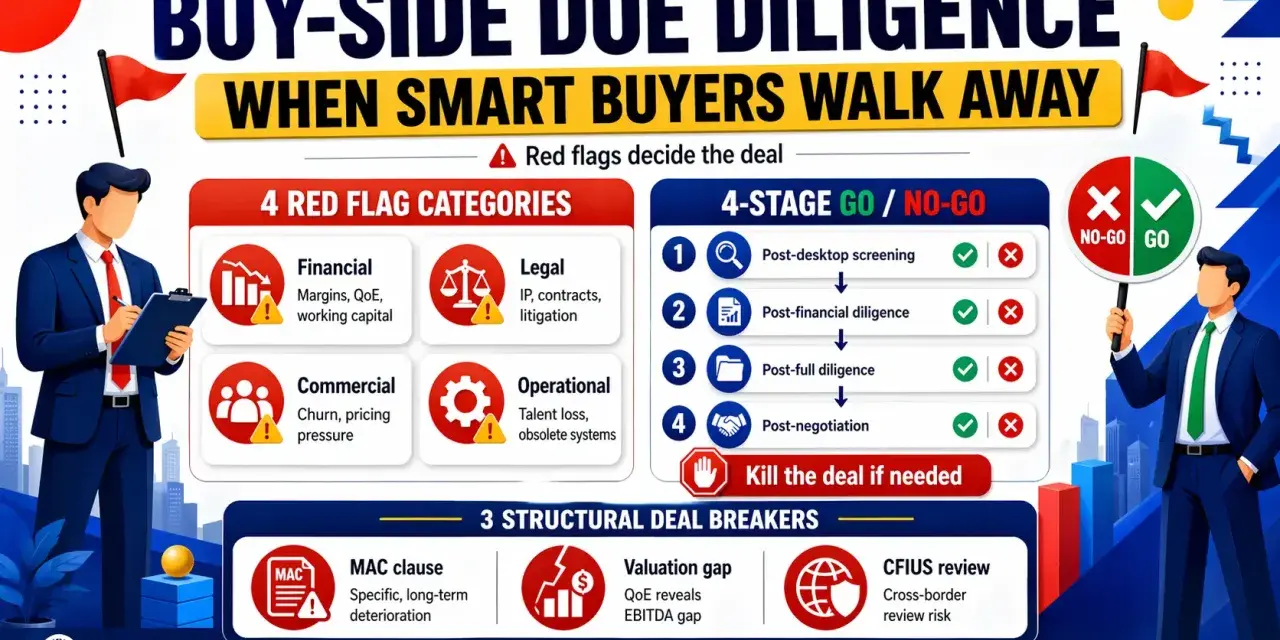

A strong due diligence checklist is not a formality; it is the fastest way to find out whether a transaction, vendor relationship, or strategic decision is built on solid ground. In U.S. risk and compliance work, the real task is to verify ownership, authority, contracts, money flows, disputes, regulatory exposure, cyber controls, and the people who can actually bind the business. This guide breaks that review into a practical sequence so you can spot red flags early and decide whether to proceed, renegotiate, or stop.

Use the review to separate clean deals from quiet risk

- Focus first on ownership, authority, and source of funds before you spend time on softer issues.

- Check the financial story, but do not ignore contracts, taxes, leases, and off-balance-sheet obligations.

- Compliance screening should cover sanctions, anti-bribery risk, privacy, cyber, and third-party exposure.

- Not every issue is a deal breaker; the point is to separate hard stops from fixable problems.

- Document what you found and what was resolved, because the paper trail matters later.

What a due diligence checklist should prove before you move forward

I usually treat diligence as a proof exercise. The question is not whether a seller, target, or vendor sounds credible in a meeting; the question is whether the records, signatures, controls, and financial facts back up the story. A good review should tell you three things fast: who really controls the entity, what obligations are already attached to it, and whether the business can operate without hidden legal or compliance problems.

| Area | What you are trying to prove | Why it matters |

|---|---|---|

| Ownership and control | The entity, its beneficial owners, and the people who can sign or direct it | Prevents hidden control issues, nominee structures, and authority disputes |

| Economics | Revenue quality, margin pressure, debt, taxes, and working capital | Shows whether the value is real or inflated by timing and accounting noise |

| Contracts and obligations | Key customer, supplier, lease, debt, and indemnity terms | Reveals change-of-control risk, termination rights, and surprise liabilities |

| Compliance exposure | Sanctions, anti-bribery, privacy, cyber, AML, licensing, and litigation history | Identifies issues that can trigger enforcement, loss of access, or remediation cost |

That is why I do not like huge, generic document requests with no priorities attached. A useful review is risk-based: start with the items that can stop the deal, change the price, or force a post-close cleanup. Once you know what proof you need, the next question is who is standing on the other side of the table.

Start with the parties, ownership, and authority

If the counterparty is not clean at the front end, everything that follows gets more expensive. I start with legal identity, formation documents, ownership structure, and signing authority. For covered financial institutions, beneficial ownership checks are especially important, and that often means identifying owners at 25% or more plus a control person. Even outside the banking context, I want to know who ultimately benefits, who can approve the deal, and whether any person in the chain is hiding behind a shell, a nominee, or an inconsistent story.

