Building business credit without leaning on your personal file is possible, but it works only when the company starts looking like a separate financial entity. I break the process into three parts: set up the legal and banking foundation, open accounts that report payment history, and manage those accounts in a way that gives bureaus clean data. This guide explains how to build business credit without using personal credit, where personal credit still shows up, and what to do in the first year so the file actually grows.

The cleanest path is separation, reporting accounts, and disciplined payment behavior

- Form a real business identity first, then separate business banking from personal banking.

- Use vendors, suppliers, and service providers that report to business credit bureaus.

- Pay early or on time every time, because payment history drives the file.

- Expect some lenders to still review personal credit or ask for a personal guarantee at the start.

- Monitor all three major business credit bureaus and correct errors quickly.

What business credit is actually doing for your company

Business credit is the company’s own borrowing profile. It helps suppliers, insurers, and lenders decide whether the business pays on time, carries too much risk, or deserves better terms. I treat it as a reputation file with financial consequences, not as a shortcut around underwriting.

| Area | Personal credit | Business credit |

|---|---|---|

| Identity | Built around your SSN and consumer file | Built around the company’s legal identity, EIN, and bureau records |

| Typical users | Consumers and owners borrowing personally | Vendors, suppliers, insurers, and business lenders |

| What matters most | Payment history, utilization, inquiries, age | Reported trade lines, payment behavior, public records, and profile accuracy |

| Why it matters | Helps you qualify for personal borrowing | Helps the company qualify for terms, cards, and financing on its own merit |

The practical difference is simple: personal credit follows you, while business credit follows the company. If the business starts as a sole proprietorship, that separation stays weak because the entity and the owner are still closely linked. Once that distinction is clear, the next step is making sure the company can be recognized on its own.

