Invoices and payments sit at the center of accounting because they turn day-to-day business activity into cash flow, liabilities, and records you can actually trust. In practice, I treat them as the point where billing, approval, settlement, and reconciliation all meet, which is why small mistakes there tend to create larger problems later. This article breaks down how the cycle works in a U.S. accounting context, what to watch for, and how to keep the process clean without overcomplicating it.

The parts of the process that matter most before cash moves

- Invoices create the claim and payments settle it, but accounting has to track both sides separately.

- Accounts receivable and accounts payable need different controls, metrics, and follow-up rhythms.

- Payment terms affect cash flow more than most people expect, especially when disputes or partial payments appear.

- Matching and reconciliation are what keep the general ledger accurate after money changes hands.

- Automation helps, but only when the underlying approval and coding rules are already sound.

What the billing side of accounting actually covers

At a basic level, an invoice is a request to pay, while a payment is the settlement of that request. That sounds obvious, but in accounting the separation matters: one document creates the obligation, the other closes it. I usually explain it this way to teams: the invoice belongs to the transaction record, the payment belongs to the cash record, and the books need both views to stay reliable.

In a U.S. business, the invoice often carries details such as the customer or vendor name, service dates, line items, tax treatment, payment terms, due date, and reference numbers like purchase orders. Those details are not decoration. They determine whether the item can be approved, posted, matched, and collected without back-and-forth. When the invoice is unclear, the payment usually slows down, and the delay often shows up later as an aging problem or a reconciliation issue.

This is also where the two sides of the ledger start to diverge. A sales invoice usually creates accounts receivable, which is money customers owe you. A vendor bill creates accounts payable, which is money you owe someone else. Once that distinction is clear, the rest of the workflow becomes much easier to design.

With that foundation in place, the next step is to look at how the cycle actually moves from document to settled cash.

