For a lot of small businesses, accounting is not just a reporting habit; it changes when income becomes taxable, when deductions show up, and how clearly you can read your own cash position. Cash basis accounting ties revenue to money received and expenses to money paid, which makes it simple on paper but not always simple in practice. I am focusing here on where it works, where it creates blind spots, and how it compares with accrual accounting in the U.S. tax context.

What matters most before you choose a method

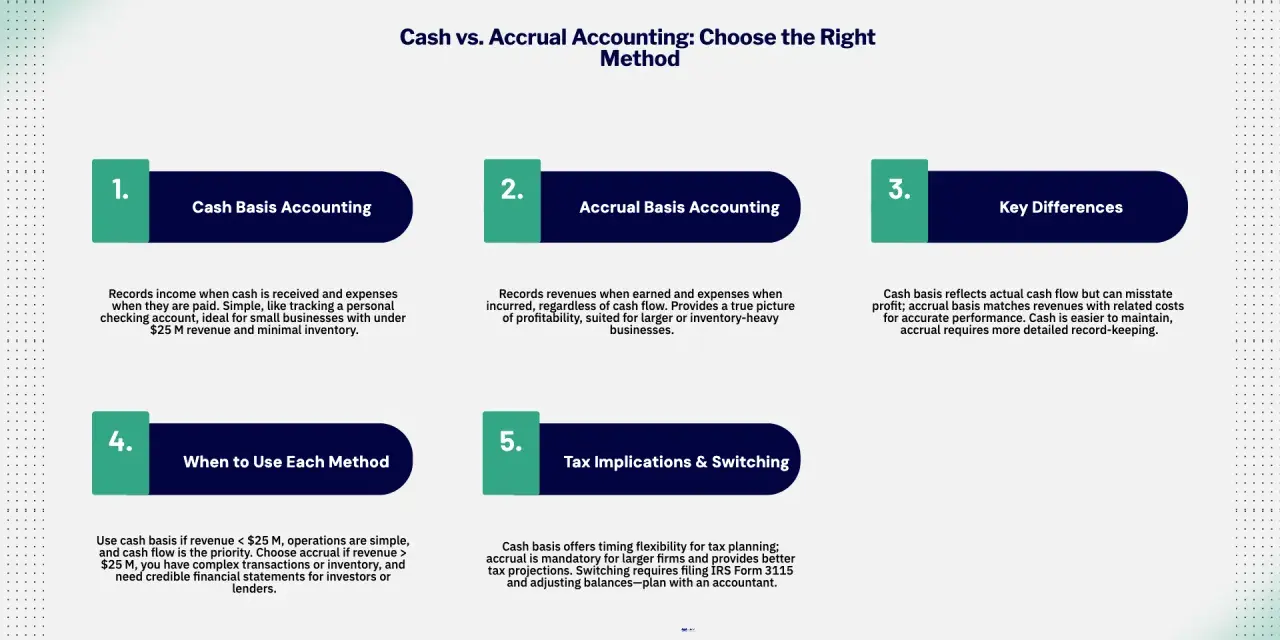

- The cash method recognizes income when you receive it and expenses when you pay them.

- It is usually strongest for service businesses, solo operators, and firms with simple billing.

- Inventory, prepayments, and constructive receipt can change the answer quickly.

- For tax years beginning in 2026, the gross receipts test for certain corporations and partnerships is $32 million over the prior three years.

- Changing methods often means filing Form 3115 and handling a section 481(a) adjustment.

How the cash method changes timing in real life

Under this method, the timing rule is blunt: if the money is in hand, or available without restriction, it counts; if the bill has not been paid, the deduction usually waits. That is why a December invoice paid in January stays out of December income, while a supplier bill paid before year-end can often be deducted in that same year. The IRS uses the same basic framing: income is counted when received, and expenses are deducted when paid.

