The right anti-money laundering stack is not just a screening tool with a few rules bolted on. It should help compliance teams detect risk earlier, document decisions cleanly, and keep pace with changing U.S. expectations without creating a flood of noise. In practice, I think the best AML solutions are the ones that make judgment easier, not the ones that simply generate more alerts.

What matters most in a modern AML stack

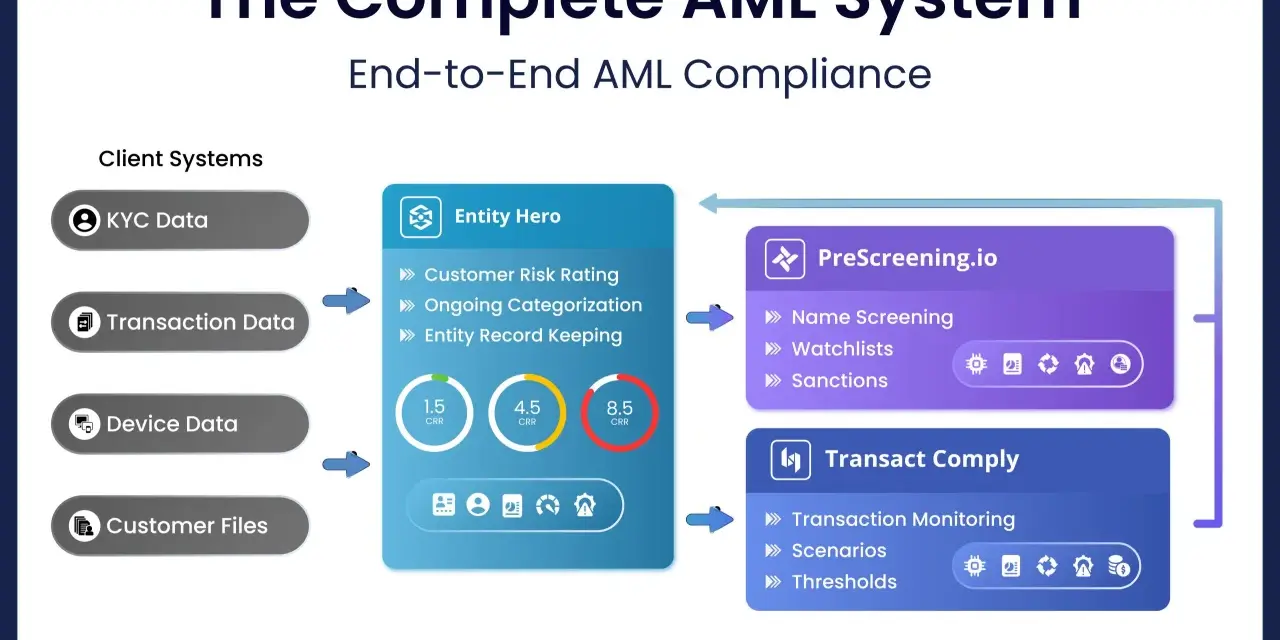

- Coverage matters more than features. Screening, transaction monitoring, customer due diligence, and case management need to work together.

- Risk-based design is non-negotiable. A small fintech and a multi-branch bank should not run the same controls in the same way.

- Data quality drives performance. Weak entity data and poor normalization can create false positives faster than any rule can fix.

- Explainability is a compliance requirement, not a luxury. Reviewers should be able to see why an alert fired and why it was closed.

- Implementation is where many projects fail. Threshold tuning, governance, and training matter as much as the software itself.

What modern AML platforms actually cover

When people talk about AML technology, they often picture one tool. In reality, the job is a chain of controls: onboarding checks, ongoing screening, transaction monitoring, investigation workflows, and reporting. I prefer to think of it as a compliance operating system, because each piece weakens the whole if it is isolated.

| Capability | What it does | Where it usually breaks down |

|---|---|---|

| Customer screening | Checks customers and counterparties against sanctions, watchlists, and internal risk markers | Poor matching logic creates too many false positives or misses weak aliases |

| Transaction monitoring | Flags unusual patterns across payments, transfers, cash movement, and account behavior | Static rules miss changing typologies; overly broad rules bury analysts in noise |

| Customer due diligence | Builds and refreshes the risk profile used for onboarding and periodic review | Profiles become stale when business activity changes but the model does not |

| Case management | Tracks reviews, supporting evidence, escalation, and disposition | Weak workflows turn investigations into email trails with no auditability |

| Reporting and recordkeeping | Supports suspicious activity reports, currency transaction reports, audit logs, and internal documentation | Missing rationale or incomplete records become a problem during exams |

The practical test is simple: if the platform cannot connect these functions into a defensible review path, it is only solving part of the problem. That matters even more once volume grows, which is why the next question is not what a tool can do, but what regulators expect it to prove.

