Starting a nonprofit in the United States is a legal and operational project, and this is the practical version of how to start a nonprofit without wasting time on the wrong filing path, vague bylaws, or avoidable compliance mistakes. I focus on the decisions that actually matter: which tax-exempt structure fits the mission, what documents need to exist before you file, how the federal application works, and what ongoing reporting looks like once the organization is live. If you want a clean launch, the details matter more than the branding.

The practical launch sequence in one view

- State law comes first. You form the nonprofit entity under state law before you apply for federal tax exemption.

- Most founders start with a 501(c)(3). It fits charitable, educational, religious, and similar public-benefit missions.

- Federal filing is electronic. Form 1023 costs $600, Form 1023-EZ costs $275, and both are filed through Pay.gov.

- EINs are not the first step. Get the entity legally formed first, then apply for the EIN.

- Annual compliance is ongoing. Small organizations often use Form 990-N if receipts are normally $50,000 or less.

- Fundraising has separate rules. Many states require charitable solicitation registration before you ask residents for donations.

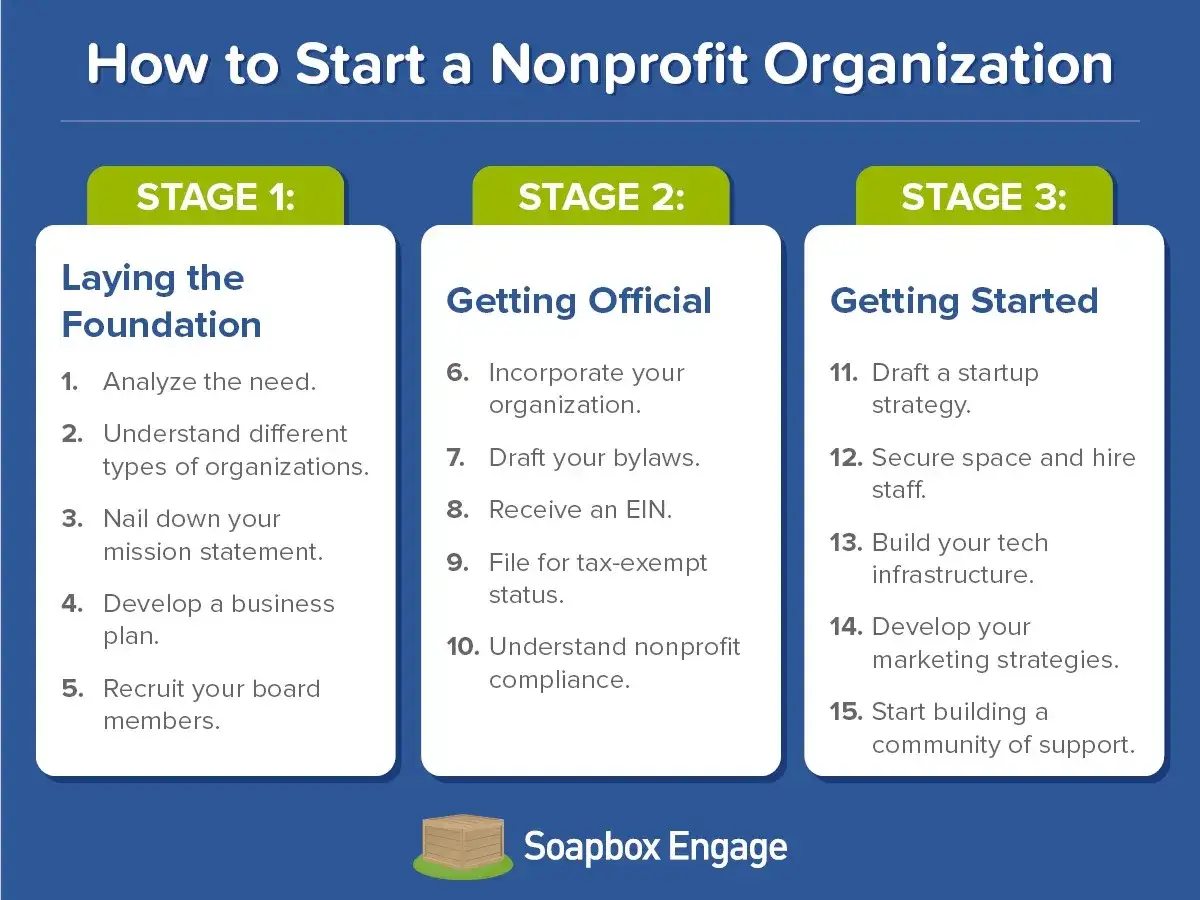

Choose the right nonprofit model before you draft documents

In practice, the first decision is not paperwork, it is purpose. I usually tell founders to pick the tax-exempt model that matches the work they plan to do, because the rest of the structure has to support that choice. State law creates the entity, federal law decides tax exemption, and those two layers need to line up.

For most mission-driven organizations, a 501(c)(3) is the default route. It fits charitable, educational, religious, scientific, and similar public-benefit work. If the organization is built primarily around advocacy or social welfare, a different lane may be more appropriate. Forcing the wrong structure onto the mission is one of the fastest ways to create compliance trouble later.

| Path | Best fit | Typical federal filing | Practical tradeoff |

|---|---|---|---|

| 501(c)(3) | Charitable, educational, religious, scientific, and public-benefit work | Form 1023 or Form 1023-EZ | Most recognizable nonprofit structure, but also the most rules-heavy |

| 501(c)(4) | Social welfare organizations with more advocacy flexibility | Form 8976 notice and Form 1024-A | Better for advocacy-heavy work, but not the same public charity model |

| Other tax-exempt organizations | Trade groups, social clubs, and other specialized missions | Form 1024 | Useful when the mission is not a classic charity |

If I had to reduce this to one rule, it would be simple: do not pick the tax form first and the mission later. Once the lane is right, the paperwork becomes much easier to make consistent. That leads directly to the part most people underestimate, which is the legal foundation under the organization.

Build the legal foundation before you file

