A strong enterprise risk assessment should tell leaders where the organization is exposed, what controls already exist, and where money, policy, or board attention needs to move next. For U.S. businesses, that means looking beyond generic risk lists and focusing on the practical intersection of operations, compliance, governance, and reputation. In this article I break down what the process should do, how to run it, which risks deserve the most attention, and how to turn the findings into decisions rather than another static report.

What matters most before you start

- The goal is not to produce a thick file; it is to rank exposure and direct action.

- A useful assessment combines business input, legal/compliance input, and control evidence.

- The best risk models separate inherent risk from residual risk, so leaders can see what remains after controls.

- Most U.S. organizations should revisit top risks quarterly and update immediately after a major incident, acquisition, or regulatory shift.

- Third-party risk, cyber risk, reporting controls, and conduct risk usually deserve a place near the top of the list.

What this process is meant to change

At its best, the assessment is a decision tool. It is a structured way to identify risk scenarios, analyze how likely and damaging they are, and decide how to respond. It shows which risks can be accepted, which need stronger controls, which require legal review, and which belong in front of the board. When I see a company treat the exercise as a compliance formality, the output usually becomes too broad to be useful and too vague to drive action.

The real value comes from making the risk picture legible. A business can tolerate some operational noise, but it cannot afford to confuse a low-probability annoyance with a high-impact issue that could trigger regulatory scrutiny, contract loss, or a material control failure. That is why I start by asking a simple question: what would actually change if the organization learned something new from this review? Once that answer is clear, the next step is to build a workflow that produces evidence, not just opinions.

How I would run the review from scope to action

I prefer a process that is structured enough to repeat, but not so rigid that it ignores how the business really works. A first pass often takes 4 to 8 weeks for a mid-sized company if interviews and basic data are available. Larger or heavily regulated organizations should expect longer, especially if business units are spread across geographies or the control environment is uneven.

- Define scope - Set the business units, jurisdictions, and risk themes that belong in the review. A U.S. public company will usually have a broader scope than a private domestic service business.

- Build a risk universe - Start with categories such as compliance, finance, technology, operations, people, and third parties. Then break them down into actual scenarios, not abstract labels.

- Collect evidence - Use incident logs, hotline data, audit findings, contract reviews, regulatory changes, training completion, vendor due diligence, and prior remediation work. This is where the review becomes real.

- Interview owners - I look for people who run the process day to day, not just executives. Frontline detail usually exposes the gap between policy and practice.

- Score the risks - Rate likelihood, impact, and control strength in a consistent way. Keep the definitions tight so different teams do not invent their own scale.

- Assign treatment - Decide whether each risk should be avoided, reduced, transferred, or accepted. Every major risk should have a named owner and a due date.

- Document the risk register - Record the scenario, score, owner, control gaps, and next action in one place so the organization can track decisions over time.

- Track follow-through - If the result does not change policies, testing, training, or budgeting, the assessment has not done its job.

That workflow works because it forces the organization to move from description to action. From there, the more difficult question is how to rank the findings without pretending the numbers are more precise than they really are.