Why risk-based design matters more than feature count

In the United States, AML programs are built around risk, not around a fixed list of software features. The core expectation is that the institution understands its products, customers, geographies, delivery channels, and transaction patterns, then designs controls that fit that profile. A retail bank, a fintech with instant payments, and a private wealth platform all face different threat models, so their monitoring logic should look different too.

That point is becoming sharper, not softer. Regulators are moving toward a more effectiveness-based posture, which means the program has to demonstrate that it works in practice, not just that it exists on paper. For a buyer, that means the vendor must help you show how alert thresholds, scenarios, and review workflows map to your actual risk assessment.

Corporate transparency and beneficial ownership data are also still shifting, so the data layer needs to tolerate rule changes without a redesign. If the platform breaks every time reporting logic changes, it will create more work than value.

When I evaluate a platform, I ask a few blunt questions: Can it explain its matches? Can it show why a scenario is still relevant? Can we adjust behavior quickly when a new typology appears? If the answer is no, the software may still look modern, but it will be weak where it counts.

- Risk assessment should drive configuration. The reverse is a common mistake.

- Documentation must survive an exam. “The vendor said so” is not a control.

- Human review still matters. Automation helps, but it does not replace judgment.

That leads naturally to the feature set that actually changes outcomes, because the best-designed program still depends on the right operational tools.

Which features actually reduce compliance risk

Not every feature deserves equal weight. The items below tend to matter most when the goal is real risk reduction rather than a flashy demo.

| Feature | Why it matters | What good looks like |

|---|---|---|

| Entity resolution | Combines records for the same person or business across systems | Matching rules that understand aliases, ownership changes, and data variations |

| Scenario tuning | Keeps monitoring aligned with current typologies and customer behavior | Documented tuning with approval, testing, and rollback logic |

| Analyst workflow | Speeds case review and preserves rationale | One place to see alerts, evidence, notes, and disposition history |

| Model governance | Shows that thresholds and logic are controlled, not ad hoc | Versioning, change logs, validation, and periodic review |

| Integration depth | Feeds the system with accurate data from core, payments, onboarding, and CRM systems | Clean data pipelines with clear ownership for upstream fixes |

| Audit trail | Makes decisions defensible after the fact | Time-stamped records that show who reviewed what and why |

The most overrated feature is usually the one buyers can see in a demo but barely use in production. The most underrated one is often data normalization, because bad formatting, duplicate identities, and missing fields can ruin even a strong monitoring model. A platform that handles messy inputs well is usually more valuable than a platform that simply has more checkboxes.

How to choose between SaaS, managed services, and internal build

There is no universal answer here. The right model depends on your transaction volume, team size, internal technical depth, and how quickly you need to scale. I usually separate the decision into three practical paths.

| Model | Best fit | Strengths | Tradeoffs | Typical cost profile |

|---|---|---|---|---|

| SaaS platform | Most banks, lenders, and fintechs that want speed and predictable operations | Faster deployment, vendor maintenance, regular updates | Less customization, possible vendor lock-in | Often starts in the low five figures annually and can rise into six figures as volume, data feeds, and modules expand |

| Managed service | Teams that need analyst support or do not want to staff every review function internally | Operational help, faster coverage, easier scaling | Less direct control, recurring service dependency | Usually software plus service fees, with costs rising quickly as case volume grows |

| Internal build | Large or highly specialized firms with strong engineering and compliance governance | Full control, deeper fit with proprietary data | Longest timeline, highest maintenance burden | Highest total cost once engineering, validation, and support are included |

As a rule of thumb, a focused SaaS deployment can often go live in about 6 to 12 weeks if the data is clean and the scope is narrow. Broader programs with multiple lines of business, historical lookbacks, or heavy integrations usually need 3 to 6 months before the controls feel stable. The difference is rarely just technology; it is almost always data readiness and governance.

That is also where budgets get distorted. Teams often price the subscription and forget the implementation work, scenario tuning, backfills, QA, and training that decide whether the tool works in real life. If those pieces are not scoped early, the program ends up looking cheap on paper and expensive in operation.

Common mistakes that create false confidence

Some of the worst AML programs are not obviously broken. They are simply noisy, slow, and hard to defend. On the surface they produce alerts, cases, and reports. Underneath, they do not improve decision quality.