The federal application is not where the organization begins. It begins with the entity documents that make the nonprofit real under state law. For a 501(c)(3), the organizing documents must limit the purpose to exempt purposes and must not authorize activities that are more than an insubstantial part of the work outside that mission. That is the organizational test in plain English: your documents have to say the right things, and the organization has to actually do the right things.

I would not file the federal application until these pieces are clean:

- Articles of incorporation or trust documents with purpose language and a proper dissolution clause.

- Bylaws that describe how the board operates, how meetings are held, and how decisions are approved.

- Initial board actions such as appointing officers, adopting the bylaws, and approving the first budget.

- Conflict-of-interest procedures so board members are not voting on matters where they have a personal stake.

- Basic recordkeeping rules so minutes, approvals, and financial decisions are documented from day one.

Bylaws are internal operating rules, and state law may require them even when federal tax law does not. I prefer to treat them as more than a formality, because weak bylaws usually become weak governance. If your board cannot explain who approves spending, who signs contracts, and who handles emergencies, the nonprofit is not really operational yet. With the entity documents aligned, the federal filing is mostly about discipline and completeness.

File for federal exemption the smart way

Once the organization is legally formed, the next step is the federal tax-exemption process. For a new charitable organization, that usually means Form 1023 or, if eligible, Form 1023-EZ. The application is filed electronically, and the user fee is $600 for Form 1023 or $275 for Form 1023-EZ. That is one of the few parts of startup that is actually straightforward.

There is one timing detail that founders often miss: the IRS generally expects the organization to be legally formed before it applies for an EIN, and if the exemption application is filed within 27 months after the month the organization was legally formed, the effective date can reach back to the formation date. Wait too long, and you can lose that retroactive advantage. In other words, delay is not harmless.

- Form the nonprofit entity with the state first.

- Get the EIN after the entity exists.

- Confirm whether Form 1023-EZ is actually available and appropriate.

- File the exemption application electronically and pay the user fee.

- Keep copies of the organizing documents, board approvals, and application package.

I also tell founders not to confuse a fast filing with a safe filing. Form 1023-EZ is shorter, but it is only for eligible organizations, and a rushed application can create problems if the mission, governance, or activities are not cleanly described. After federal status is underway, the real challenge shifts from formation to ongoing compliance.

