. This article explains what the screening is, where it fits in compliance, how to run it without drowning in false positives, and what to do when the news is real.

Key points at a glance

- Adverse media screening looks for credible negative public information that may change a customer’s AML risk.

- In the U.S., it supports customer due diligence and ongoing monitoring, but it is not a standalone SAR trigger.

- The best programs separate true risk signals from duplicate alerts, stale allegations, and name-only matches.

- Coverage, escalation rules, and documentation matter more than chasing every possible article.

- A workable process links news findings to customer risk ratings, enhanced due diligence, and governance decisions.

Where adverse media AML fits in a risk-based program

By adverse media, I mean negative public information that could indicate fraud, corruption, money laundering, sanctions evasion, terrorist financing, or similar conduct that changes a customer’s risk profile. I do not treat it as proof of wrongdoing; I treat it as a signal that may justify more questions, a higher risk rating, or enhanced due diligence.

That distinction matters because negative news sits in a different lane from sanctions screening and transaction monitoring. Sanctions screening asks whether a person or entity matches a list; transaction monitoring asks whether activity looks unusual; adverse media asks whether the broader public record suggests hidden risk, weak governance, or a pattern of illicit behavior.

| Control | Main question | Typical input | Typical output |

|---|---|---|---|

| Adverse media | Does public information suggest elevated AML risk? | News articles, court records, regulator releases, credible open-source reporting | Risk review, enhanced due diligence, escalation, or monitoring |

| Sanctions screening | Is there a list match or prohibited relationship? | Sanctions lists, watchlists, internal restricted-party records | Clear, escalate, block, or reject according to policy |

| Transaction monitoring | Does the activity pattern look inconsistent or suspicious? | Payments, volume, velocity, counterparties, geographic routes | Alert review, narrative analysis, possible SAR referral |

Once you see that distinction, the next issue is what regulators actually expect from a U.S. program and where the line is drawn.

What U.S. regulators expect and what they do not

FinCEN’s guidance draws a useful boundary: media searches are not categorically required, and negative news alone does not automatically trigger a SAR. That leaves firms with flexibility, but it is not a free pass; if you choose to use adverse media, you still need documented policies, risk-based triggers, and a defensible escalation path.

The FATF standard pushes the same logic from a different angle. Risk-based AML is supposed to match controls to exposure, so higher-risk customers, geographies, industries, and ownership structures deserve deeper review. In other words, the right question is not “Should every customer get the same media search?” The better question is “Which relationships justify stronger open-source review, how often, and with what review standard?”

For U.S. teams, that distinction affects exam readiness. If the program says it screens adverse news, I expect to see the method, the scope, the refresh cadence, and the rationale for exceptions. If the program does not screen broadly, I still expect the firm to show how it otherwise learns about negative information and feeds that into monitoring. That bridge leads directly to workflow design.

How I would build a screening workflow that stays useful

In practice, the best workflow is narrow enough to be manageable and broad enough to catch meaningful risk. I usually think in five steps.

- Define scope. Start with customers, beneficial owners, controllers, signatories, and other exposed parties that matter to the relationship.

- Set risk tiers. Higher-risk segments get broader source coverage and shorter review cycles than low-risk retail or low-value relationships.

- Use source types deliberately. News coverage, court records, regulator releases, company registries, and credible local-language reporting each catch different risk signals.

- Match on more than the name. I prefer a rule set that looks at aliases, geography, age, business type, and known associates before it escalates an alert.

- Document the decision. An analyst note should say why the result was kept, cleared, escalated, or referred for enhanced due diligence.

OSINT, or open-source intelligence, is just the disciplined use of public information. In compliance, that matters because an undisciplined search can produce a wall of noise, while a well-tuned one can surface exactly the fact pattern that changes a risk decision. That brings us to the harder part: telling meaningful news from background static.

What counts as meaningful negative news and what usually does not

I separate alerts into signals that should move the file and signals that should merely be noted. The difference is usually credibility, relevance, recency, and whether the article actually identifies the same person or entity.

| Signal | Why it matters | What I check next |

|---|---|---|

| Criminal charges, convictions, or regulator action | Stronger evidence that risk is real | Jurisdiction, dates, appeal status, and connection to the customer |

| Multiple independent reports with documents or named authorities | Higher confidence than a single article | Whether the facts are consistent across sources |

| Single unsourced allegation, blog post, or opinion piece | Low confidence and high false-positive risk | Whether anything else corroborates it |

| Name-only match | Often not the same person | Address, date of birth, ownership data, business history, and associates |

| Old news with no current relevance | May not reflect present risk | Whether the issue was resolved, dismissed, or superseded |

The red flag I see most often is lazy equivalence: an article exists, therefore the customer is risky. That is not how good compliance works. A stale allegation about a common-name match is not the same thing as a recent enforcement action tied to the same beneficial owner, and the program should say so plainly.

As a rule, I give more weight to facts that are independently reported, recent, and directly connected to the person, entity, or network under review. That standard becomes even more important when the alert could affect onboarding, periodic review, or account exit.

How to respond when the news is real

When the match looks credible, I do not jump straight to closure or SAR language. I start by confirming identity, reading the full source material, checking whether the matter is ongoing, and comparing the information with the customer file and transaction history.

- Clear the alert if the person is not the customer, the article is not credible, or the fact pattern is unrelated.

- Escalate to enhanced due diligence if the news suggests ownership opacity, bribery, fraud, sanctions exposure, or another material AML issue.

- Update the customer risk rating if the news changes the profile but does not yet justify account action.

- Refer for SAR review if the facts, taken together, suggest suspicious activity rather than mere reputational concern.

- Consider exit only when the risk is no longer acceptable under policy, legal obligations, and relationship strategy.

The rule does not turn negative news into an automatic filing trigger. That is a useful guardrail, because it keeps compliance from turning into reflexive over-reporting. The real task is to determine whether the news, together with transactions and customer behavior, supports a suspicion that belongs in the SAR process.

I also like to keep the escalation path explicit. Analysts should know when to consult legal, when to involve senior compliance, and when a case should stay open for monitoring rather than being pushed into a premature decision. That discipline is what keeps the process defensible.

The mistakes that weaken adverse media programs

Most failure modes are operational, not conceptual. The program exists on paper, but it breaks because the search logic is weak, the reviewers are inconsistent, or nobody can explain why one alert was escalated and another was ignored.

- Overbroad queries: they create noise and train reviewers to ignore the queue.

- Overnarrow queries: they miss aliases, transliterations, and local-language coverage.

- No recency filter: stale stories swamp current risk.

- No evidence standard: one article is treated as enough even when it is weak or uncorroborated.

- Poor documentation: analysts clear or escalate alerts without showing why.

- One-size-fits-all cadence: low-risk and high-risk customers are reviewed the same way.

The most expensive mistake is assuming technology alone solves the problem. Tools help, but the control only works when policy, training, and escalation criteria are aligned. From there, the final question is not whether adverse media exists, but what a mature program does with it.

What a mature negative-news program should leave you with in 2026

A strong program does not try to eliminate every false positive. It produces a repeatable way to decide when news is relevant, when it changes risk, and when it should be ignored because it is weak, stale, or disconnected from the customer.

If I were auditing a program today, I would look for three things: a written scope, a clear review standard, and an audit trail that shows how the team turned information into action. That is the difference between a screening exercise and a real compliance control. When those pieces are in place, adverse media becomes useful governance infrastructure rather than another noisy alert source.

In practice, the best teams keep the process simple enough to run every day and rigorous enough to defend in front of examiners, auditors, and management. That is the standard I would aim for.