What boards need to know at a glance

- Conflicts are normal; unmanaged conflicts are the real governance risk.

- Disclosure should happen before discussion, not after the vote.

- A conflicted director should usually step out of the room and out of the decision.

- US boards are shaped by different rules, including Delaware corporate law, SEC disclosure, and IRS expectations for charities.

- Documentation is not optional; it is the board’s best defense if the decision is challenged later.

- When the transaction is material or sensitive, independent review is usually the safer path.

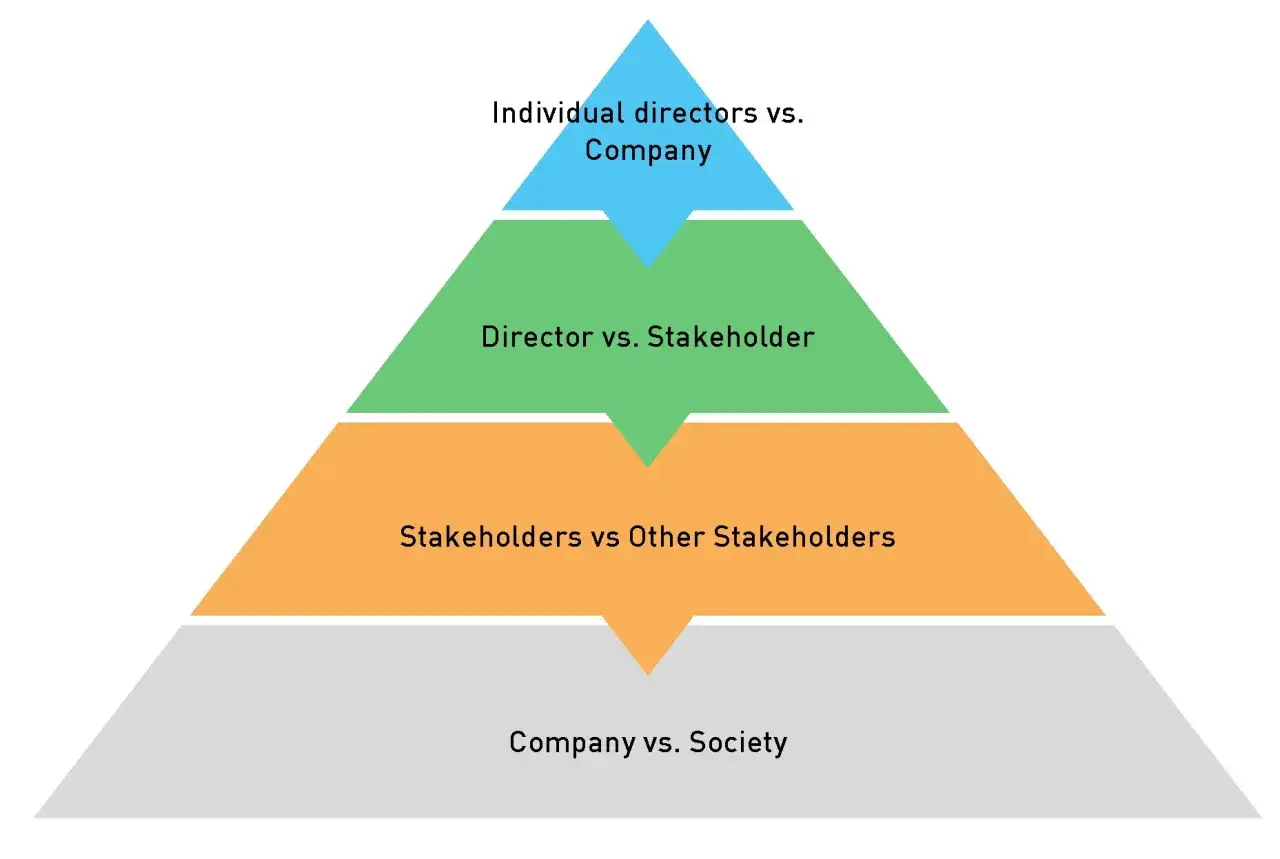

What counts as a real conflict on a board

The cleanest definition is also the most practical: a conflict exists when a director’s personal interest could interfere with, or appear to interfere with, judgment owed to the organization. That personal interest can be direct, like ownership in a vendor, or indirect, like a family member who benefits from the deal.

I usually separate conflicts into three buckets. An actual conflict is already affecting the decision. A potential conflict could become relevant if the transaction moves forward. A perceived conflict may not be illegal or even improper, but it can still weaken trust if the board does not handle it openly.

The important point is that a conflict is not automatically a deal-breaker. For many boards, the issue is not whether the relationship exists, but whether the board has enough distance, disclosure, and independence to make the decision fairly. That distinction matters even more once you start looking at the scenarios that most often trigger problems.

Common conflict scenarios that show up in real boardrooms

Some conflicts are so common that boards start to treat them as routine. That is exactly when they become risky. The more familiar the relationship, the more likely the board is to underestimate how much it affects the process.

- Vendor or consulting contracts - A director owns, advises, or has a financial stake in a company that wants business from the organization. This is one of the most obvious related-party problems because the director can benefit from the board’s own purchasing decision.

- Executive compensation - Directors often review pay, bonuses, severance, and equity awards. If a director is also an officer, founder, or major shareholder, their incentives can tilt the discussion in subtle ways.

- Family employment - Hiring a director’s spouse, child, sibling, or in-law is not automatically prohibited, but it needs careful review. Boards often miss this because the benefit looks indirect at first.