Set up fundraising and annual compliance before the first donation

Fundraising is where new nonprofits often discover that the rules are broader than they expected. Many states require charitable organizations to register before they solicit residents for contributions, and some states also require periodic financial reports. A few local governments add their own layers. If your organization plans to fundraise across state lines, registration is not a future problem; it is a launch requirement.Annual federal reporting matters just as much. Most small exempt organizations that have annual gross receipts normally at or below $50,000 can satisfy their annual reporting requirement with Form 990-N. Gross receipts means total money received, not profit after expenses. Larger organizations generally move into Form 990-EZ or Form 990, depending on their size and structure. The deadline for Form 990-N is the 15th day of the 5th month after the close of the tax year.

Two more operational issues deserve attention early:

- Unrelated business income can create tax filing obligations even when the organization is exempt. If unrelated gross income is $1,000 or more, Form 990-T is generally required.

- Quid pro quo disclosures matter when donors receive something in return, such as a dinner, ticket, or merchandise. The charity has to disclose the fair market value of what was received.

- Public inspection rules apply to many charitable organizations, including the approved exemption application and the last three annual information returns.

This is the part that turns a nonprofit into a real operating business, even if it is mission-driven. The organization has to know where the money came from, what restrictions apply, what was delivered in return, and what must be filed on time. That reality is what makes a real budget more useful than a hopeful one.

Budget for the real startup cost

People often assume the biggest expense is legal paperwork. In reality, the larger cost is usually the combination of setup, compliance, and cleanup if the early decisions were sloppy. In 2026, the federal user fees are fixed at $0 for an EIN, $275 for Form 1023-EZ, and $600 for Form 1023. Form 990-N itself has no filing fee.

| Cost item | What to expect |

|---|---|

| EIN | Free if filed online |

| Form 1023-EZ | $275 user fee |

| Form 1023 | $600 user fee |

| Form 990-N | No filing fee |

| State incorporation and annual filings | Varies by state |

| State charitable registration | Varies by where you solicit |

| Bookkeeping, accounting, and legal review | Varies with complexity, but usually matters more than founders expect |

If your mission is simple and you qualify for the streamlined federal filing, the launch can stay relatively lean. But the cheap version only stays cheap if the entity documents, governance, and compliance calendar are correct the first time. The fix is usually process, not enthusiasm.

Avoid the mistakes that slow new nonprofits down

The same mistakes show up over and over, and they are usually predictable. I see founders spend early energy on a logo, website, and social media presence before the governance and filing structure are even stable. That is backwards. A nonprofit needs legitimacy before it needs polish.

- Choosing the wrong tax-exempt path because the founder wants a charity label without matching the actual mission.

- Writing vague organizing documents that do not clearly support the exemption being requested.

- Letting the board become ceremonial instead of independent, active, and documented.

- Soliciting donations before state registration in places where registration is required.

- Ignoring annual filings until deadlines are missed and penalties start stacking up.

- Assuming exempt status removes tax issues when unrelated business income can still trigger Form 990-T.

The deeper problem is usually the same one: founders think formation is a one-time event, when it is really the start of a compliance rhythm. Once you accept that, the first year becomes much easier to manage.

The first year should feel boring in the right ways

The best nonprofit launches are not dramatic. They are orderly. In the first 90 days, I want the board functioning, the bank and accounting setup complete, the filing calendar visible, and the fundraising rules documented. After that, the work is mostly repetition: keep minutes, track restricted gifts, review program activity against the exempt purpose, and file on time.

- Month 1: finalize the board, adopt bylaws, and set signature authority.

- Month 2: complete state registrations, set up bookkeeping, and define donation acknowledgment procedures.

- Month 3: lock in the annual filing calendar, review any unrelated business activity, and verify public disclosure files are ready.

If you keep the organization boring in that sense, you are doing it right. A nonprofit earns trust by being clear, documented, and consistent long before it becomes large. That is the real answer to launching well: build the structure to support the mission, then let the mission do the work.