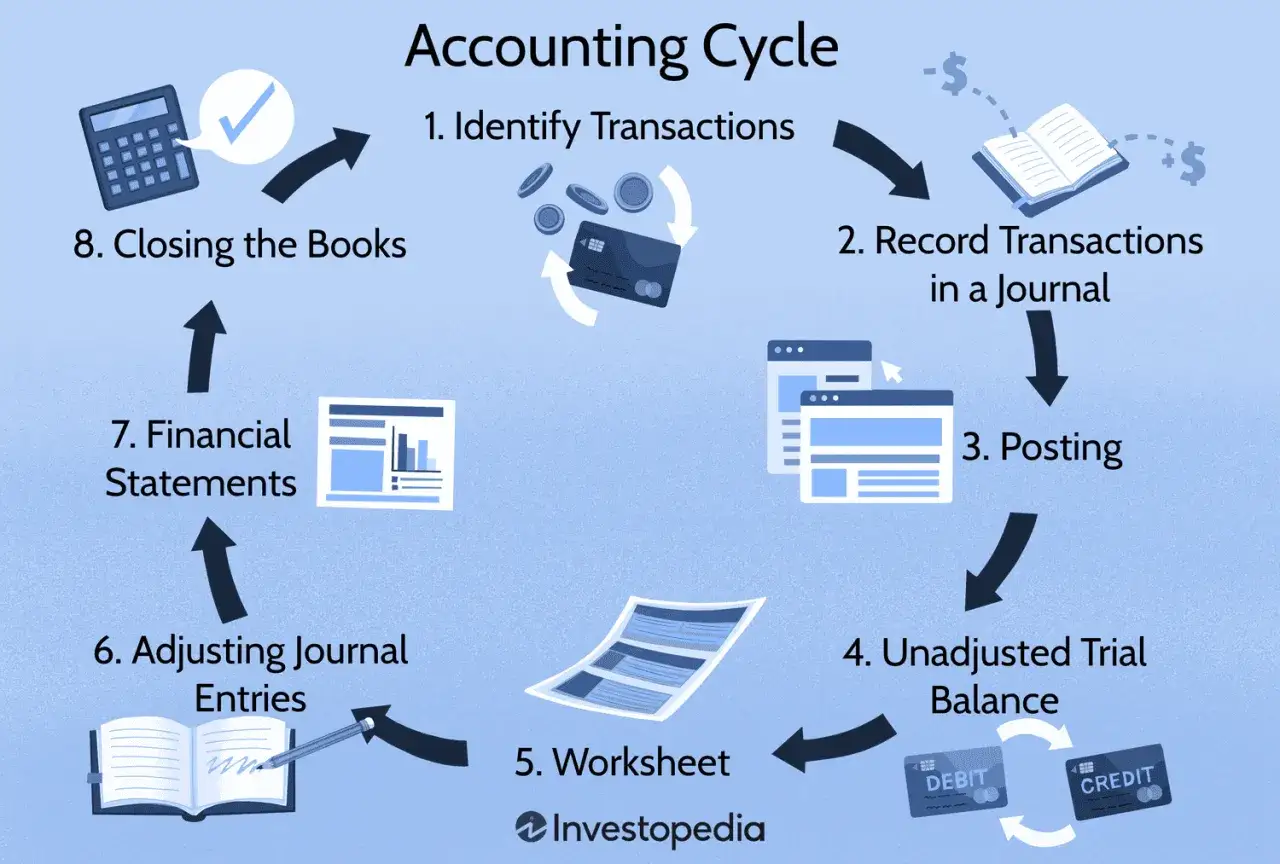

How the invoice cycle works in practice

The cleanest way to think about the cycle is as a sequence of controlled handoffs. I usually map it in six steps:

- Create the source document with the correct customer, vendor, amount, dates, and coding.

- Review and approve the invoice or bill against the contract, purchase order, or service evidence.

- Send or receive the invoice so the other side can process it through their system.

- Apply the payment to the right open item, which is the cash application step on the receivables side.

- Post the entry to the general ledger so the accounting records reflect the transaction.

- Reconcile the balance against the bank statement or subledger and clear exceptions.

That workflow sounds linear, but reality is messier. Partial payments, short pays, credit memos, duplicate bills, and disputed charges all interrupt the clean version. A credit memo is simply a negative adjustment that reduces what is owed, while a short pay means the payer settled only part of the invoice. If those exceptions are not tracked deliberately, the balance may look open even after cash has moved, or closed even though money is still missing.

I also pay attention to timing. Sending an invoice late, waiting too long for approval, or applying a payment days after receipt can distort aging reports and make the month-end close harder than it should be. Once you see the sequence clearly, the next question is why receivables and payables need different controls rather than one shared rulebook.

Why receivables and payables need different controls

Receivables and payables are mirror images only at the most superficial level. In practice, they serve different business goals, expose different risks, and need different metrics.

| Area | Main objective | Typical risk | Useful metric |

|---|---|---|---|

| Accounts receivable | Get paid on time and reduce overdue balances | Customer disputes, slow collections, misapplied cash | Days sales outstanding, aging buckets, dispute rate |

| Accounts payable | Pay the right amount on the right date | Duplicate invoices, unauthorized spend, missed discounts | Approval cycle time, exception rate, on-time payment rate |

On the receivables side, the pressure is usually on speed and accuracy. You want the customer to understand the charge, accept it quickly, and pay without friction. On the payables side, the pressure is on control and timing. You want to verify the bill, avoid fraud, and pay before the due date without handing cash away early unless there is a real reason to do so.

The controls also differ. Receivables teams care about invoice clarity, follow-up cadence, and cash application. Payables teams care about approval limits, vendor master data, and matching rules. If a company treats both sides as the same process, it usually ends up with weak collections, sloppy approvals, or both. The next layer is cash timing, because even a correct invoice can create stress if the payment terms are poorly chosen.

Payment terms and methods that change cash flow

Payment terms are not just administrative language. They shape working capital, customer behavior, and the pace of your close. Net 30 means payment is due 30 days after the invoice date. Net 15 and net 60 follow the same idea. Due on receipt is faster but less flexible, and early-payment discounts can be useful when the tradeoff is worth the margin you give up.

For U.S. businesses, the payment method matters just as much. ACH is usually the cheapest and most predictable option for recurring domestic payments. Cards are faster and easier for some customers, but processing fees can commonly run around 2% to 4%, depending on the provider and card type. Domestic wires are useful for urgency or high-value transfers, but banks often charge meaningful fees on both sides. Checks still exist, especially in older AP processes, but they slow everything down and create more reconciliation work.

| Method | Best for | Main advantage | Main drawback |

|---|---|---|---|

| ACH | Domestic business payments and recurring billing | Low cost and easy reconciliation | Can still take a few business days to settle |

| Card | Small balances, speed, convenience | Fast approval and simple checkout | Higher fees and possible chargebacks |

| Wire | Urgent or large transfers | Quick settlement and strong certainty | Higher bank fees and less flexibility |

| Check | Legacy workflows and some vendor relationships | Familiar to many vendors | Slow, manual, and easy to lose track of |

Late payments are not a small issue either. Xero US has reported improvement in late-payment behavior through 2025, but even a few extra days can put pressure on a small business that depends on steady inflows. I take that as a reminder that the real issue is not whether a payment eventually arrives, but whether the process helps cash arrive when it should. Once cash timing is visible, controls become the difference between a clean close and a messy one.