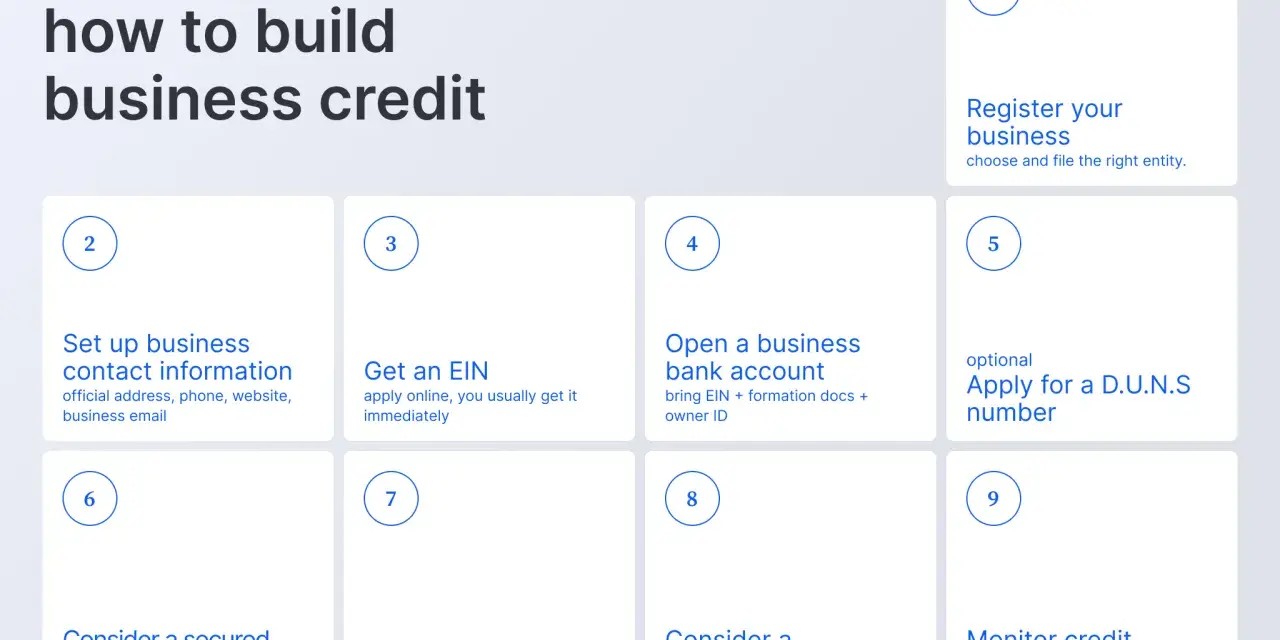

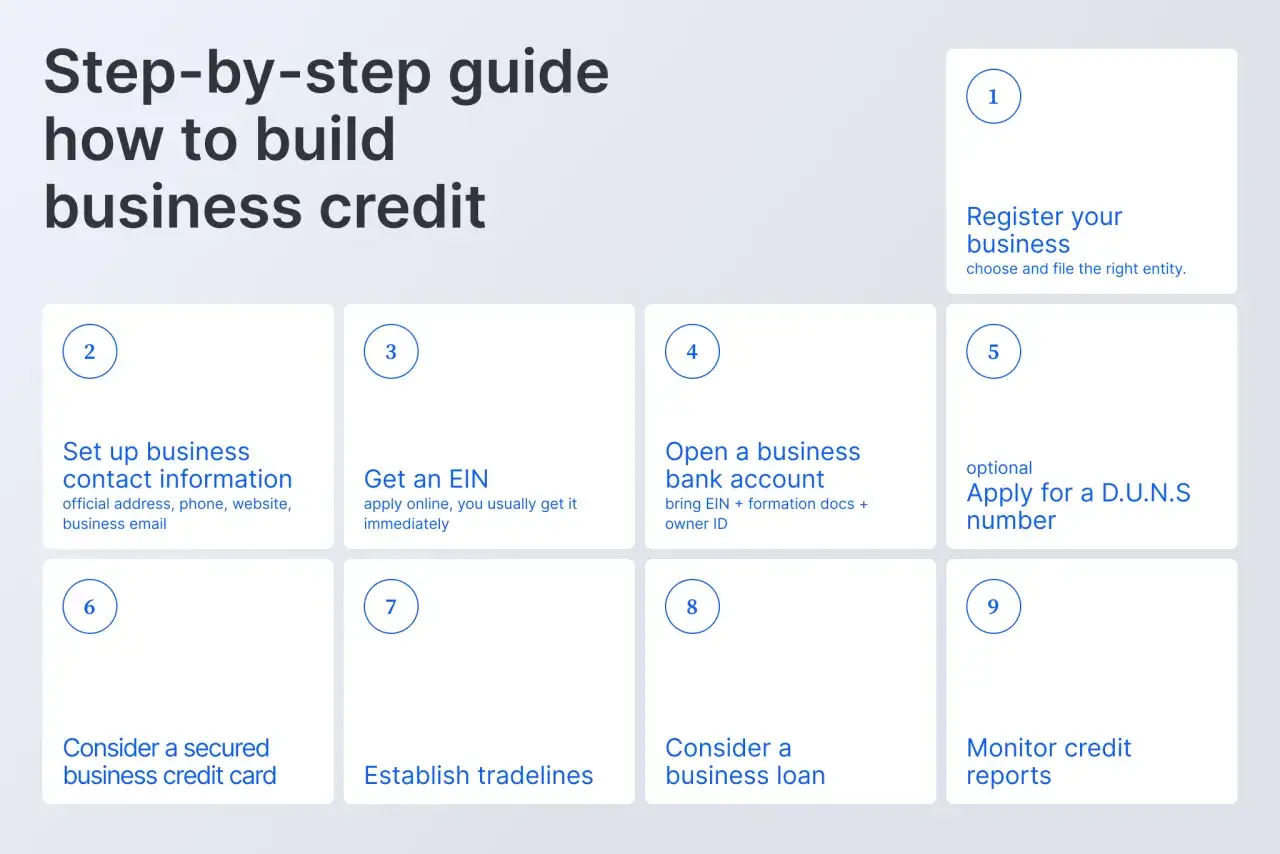

Set up the company so the bureaus can recognize it

I would start here every time, because no amount of good payment behavior helps if the business identity is messy. The SBA is clear that new businesses often still get judged through the owner’s personal credit at the beginning, so the fastest way to reduce that dependence is to make the business look like a real, separate borrower.

- Choose a separate legal entity. An LLC or corporation usually gives you a cleaner separation than a sole proprietorship.

- Get an EIN. Your Employer Identification Number is the tax ID you will use for banking, licensing, and many credit applications.

- Open a dedicated business bank account. This keeps deposits, expenses, and bank references tied to the company instead of your personal checking.

- Keep the business identity consistent. Use the same legal name, address, phone number, and industry classification everywhere.

- Claim your D-U-N-S number if it makes sense for your setup. Dun & Bradstreet still uses it to organize a business credit file, so it can help the company become visible to counterparties that rely on D&B data.

Consistency matters more than most founders think. If your bank account says one thing, your state filings say another, and your vendor application uses a third version of the company name, the bureaus can split the data or miss it entirely. Once the foundation is clean, you can start using accounts that actually report payment history.

