When I explain what are internal controls, I keep the answer simple: they are the rules, checks, and responsibilities that keep accounting data accurate, protect assets, and make fraud or error easier to catch. In practice, they show up in invoice approvals, cash handling, reconciliations, and user access reviews. This article breaks down how internal controls work in accounting, which ones matter most, and how they fit U.S. governance and reporting expectations.

The practical version of internal controls in accounting

- Internal controls are the procedures that help a business safeguard assets, keep records reliable, and run its accounting process with fewer mistakes.

- The strongest control systems combine preventive, detective, corrective, and compensating controls instead of depending on just one type.

- In U.S. accounting, COSO is the most common reference point, and its framework organizes control around five components and 17 principles.

- Controls matter most in the high-risk parts of the finance cycle: cash, vendor setup, payroll, journal entries, and month-end close.

- A policy on paper is not enough; what matters is whether the control actually runs, leaves evidence, and catches the right risk on time.

What internal controls actually do in accounting

In an accounting setting, internal controls exist to do three jobs at once: protect assets, keep financial reporting reliable, and make operations more efficient. I usually think of them as the guardrails around money and data. A good control does not just stop theft or catch errors after the fact; it also reduces confusion, speeds up review, and makes month-end close less painful.

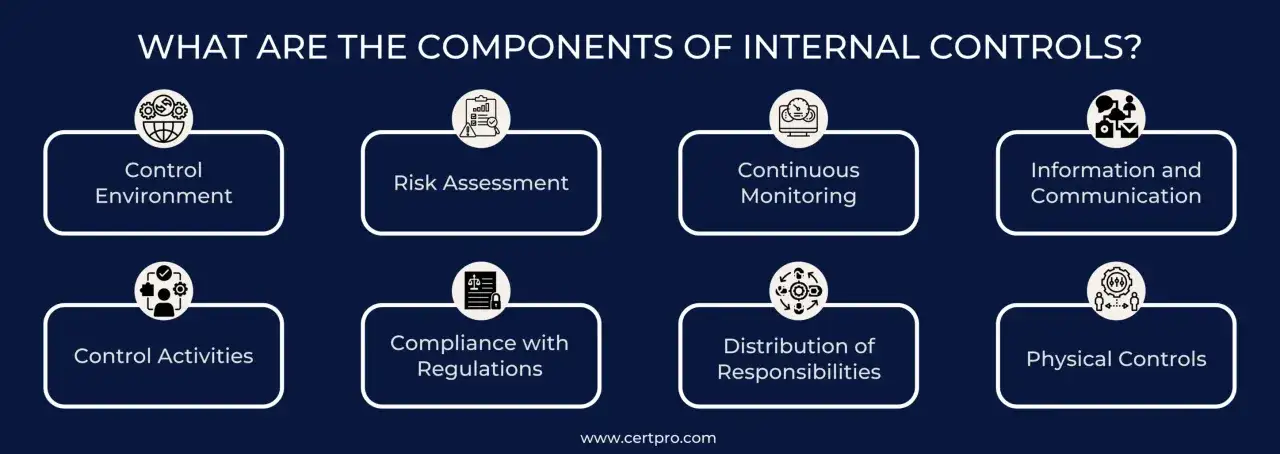

COSO’s framework is useful here because it reminds you that control is not only about compliance. It is built around five components: control environment, risk assessment, control activities, information and communication, and monitoring. Those pieces work together. If the tone at the top is weak, even well-written procedures tend to drift. If monitoring is weak, the same mistake can repeat for months before anyone notices.

There is one concept that matters more than most people expect: reasonable assurance. Internal controls reduce risk, but they do not eliminate it. That is important because accounting teams sometimes treat controls as if they should make every error impossible. That expectation is unrealistic and usually leads to frustration. The better goal is to make significant errors hard to commit, easier to detect, and more expensive to hide. Once that idea is clear, the next step is choosing the right kind of control for the risk you are trying to manage.

The control types I would use first in a finance function

Good accounting control design is usually a mix of four types. The label matters less than the function, but the mix matters a lot. If a process relies only on detective controls, problems are found late. If it relies only on preventive controls, it can become slow and rigid. The point is balance.

| Control type | What it does | Common accounting example | Where it works best |

|---|---|---|---|

| Preventive | Stops an error or misuse before it happens | Approval limits for payments, restricted system access, three-way match before invoice payment | High-risk transactions and access-sensitive processes |

| Detective | Finds mistakes after the transaction has happened | Bank reconciliations, variance reviews, exception reports | Processes where review is cheaper than blocking every transaction upfront |

| Corrective | Fixes the issue and reduces the chance of repeat failure | Adjusting entries, password resets after role changes, process remediation after a failed test | Anywhere a control failure has already shown up and needs remediation |

| Compensating | Offsets a weakness when the ideal control is not possible | Extra supervisory review when one person handles a small process alone | Smaller teams and temporary staffing gaps |

In practice, preventive controls are strongest when the risk is severe, like unauthorized payments or incorrect bank access. Detective controls are often the workhorses of accounting because they are practical and scalable. Corrective and compensating controls matter because real finance teams rarely operate in perfect conditions. People leave, systems change, and the process still has to run. That reality becomes clearer when you look at the controls that protect the daily accounting cycle.

Day-to-day examples that protect cash, revenue, and the close

The best way to understand accounting controls is to look at where money moves. That is where risk is concentrated, and that is where a control failure becomes visible fast.

Cash and banking

Cash should never be handled as if trust alone is enough. I want bank reconciliations prepared monthly, reviewed by someone independent of cash posting, and cleared items explained rather than waved through. If a company has meaningful volume, I also want positive pay or equivalent bank-side protection. These controls matter because cash is liquid, fast-moving, and hard to recover once it disappears.