- Corporate opportunities - A board member may learn about a deal, investment, or partnership that should belong to the organization, then pursue it personally or through another company.

- Competitor or investor overlap - A director may serve on multiple boards, hold overlapping equity stakes, or have a relationship with a strategic partner. These cases can be harder to spot, but they matter because they shape loyalty and confidentiality.

The red flag is not just the existence of these ties. It is the point where the board starts assuming the answer before it has tested the facts. From there, the process matters more than anyone wants to admit, which is why the next step is procedural discipline.

How to handle the conflict without damaging the decision

When boards handle conflicts well, the process looks boring on purpose. That is a feature, not a flaw. I prefer a disciplined sequence because it reduces the chance that a single person, even unintentionally, bends the outcome.

- Disclose early and fully - The director should explain the relationship, the financial stake, and any other facts that might affect judgment. Partial disclosure is usually worse than no disclosure because it gives the board a false sense of comfort.

- Stop the process before the deal is shaped - If a conflicted director is helping define the terms, the conflict has already entered the decision-making process. Waiting until the final vote is too late in many cases.

- Recuse the conflicted director - In practical terms, recusal means leaving the discussion, not just abstaining at the end. The board should make the record clear about when the person left and whether they were present for any substantive discussion.

- Use disinterested directors to test the decision - The remaining directors should ask whether the deal is fair, whether alternatives exist, and whether the organization could obtain better terms elsewhere. This is where independence actually shows up.

- Bring in outside help when the stakes are high - Counsel, auditors, compensation consultants, or market data can help the board show that it did not approve the transaction casually. For larger deals, independent support is often worth the cost.

- Document the path, not just the result - Minutes should reflect the disclosure, the recusal, the review process, and the basis for approval or rejection. If the transaction is revisited later, the board should be able to reconstruct the reasoning without guessing.

One nuance that gets missed often: a recusal is not a cure-all if the conflicted director already influenced the negotiation behind the scenes. The board needs a clean process, not just a clean vote. That distinction becomes easier to see once you compare how different US entities are governed.

How the rules change across public companies, nonprofits, and private boards

The underlying governance principle is the same across entity types: put the organization first and manage personal benefit transparently. The legal overlay, however, changes the pressure points.

| Board type | Main pressure point | What I watch for in practice |

|---|---|---|

| Public company | SEC related-person disclosure and independent review expectations | Item 404 disclosure can be triggered by transactions over $120,000, and the company should have a clear policy for review, approval, or ratification of related-person transactions. |

| Nonprofit | Duty of loyalty, private benefit risk, and Form 990 governance questions | The IRS expects a written conflict policy, periodic disclosure, and consistent enforcement. For charities, repeated private benefit can become a serious tax issue. |

| Private company | Corporate law, shareholder trust, and future diligence | Even when there is no SEC filing, the board still needs a process that can survive investor diligence, lender review, or a later dispute among owners. |

If the entity is organized in Delaware, section 144 gives a useful roadmap for interested-director transactions: disclosure of the material facts, approval by disinterested directors or stockholders, or a showing that the transaction is fair to the corporation. In other words, the law does not treat every conflicted transaction as automatically invalid, but it does demand a process that is visible and defensible.

For charities, the IRS is even more explicit about the governance mechanics. It encourages written policies, written disclosures, and consistent monitoring, and it expects boards to show that they are acting solely in the organization’s interest. I see that distinction matter most when a board sits somewhere between mission-driven and commercially active, because the temptation to blur the lines is high.

The practical lesson is simple: the more public the organization, or the more sensitive the transaction, the less room there is for informal judgment calls. That takes us to the part that often decides whether a conflict stays manageable or turns into a board problem.

The documentation that protects the board

Good documentation does not create honesty, but it proves the board had a process. If a conflict is ever reviewed by regulators, donors, shareholders, lenders, or litigators, the minutes and supporting materials often matter as much as the transaction itself.

I would want the file to include these elements:

- A written disclosure from the conflicted director or officer.

- Minutes showing when the disclosure happened and when the person left the discussion.

- Evidence that disinterested directors reviewed the matter independently.

- Comparative pricing, bid results, or market data if the transaction involves money or services.

- A clear approval or rejection rationale tied to the organization’s interests.

- Follow-up monitoring if the transaction is ongoing, recurring, or performance-based.

Boards also do themselves a favor when they keep a standing conflict register or annual disclosure process. It is easier to update one clean record than to reconstruct a year’s worth of relationships from memory. That habit is especially useful when the board is large, geographically dispersed, or full of people who sit on multiple outside boards.

Once those records exist, the remaining question is whether the board is actually willing to use them when a real issue appears.

What I would insist on before approving a conflicted transaction

When a board is close to approving a conflicted matter, I look for a few non-negotiables. If any of them are weak, the board should slow down rather than force the deal through.

- Is the conflict disclosed in writing and in enough detail to understand the stakes?

- Did the conflicted person exit the discussion early enough to avoid shaping the outcome?

- Are the remaining directors truly disinterested, not just technically present?

- Can the board explain why the transaction is in the organization’s best interest, not just why it is convenient?

- Has the board compared the deal against realistic alternatives?

- Would the record still look disciplined if it were reviewed a year from now?

If the answer to any of those questions is shaky, I would rather see the board bring in counsel, re-open the review, or walk away than approve something it cannot defend later. The best-managed conflicts are rarely the most aggressive ones; they are the ones where everyone can see that the board stayed objective, documented its reasoning, and protected the organization’s interests first.