I like this method when the business owner wants a close link between bank activity and tax results. It reduces the mental overhead of tracking receivables and payables, but it does not eliminate judgment. If a customer payment is already available to you, or a check has been made available without restriction, you do not get to ignore it just because you have not deposited it yet. That distinction matters more than most owners expect, and it leads directly to the bigger question of fit.

Where it fits best and where it starts to break

In practice, I see the cash method work best for businesses with short billing cycles, light inventory, and few moving parts. Consultants, lawyers, marketers, designers, and many other service businesses often value the way it keeps tax reporting close to actual cash flow. If the business is small enough that the owner can explain every major inflow and outflow without a spreadsheet forest, the method usually feels natural.

It starts to break down when the business lives on work-in-progress, deposits, milestones, inventory, or financing covenants. A retailer, manufacturer, contractor, or growing business with outside investors may find the simplicity misleading because the books can look healthier or weaker than the underlying operations really are. In my experience, lenders, boards, and investors usually care less about simplicity and more about whether the numbers show obligations, margins, and timing pressure with enough precision.

As a rule, C corporations, partnerships with a C corporation partner, and tax shelters generally cannot use it, subject to exceptions. That is why the next step is not a slogan about simplicity; it is a side-by-side comparison of how the two methods actually behave.

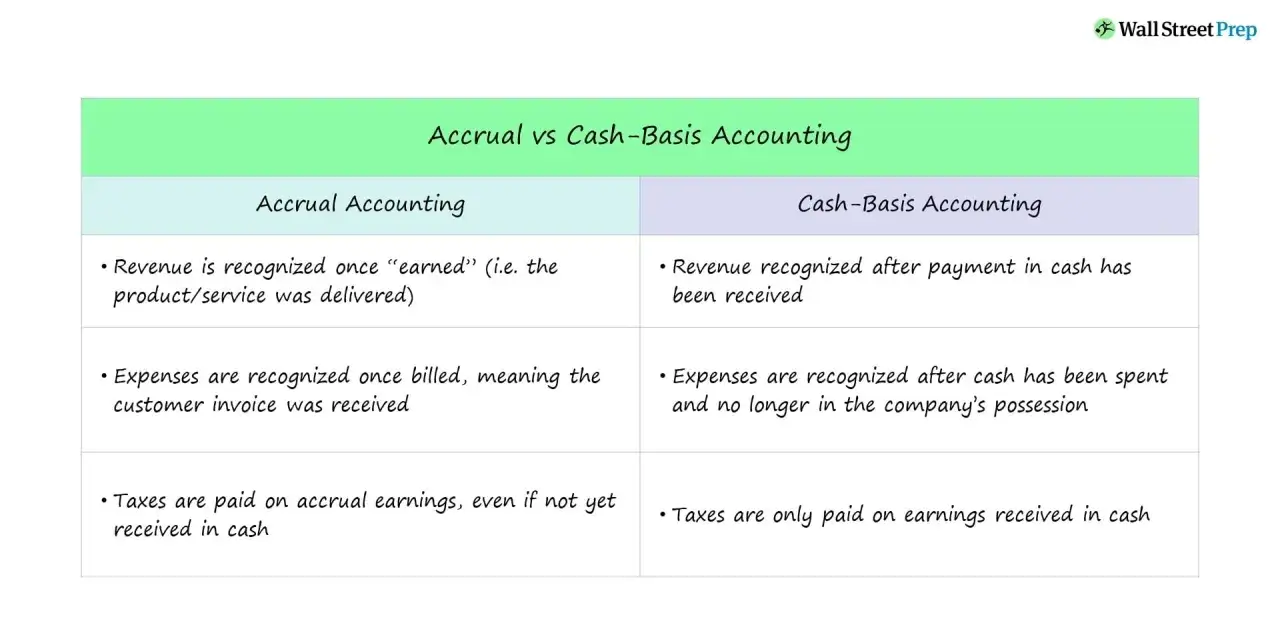

Cash method vs accrual in plain English

| Issue | Cash method | Accrual method | What it means in practice |

|---|---|---|---|

| Revenue timing | When cash is received | When it is earned | Cash can delay tax on unpaid invoices; accrual can show income before the money arrives. |