- Using static rules forever. A rule that made sense last year can become a blind spot after customer behavior or payment patterns shift.

- Ignoring feedback from analysts. If investigators keep closing the same type of alert, that is a tuning signal, not a housekeeping issue.

- Separating onboarding from monitoring. A risk score that never influences monitoring logic is mostly decoration.

- Letting data defects linger. Duplicate customers, missing identifiers, and inconsistent names create avoidable noise.

- Overlooking testing and validation. A vendor model still needs evidence that it works for your portfolio.

- Buying for audit optics only. A tool that looks impressive in a board deck may still be weak in production.

The fix is not more alerts. It is better governance around why alerts exist, how they are reviewed, and what gets changed when outcomes are poor. That is the practical bridge to a stronger rollout, which is where most programs either become credible or stall.

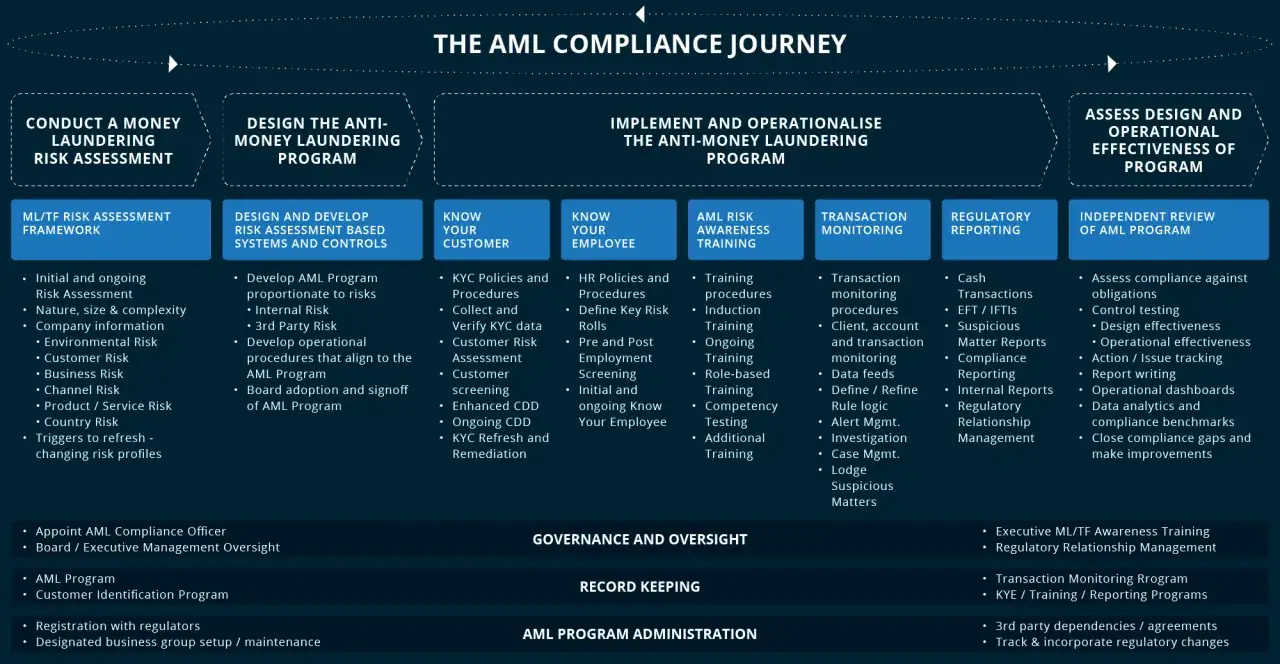

What a strong rollout looks like in 2026

A good implementation is methodical, not flashy. The sequence below is the one I would trust for most U.S. institutions.

- Start with a current risk assessment that reflects products, customers, geographies, and channels.

- Map the data sources before configuring scenarios, because bad inputs are hard to fix later.

- Define what success means using measurable metrics such as alert precision, false positive rate, case turnaround time, and SAR timeliness.

- Run a controlled pilot, then tune thresholds and logic using documented evidence.

- Train analysts and approvers on the reasons behind the rules, not just the mechanics of clicking through a case.

- Schedule independent testing so the program is validated by someone who is not the original builder.

My practical benchmark is simple: the system should help the team close more meaningful cases with less wasted effort, while still leaving a clean audit trail. If a deployment raises volume but not quality, it is not a win. If it reduces noise but weakens detection, that is worse.

When I review AML solutions, I look for evidence that the platform improves judgment, not just throughput. The best ones are not the loudest; they are the ones that make compliance work clearer, faster, and more defensible when the questions get hard.