- Confirm the exact legal name, entity type, jurisdiction, and status in good standing.

- Identify ultimate owners, controllers, and any related parties that may influence decisions.

- Verify who can sign, who can approve, and whether board or member consent is required.

- Screen principals for sanctions, watchlists, criminal matters, and regulatory actions.

- Check for conflicts of interest, especially where family ties or side businesses are involved.

- Ask whether the entity uses intermediaries, nominees, or consultants to move money or make decisions.

When the ownership chart looks tidy but nobody can explain the business rationale behind a related-party payment, I slow down. That is not just a documentation issue; it is often a governance signal. After the people and authority checks pass, I move to the economic reality hiding in the papers.

Verify the numbers, contracts, and hidden obligations

This is where a lot of people get distracted by polished financial statements and miss the harder questions. A business can look healthy on paper and still be sitting on liabilities that will surface only after closing: a lease with a bad renewal clause, a supplier agreement that can be terminated on short notice, a tax exposure that was never booked, or an indemnity that shifts risk in a way the valuation never reflected. I want the numbers, but I want the contracts that explain the numbers even more.

| Document set | What to inspect | Common red flag |

|---|---|---|

| Financial statements | Revenue quality, margin trends, cash flow, working capital, one-time items | Margins that depend on unusual timing or accounting adjustments |

| Debt and liens | Loans, covenants, guarantees, UCC filings, collateral pledges | Hidden defaults or assets already tied up elsewhere |

| Material contracts | Change-of-control clauses, exclusivity, pricing resets, termination rights | A key customer or supplier can walk away after the transaction |

| Tax and payroll | Filed returns, nexus, withholding, sales tax, wage and classification issues | Unpaid taxes or worker classification problems that never hit the P&L cleanly |

| Insurance and claims | Coverage limits, exclusions, deductibles, open claims, lapse history | Policies that do not actually cover the most likely loss scenario |

I also look for concentration risk. If a small number of customers, vendors, or channels drive most of the business, the transaction is more fragile than the headline revenue suggests. That leads naturally into the compliance layer, because many deal surprises are legal before they are financial.

Run the compliance lens across the business

Compliance checks are not a box-ticking exercise. They are the part of the review that tells you whether the business has been operating within the rules that matter most in the United States: anti-bribery, AML, sanctions, privacy, cyber, labor, and industry licensing. In 2026, I would treat third-party risk and data controls as first-class diligence items, not add-ons.

Anti-bribery and third parties

Foreign agents, consultants, distributors, and lobbyists deserve more scrutiny than most teams give them. If the business cannot explain why a third party was hired, how it was paid, what services it provided, and who approved the relationship, I assume the risk is unresolved. The practical question is not whether a policy exists; it is whether the policy is enforced, tested, and reflected in actual payments and approvals.

Data, cyber, and privacy

If the business handles customer, employee, or transaction data, I want to know what was collected, where it is stored, who can access it, and whether the incident response plan has been tested. A prior breach is not automatically fatal, but it changes the conversation. I want the scope of exposure, the remediation taken, whether any notices or regulatory steps were triggered, and whether the same weakness still exists somewhere in the stack.

Competition and antitrust

In pre-merger work, the information flow itself can create risk. The FTC advises sharing the least amount of competitively sensitive information needed for diligence, which is why clean teams, redaction, and careful access controls still matter when competitors are involved. That is one of those areas where process discipline protects the deal as much as legal analysis does.

Read Also: Due Diligence: Separate Promises from Proof - Your Guide

Third-party vendors

Vendor diligence needs to be ongoing, not front-loaded and forgotten. FINRA's 2026 oversight report makes the point clearly: firms should keep doing initial and ongoing checks on mission-critical providers, validate contract controls, maintain inventories of vendor services and data access, test incident response, and make sure access is revoked at offboarding. Even outside financial services, that is a strong model for any company that depends on outside systems, data processors, or managed services.