| Expense timing | When cash is paid | When the liability is incurred | Cash tracks bank outflows closely; accrual tracks obligations more accurately. |

| Inventory | Often limited or subject to special rules | Usually a natural fit | Product businesses need to check whether inventory forces additional accounting steps. |

| Management view | Simple and cash focused | Better for margin and obligation analysis | Cash is good for tax timing; accrual is usually better for operating decisions. |

| Complexity | Lower | Higher | Lower complexity helps small owners, but it can hide timing gaps as a business grows. |

I would not call one method universally better. The right choice depends on the question you need the books to answer: how much cash moved, or how much of the business has actually been earned and owed. Once that is clear, the practical traps become much easier to spot.

The rules that trip businesses up

A lot of mistakes come from assuming the cash method is the same thing as whatever hits the bank account. It is not. Timing rules still apply, and they can move income or deductions into a different year than the owner expected.

Constructive receipt is still receipt

If money is credited to your account or otherwise made available without restriction, it is generally treated as received even if you do not physically touch it. That is why holding a check in a drawer, or simply waiting to deposit money until January, does not erase December income. The rule is meant to stop timing games, and it does a decent job of that because it follows control, not just possession.

Prepaid costs do not all land at once

Expenses paid in advance are another place where owners get tripped up. A one-year insurance policy paid in advance may be deductible in the year it applies, but a longer prepaid benefit often has to be spread across years. The common 12-month rule helps in some cases, but it is not a blank check to front-load every prepaid expense you want.

Read Also: WIP Accounting Explained - Avoid Costly Mistakes

Inventory can pull you into more complexity

If your business produces, buys, or sells merchandise, inventory rules can override the simplicity people expect from the cash method. For tax years beginning in 2026, a corporation or partnership meets the gross receipts test if average annual gross receipts for the preceding three-tax-year period do not exceed $32 million, and that matters because it can preserve cash-method eligibility for many businesses that would otherwise need to think harder about inventory. Even then, the details are not casual: some small businesses can treat inventoriable items as materials and supplies, but they still need a method that clearly reflects income.

In other words, the method is simple until the business model is not. That is why a switch, or even a first-time election, should be handled with a clean process rather than a quick checkbox.

How to switch methods without creating a tax mess

When a business outgrows its current method, the biggest risk is not the form itself; it is duplicating income or omitting expenses during the transition. The IRS generally requires Form 3115 to request a change in an overall accounting method, and the resulting section 481(a) adjustment is what keeps the same item from being counted twice or skipped entirely.

- Identify your current method and the tax return where it is being used.

- List open receivables, unpaid bills, prepaid expenses, and inventory items before the change.

- Work out whether any prior income or deductions would otherwise be duplicated.

- Prepare Form 3115 and follow the filing path that matches the type of change.

- Reconcile the books after the change so tax reporting and management reporting do not drift apart.

If you have more than one business, keep the records separate and avoid mixing method changes in a way that shifts profit from one entity or activity to another. The goal is not just compliance; it is a method that still tells the truth after the year-end dust settles. From there, the last question is strategic: what choice actually serves the business in 2026?

The choice I would make for a U.S. business in 2026

Cash basis accounting is often the right first move for a small service business because it is easy to explain, easy to administer, and usually close to the owner’s lived reality. If revenue arrives in bursts, expenses are straightforward, and inventory is not part of the story, I would lean toward it without apology.

But I would not keep it by default if the business has grown into something more layered. Once inventory, long contracts, financing terms, or outside stakeholders matter, I usually want accrual visibility somewhere in the reporting stack, even if the tax method stays cash. That is the practical balance: use the method that reduces compliance friction, but do not let it hide margin pressure, unpaid obligations, or a business model that is changing faster than the books.

In the end, the best accounting method is the one that matches how the business actually earns, spends, and carries risk, not the one that merely feels easiest in the moment.