How to score and prioritize risk without fake precision

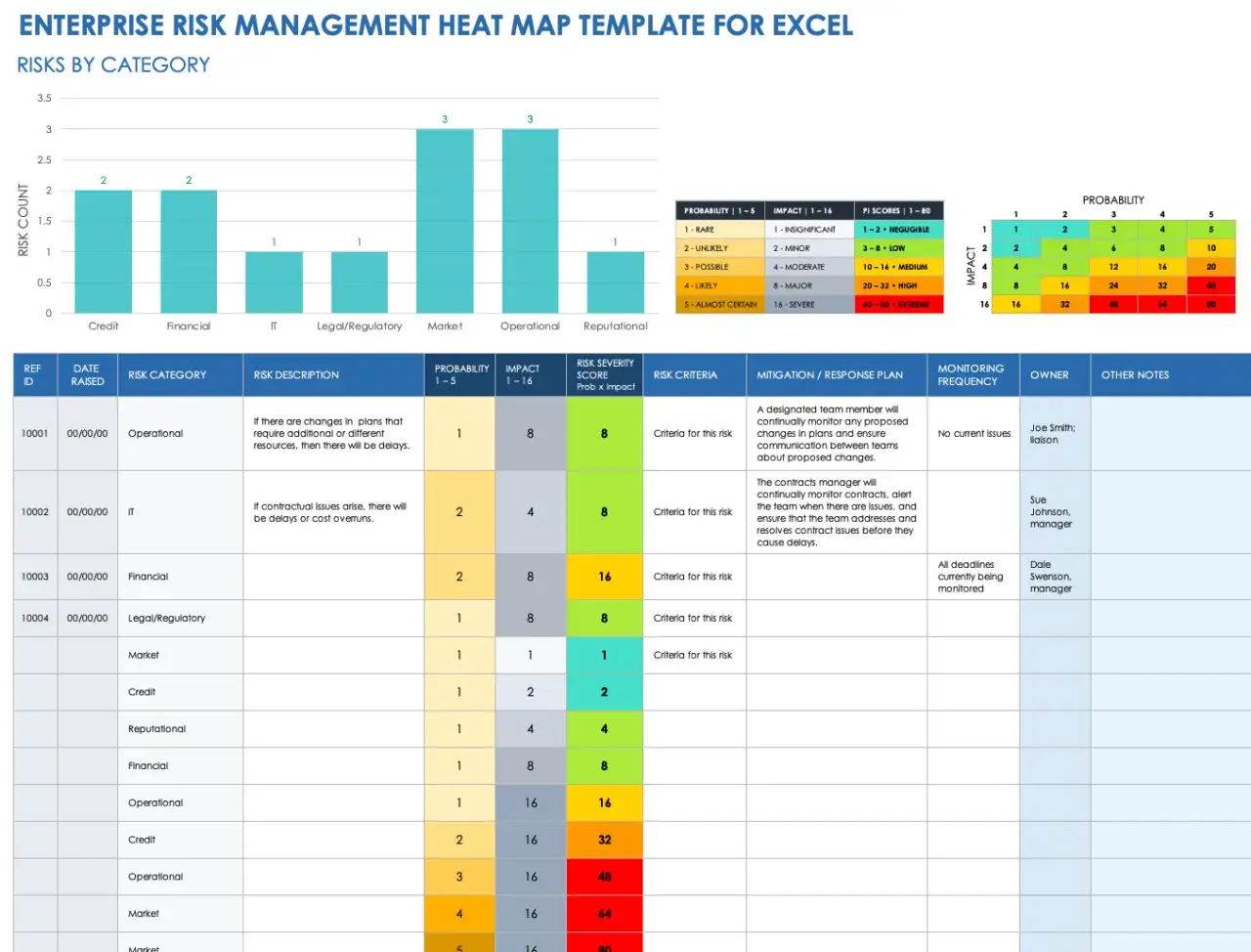

I am cautious about scoring models that look scientific but behave like guesswork. A 5 by 5 matrix is common because it is easy to explain, not because it is magically accurate. Used well, it creates a shared language. Used badly, it gives leaders a false sense of certainty.

| Method | Best use | Strength | Limit |

|---|---|---|---|

| Qualitative | Early reviews, smaller organizations, quick prioritization | Fast and easy to explain | More subjective and harder to compare across teams |

| Semi-quantitative | Most enterprise programs | Gives consistent ranking without heavy modeling | Can create fake precision if the scoring rules are loose |

| Quantitative | High-value exposures, capital planning, insurance, cyber scenarios | Useful when the data is strong and the stakes are high | Slower, data-heavy, and not worth forcing on every risk |

The split between inherent risk and residual risk matters here. Inherent risk is the exposure before controls. Residual risk is what remains after controls, monitoring, and remediation. If a risk looks severe before controls but ordinary after controls, that difference should be visible in the score and in the narrative. A control on paper is not the same thing as a control that operates consistently, which is why evidence matters more than policy language.

For U.S. organizations, I also like to prioritize by consequence, not only frequency. A risk that happens rarely but can trigger fines, a shutdown, a license problem, or a major disclosure issue belongs near the top even if it looks quiet on paper. That logic becomes clearer when you map the main risk categories to the evidence you expect to see.