Controls that keep the books defensible

Good controls do two things at once: they prevent bad entries and make the correct ones easier to prove. That matters for management, lenders, auditors, and anyone else who needs confidence in the numbers. In my view, the best control is the one that stops a problem before it lands in the general ledger.

- Segregation of duties keeps one person from creating, approving, and paying the same item without review.

- 2-way or 3-way matching compares the invoice with the purchase order, and sometimes with receiving evidence, before payment is released.

- Vendor master controls reduce fraud and payment redirection by limiting who can change banking details.

- Approval thresholds make sure larger or unusual charges get a second look.

- Duplicate detection catches the same invoice number, amount, or vendor being entered twice.

- Regular reconciliation clears open items and keeps aging reports meaningful.

If your business uses contractors or service providers, I would also keep tax forms and contract references close to the invoice record. In the U.S., that is often the difference between a smooth year-end and a scramble for missing documentation. Controls are not there to slow the business down; they are there to make sure speed does not create liability. From there, the most useful question is what usually goes wrong when teams ignore these guardrails.

Common mistakes that slow cash or distort the books

Most billing problems are not dramatic. They are small, repeatable errors that pile up until cash flow or reporting starts to wobble. The pattern is usually visible long before the pain becomes obvious.

- Sending invoices late pushes collection dates out and makes revenue look slower than the work really was.

- Using vague descriptions gives customers or vendors a reason to dispute the charge.

- Posting to the wrong account creates clean-looking books with the wrong story underneath.

- Ignoring credit memos leaves balances overstated and confuses follow-up.

- Applying payments manually without a rule increases the chance of misapplied cash.

- Letting approvals drift turns a policy into an exception culture.

- Skipping aging reviews allows old balances to sit until they are harder to collect or explain.

The practical fix is boring but effective: standardize the fields, enforce the approval route, and review exceptions before month-end. I have seen teams spend far more time untangling a few avoidable mistakes than they would have spent preventing them. That is why process design should match the volume you actually handle, not the system you hope to have someday.

What a practical process looks like for a small team

There is no prize for using enterprise software before you need it. A small team usually benefits more from consistency than complexity, and that means choosing a process that fits the actual invoice volume.

| Monthly volume | Practical setup | What I would automate first |

|---|---|---|

| Under 50 invoices | Shared inbox, simple approval path, weekly reconciliation | Reminders, invoice templates, bank matching |

| 50 to 300 invoices | Dedicated AP or AR workflow, approval routing, aging review cadence | OCR capture, payment matching, duplicate checks |

| Above 300 invoices | Role-based permissions, centralized document storage, close checklist | Integrated approvals, cash application, exception handling |

For smaller businesses, I usually prefer a rhythm that is easy to remember: issue bills quickly, review open items weekly, reconcile bank activity on a fixed schedule, and close exceptions before they become month-end surprises. For larger teams, the priority shifts to standardization and audit trail. The accounting system should tell you who touched the item, what changed, and why it was approved. Once that structure is in place, the only real question is how to keep it useful as the business grows.

The habits I would keep if I wanted cleaner books next quarter

If I had to reduce the whole topic to a few habits, I would start with consistency. The mechanics matter less than the discipline behind them. When invoices and payments run through the same controls every time, the books become easier to trust, the close gets faster, and cash stops hiding in exceptions.

- Review open items weekly so problems surface while they are still easy to fix.

- Send invoices as soon as the work is complete instead of waiting for a separate administrative batch.

- Use one naming standard for customers, vendors, and memo fields so records are searchable.

- Track the aging report on both sides of the ledger, not just when something looks overdue.

- Document write-off rules so small balances do not linger forever.

- Compare bank activity to the subledger before the month is closed.

If you want the shortest useful rule, it is this: make the next person in the process able to approve, pay, collect, or reconcile without guessing. That is what turns billing from administrative work into reliable accounting.