Choose accounts that actually report payment history

Not every account helps your file. Some vendors will happily sell you supplies, but unless they report, the account does almost nothing for credit history. I look for reporting relationships first and pricing second, because a cheap non-reporting account is still a dead end for credit building.

| Account type | Best use | Why it helps | Main limitation |

|---|---|---|---|

| Vendor trade account | Office supplies, packaging, basic inventory | Often the easiest entry point and a common way to start reporting trade lines | Only helps if the vendor reports to a bureau |

| Service account | Internet, phone, web hosting, utilities | Useful because everyday operating accounts can create a payment trail | Many providers do not report by default |

| Retail account | Recurring purchases at a specific store | Can add another reporting relationship if the retailer shares data | Use is usually limited to one brand or chain |

| Business credit card or line | Flexible spending and revolving credit | Helps diversify the file once the business is ready | Early-stage approvals often still involve personal credit or a personal guarantee |

A small number of clean, reporting accounts is more useful than a pile of accounts that never show up anywhere. I prefer to start with a few low-risk vendors, make sure they report reliably, and then add stronger forms of credit only after the file has some history. That leads directly to the part most owners miss: how they pay matters as much as what they open.

Paying on time is the floor, not the finish line

Business credit scores reward behavior, and the behavior that matters most is payment discipline. Timely payments are the minimum; early payments can help more with vendors and suppliers that score payment speed, especially in the Dun & Bradstreet ecosystem where the PAYDEX score is built around how reliably a business pays reporting suppliers. I would rather see three boring, perfectly paid accounts than ten accounts that are technically open but constantly pushed to the edge.

- Pay before the due date whenever cash flow allows it. Early payments are safer than “just on time” payments when you are trying to build a reputation.

- Keep balances low and predictable. A clean file is easier to interpret than one that swings wildly from month to month.

- Automate reminders and payments. One missed invoice can damage a relationship that took months to establish.

- Reconcile invoices before paying. If a vendor bill is wrong and you pay it anyway, the error can still be reported.

- Review your business reports regularly. Each bureau can show different data, so do not assume one clean file means all three are clean.

That payment discipline matters, but so does realism about timing and underwriting, because not every lender is ready to ignore personal credit just because the file looks decent.

How long it usually takes before personal credit matters less

There is no honest one-week answer here. In practice, the first reporting accounts may start creating a file within a few billing cycles, but a stronger profile usually takes months, not days. What matters most is whether the business can show consistent identity, consistent payments, and enough history for a lender or supplier to trust the pattern.

- First 30 days: form the entity, get the EIN, open the business bank account, and clean up the company identity.

- 30 to 90 days: open a few reporting vendor or service accounts and make the first payments early.

- 3 to 6 months: check the business credit files, fix errors, and add another reporting relationship if cash flow supports it.

- 6 to 12 months: start looking at better vendor terms, business cards, or revolving products that fit the company’s revenue.

- For bank financing: traditional banks often want good personal credit and roughly two years of business history, while alternative lenders may move faster and accept shorter time in business if revenue is strong.

Personal credit does not disappear overnight, and I would not pretend otherwise. Many unsecured offers still lean on the owner’s creditworthiness or a personal guarantee, especially early on, because the lender wants a second repayment source if the business fails. The cleaner your business history becomes, the less often that fallback gets used.

The mistakes that stall a business file

Most weak business credit files are not the result of bad luck. They are usually the result of sloppy setup, weak vendor selection, or impatience. I see the same mistakes over and over, and they are all fixable.

- Starting as a sole proprietorship and expecting separation anyway. If the business and owner are indistinguishable, the file is harder to build cleanly.

- Using accounts that never report. Operational accounts can help cash flow, but they will not build a credit history if they stay off the bureaus.

- Letting company data drift. A different address, phone number, or legal name across filings can fragment the profile.

- Missing small invoices. A late $150 bill can matter more than the amount suggests because it becomes a data point, not just a payment issue.

- Applying for credit too early. If the file is thin, the lender will often default back to your personal profile anyway.

- Ignoring report errors. If a bureau shows the wrong industry code, address, or payment history, the score can suffer until someone fixes it.

If I had to reduce the entire process to one sentence, it would be this: build a file that looks boring, consistent, and credible to a lender. That is what earns better terms over time, not aggressive application sprees. Once those mistakes are out of the way, the first-year roadmap becomes much easier to follow.

A practical first-year roadmap I would actually follow

When I map this out for a new business, I keep the sequence simple and realistic. The goal in year one is not to impress a bank with a perfect profile, but to give the company enough verified history that future applications are judged on the business first.

- Month 1: form the entity, get the EIN, open the business bank account, and make sure the company name, address, and phone number match everywhere.

- Months 1 to 2: open two or three reporting vendor or service accounts that fit normal operating expenses.

- Months 2 to 6: pay early, automate reminders, and confirm that the payments are actually appearing on the business reports.

- Months 4 to 8: add one stronger revolving product only if the company can support it without stretching cash flow.

- Months 6 to 12: review all three business credit files, correct errors, and use the history you have built to negotiate better terms.