The risk areas U.S. organizations should not bury

In practice, the same themes appear again and again. The details vary by industry, but the pressure points are familiar. The table below is the one I would use to start a board-level discussion.

| Risk area | What I would ask | Evidence that matters |

|---|---|---|

| Third-party and anti-bribery risk | Who sells, transacts, or speaks for the company in high-risk markets? | Due diligence files, contract clauses, payment reviews, and monitoring results |

| Cybersecurity and data privacy | Where are sensitive systems, who has access, and how fast can the company recover? | Access logs, patching records, tabletop exercises, incident response metrics |

| Financial reporting and internal controls | Can management trust the numbers and the close process? | Reconciliations, segregation of duties, control tests, remediation tracking |

| Conduct and workplace risk | Are people comfortable reporting issues, and do leaders act on them? | Hotline trends, investigation timing, training data, discipline records |

| Regulatory and transactional risk | Do acquisitions, new products, or new geographies change the compliance profile? | Deal diligence, integration plans, legal reviews, change logs |

Two themes sit behind almost every one of those categories: third-party exposure and control weakness under change. A program can look fine in steady state and then break as soon as the company acquires a business, enters a new market, or outsources a critical function. That is why the review has to be tied to change management, not just annual compliance work. The next step is understanding the mistakes that keep otherwise sensible programs from producing useful results.

The mistakes that make the review look good and work badly

I see the same failure modes over and over, and they are usually avoidable.

- Too many categories - If every issue becomes its own category, leaders cannot see the signal.

- No shared definitions - If teams score impact differently, the ranking becomes political instead of analytical.

- Anonymous ownership - A risk without a named owner tends to survive every meeting untouched.

- Policy over evidence - Policies tell me what should happen; evidence tells me what is actually happening.

- Annual-only thinking - A static review misses the risks introduced by acquisitions, incidents, new vendors, and new laws.

- No remediation discipline - If control fixes are not tracked to closure, the organization learns the wrong lesson.

One subtle but costly mistake is over-relying on executive interviews. Senior people can describe the intended control environment very well, but they are often the least useful source for understanding how the process behaves on a busy Tuesday afternoon. I always want some mix of management input, frontline input, and actual artifact review. That is what turns the work from a presentation into an operating picture.

How to turn findings into governance instead of another report

If the assessment ends with a slide deck, the organization has probably spent money without changing behavior. Strong governance means the output shapes budget, policy, testing, and reporting. In practice, that requires four things.

First, the board or the relevant committee should see a short list of top risks, not a wall of color-coded boxes. I usually prefer a focused view of roughly 8 to 12 material risks, with trend arrows and remediation status. Anything more becomes difficult to govern.

Second, management should connect each major risk to an owner, a control set, and a remediation plan. That plan should say what changes, by when, and how success will be measured. If there is no deadline, there is usually no urgency.

Third, the company should align risk appetite and risk tolerance with decision-making. Appetite is the amount of risk the organization is willing to take to pursue its goals. Tolerance is the acceptable variation around a specific objective. When those two ideas are confused, leaders often approve exposure they would never knowingly accept.

Fourth, the process should influence resources. If the highest-rated risk is a third-party channel, then third-party monitoring needs funding. If the highest-rated risk is a cyber issue, then the security and response budget needs to reflect that reality. I have little patience for assessments that identify risk cleanly but leave the budget untouched.

That governance layer is what makes the work durable. Once that is in place, the final question is cadence: how often should the organization revisit the analysis so it stays useful rather than stale?

The cadence that keeps the program useful

The strongest programs I see treat risk review as a living process. They do not wait twelve months for the next formal cycle if the business changes tomorrow. My default rhythm is simple: a full refresh at least annually, a lighter quarterly review of the top risks, and event-driven updates whenever something material happens.

- Quarterly - Recheck the top risks, open remediation items, and control performance trends.

- After an incident - Reassess the affected area as soon as the root cause is understood.

- After an acquisition or major vendor change - Review inherited controls, new exposures, and integration timing.

- After a significant legal or regulatory shift - Update the risk universe and control map before the next reporting cycle.

That rhythm matters because risk is not static. Business lines change, systems change, people change, and enforcement expectations change with them. In practice, U.S. compliance teams are expected to show periodic testing, continuous review, and real follow-through. If I had to reduce the whole topic to one rule, it would be this: keep the assessment close to operations, or it will drift away from reality.

For most U.S. organizations, the best next step is simple: map the top 10 risks to owners, controls, and evidence, then decide what gets reviewed quarterly and what gets re-tested after change. That keeps the work close to operations and makes the next cycle faster, sharper, and easier to defend.