Payables and vendor setup

Accounts payable is one of the easiest places for fraud and error to hide. A strong process separates vendor creation, invoice approval, and payment release. The three-way match between purchase order, receiving record, and invoice is still one of the most practical controls in accounting because it catches overbilling, duplicate invoicing, and orders that were never received. Vendor master changes deserve extra review because fake or altered vendor records are a classic weak point.

Revenue, receivables, and credit

Revenue controls should make sure sales are recorded only when the underlying event has occurred and the supporting evidence exists. That means checking contract terms, shipment or service completion, and any returns or credits. On the receivables side, aging reports and collection reviews help spot accounts that are drifting out of range. The goal is not just accuracy; it is also early warning. If receivables are slipping, the control should show that before the close turns into a rescue mission.

Payroll and employee changes

Payroll is sensitive because it combines people data, payment processing, and timing pressure. I expect controls around new hires, terminations, rate changes, and overtime approval. A company should also review payroll master files for unusual changes and restrict who can edit employee records. Payroll fraud often begins with a simple access problem, not a complex scheme.

Read Also: P&L Meaning - How to Read a Profit and Loss Statement

Month-end close and journal entries

Month-end close is where many accounting problems either get caught or quietly rolled forward. I like controls over journal entry approval, late adjustments, account reconciliations, and unusual manual postings. Manual journal entries deserve extra scrutiny because they can bypass normal process logic. If a team can explain every large or unusual entry in plain language, the close is usually in better shape than if it depends on vague review notes.

These controls sound basic, but in accounting basics are where losses and misstatements usually start. The real failure is rarely a missing policy; it is a process that looks controlled on paper and feels loose in practice.

Why controls fail even when the policy looks fine

Most control failures come from a handful of predictable problems. The first is segregation of duties failure, where one person can initiate, approve, and record the same transaction. The second is stale review, where reconciliations or approvals happen too late to matter. The third is access creep, where employees keep permissions long after their role changed.

- One person can create, approve, and pay a transaction.

- Reconciliations are done, but nobody clears the exceptions.

- System access is never reviewed after promotions, transfers, or terminations.

- Controls exist, but the team cannot produce evidence that they were performed.

- Exception reports are generated automatically and ignored automatically.

- People rely on spreadsheets without version control or review discipline.

There is also a distinction that matters in audits and governance discussions: a control can be well designed and still fail in operation. That is the difference between design effectiveness and operating effectiveness. A control may look reasonable in a policy document, but if it is not performed consistently, it does not protect the company in the real world. The SEC also treats severe issues seriously enough that a combination of deficiencies can rise to a material weakness, which changes how management can describe the control environment.

Once you know how controls break, building them becomes a design problem rather than an abstract accounting debate.

How to design controls that hold up under pressure

When I help shape a control structure, I start with the process, not the policy. The best controls are tied to a specific risk, owned by a named person, performed on a defined schedule, and supported by evidence that someone else can review.

- Map the process from start to finish so you can see where money, data, and approvals actually move.

- Identify the highest-risk points, especially where someone could misstate balances, move cash, or override a check.

- Choose the lightest control that still meaningfully reduces the risk, rather than piling on approvals that nobody reads.

- Assign one owner, one frequency, and one evidence standard for each key control.

- Build in review and exception handling so the control does something with the problems it finds.

- Test the control periodically and update it when systems, staffing, or transaction volume changes.

Automation helps, but only when the underlying logic is sound. In 2026, many accounting processes run through cloud ERPs, payroll systems, and payment platforms, so IT access and change controls are part of the accounting control story whether teams label them that way or not. If a system lets the wrong person edit master data or post unsupported entries, the accounting process inherits that weakness immediately. That is why control design and technology design now belong in the same conversation.

That design work becomes especially important once U.S. reporting obligations enter the picture.

What U.S. reporting rules change for public companies

For U.S. public companies, internal controls are not just a management preference. They connect directly to SEC reporting expectations and, for many issuers, to Sarbanes-Oxley Section 404. Management must assess internal control over financial reporting, and if there is one or more material weakness, management cannot conclude that the system is effective.

That rule changes behavior in a useful way. It pushes companies to document the framework they use, test controls with some discipline, and disclose material weaknesses instead of pretending the issue is minor. COSO remains the common framework because it gives management and auditors a shared language for evaluation. That shared language matters when boards, auditors, and finance teams need to discuss not just whether a control exists, but whether it actually works.

- Public companies generally need a formal ICFR assessment.

- Material weaknesses must be disclosed when identified.

- Auditor attestation is part of the reporting structure for many issuers.

- Private companies may not face the same disclosure burden, but lenders, investors, and boards still expect disciplined controls.

Even where the law is less demanding, the business case remains the same. Reliable accounting supports financing, due diligence, tax work, and strategic decision-making. If the books are fragile, everything built on top of them becomes fragile too. That is why I usually finish with the question of where to begin if the company cannot fix everything at once.

If I were tightening a finance function this quarter, I would start here

I would not start with software. I would start with the few controls that protect the most exposed parts of the ledger and cash flow. In most small and mid-sized companies, that means bank reconciliations, vendor master access, payment approvals, journal entries, and month-end review of unusual balances.

- Require monthly bank reconciliations with documented review and exception follow-up.

- Separate vendor setup from invoice approval and payment release wherever staffing allows.

- Review who can post journal entries, edit master data, and approve payments.

- Use an approval matrix with clear dollar thresholds so decisions are not improvised.

- Track outstanding reconciling items, not just the reconciliations themselves.

If a company gets those five areas right, most of the rest becomes easier to manage. The real goal is not control theater; it is a system that makes errors harder to miss, fraud harder to hide, and reporting easier to trust.