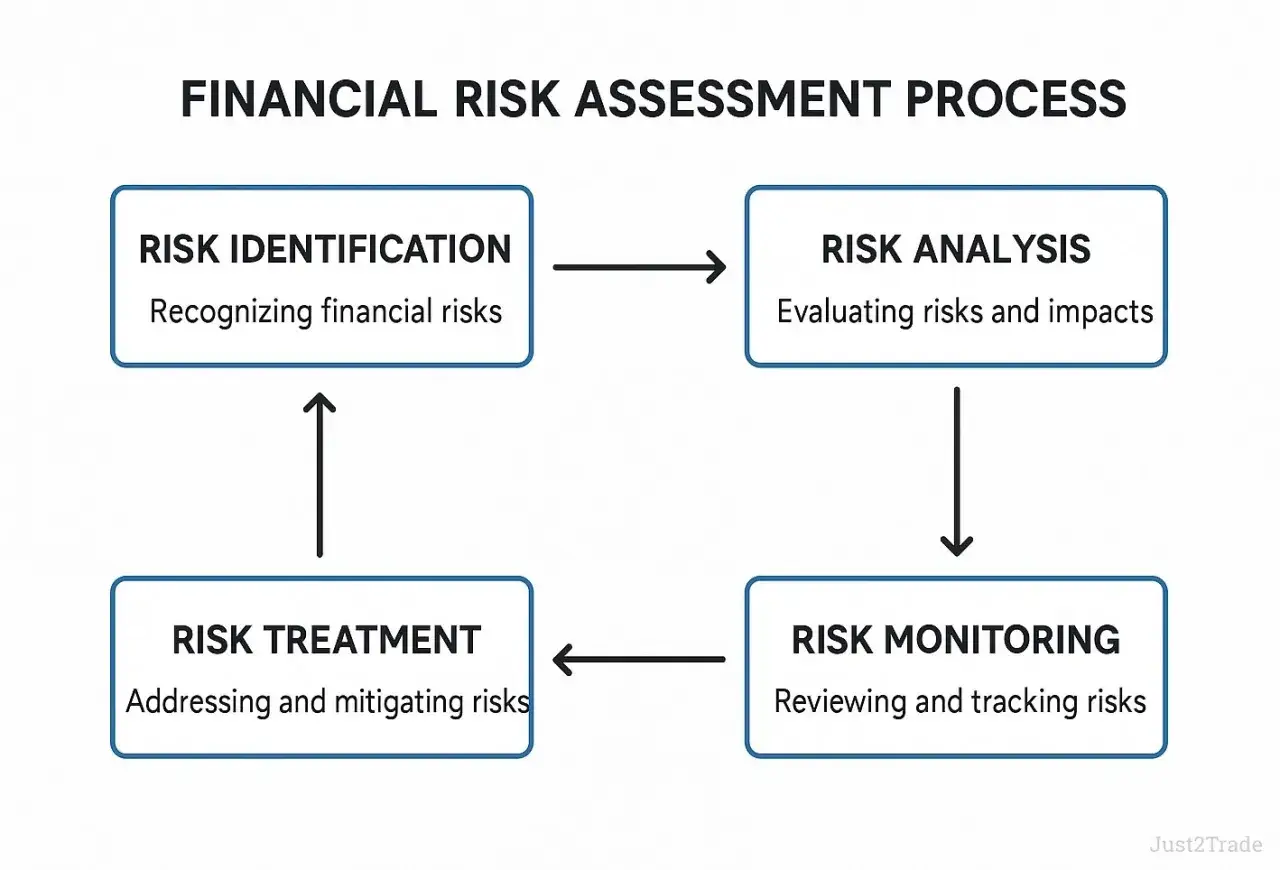

If the compliance layer looks uneven, I do not try to force it into a generic risk score. I map it to the way the transaction could actually fail, and then I decide whether the issue is a hard stop, a pricing issue, or a cleanup item that can be handled after closing.

Turn findings into decisions, not just notes

The biggest mistake I see is collecting information without converting it into an action. A review only helps if someone decides what happens next. I like to separate findings into three buckets: hard stops, items that change the economics, and issues that can be fixed after signing or closing. That keeps the team from arguing about every issue as if every issue is equally serious.

| Finding | Typical response | Why |

|---|---|---|

| Missing authority or false signature trail | Pause and verify before any commitment | You may not even have a valid deal path |

| Material lawsuit, sanction hit, or bribery concern | Hard stop until counsel reviews the facts | The downside can exceed the value of the transaction |

| Weak contract protection or vendor security gap | Negotiate indemnity, escrow, remediation, or better terms | The risk may be manageable if it is priced and documented |

| Missing policy, minor control gap, or incomplete file | Close with a written remediation plan | Annoying, but usually fixable if the risk is low |

- Rank each issue by severity and likelihood.

- Assign an owner and a deadline for every unresolved item.

- Document the evidence, not just the conclusion.

- Escalate anything that affects legality, authority, or reputation.

- Tie remedies to the transaction documents or vendor contract.

I also like a 30/60/90-day remediation plan when the deal can still move forward. That gives the business a realistic path to fix what is fixable without pretending the issue does not matter. The last step is making sure the review leaves a trail the board, counsel, or buyer can actually use.

What I would not skip in a U.S. risk review

If I had to trim the process, I would not cut the ownership check, the contract review, or the compliance review. Those three areas reveal most of the problems that later become expensive. I would also avoid one-time diligence that is never refreshed, especially when the relationship continues after closing or the vendor handles sensitive systems.

- Keep the data room clean and limited to people who actually need access.

- Ask for source documents, not just summaries or management assurances.

- Update the review if the deal pauses, the price changes, or new facts surface.

- Preserve a clear record of what was found, what was accepted, and what was fixed.

In practice, the best diligence process is not the longest one. It is the one that forces a clear yes, no, or renegotiate decision based on facts that can stand up later. That is what makes the review useful in a real transaction, not just impressive in a folder.