An expense is the cost of using resources to earn revenue in a period; a liability is an obligation to give up resources later, and equity is the residual claim left for owners. So, is an expense a liability or equity? No. In U.S. accounting, expenses belong on the income statement, while liabilities and equity live on the balance sheet. The subtle part is that one transaction can create a liability first and only become an expense when the benefit is consumed.

That timing issue is where most confusion starts, especially with unpaid bills, accrued payroll, prepaid insurance, and owner-related payments. I’m going to separate the concepts cleanly, show how the entries work, and point out the mistakes that lead to bad classification.

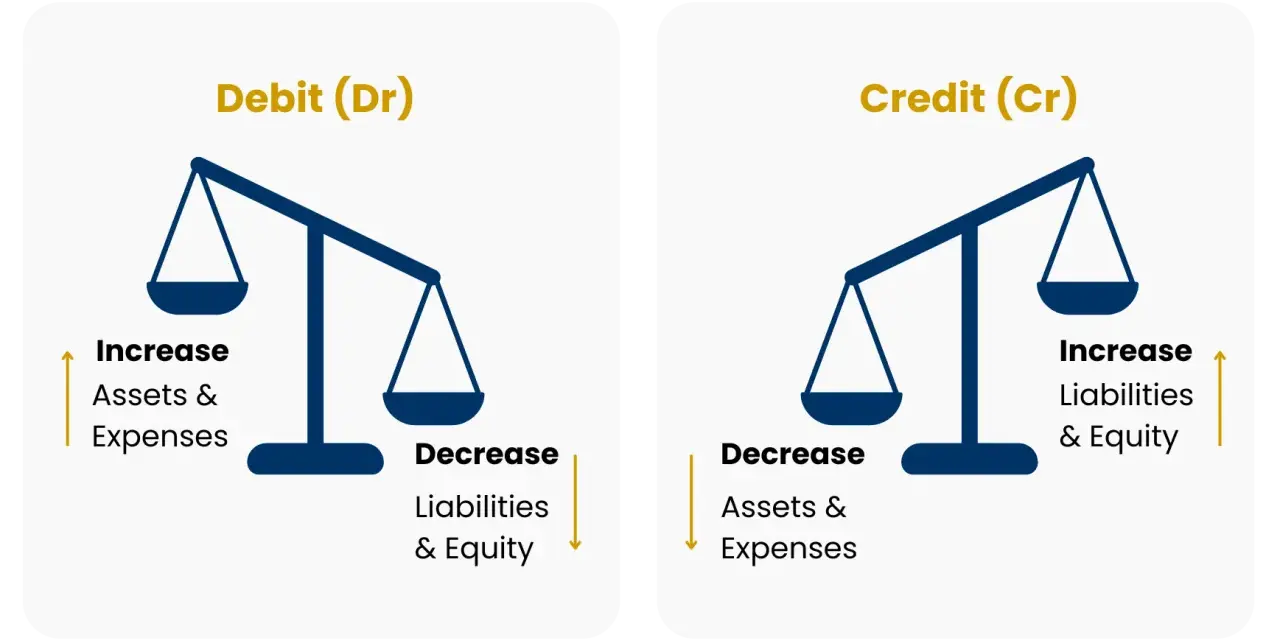

The practical rule is simple: expenses affect performance, while liabilities and equity describe the balance sheet

- Expenses measure costs consumed in the current period and reduce net income.

- Liabilities are present obligations to pay cash or provide services later.

- Equity is the residual interest after liabilities are deducted from assets.

- An unpaid expense often creates a liability, but the expense itself is still an income statement item.

- Expenses reduce equity indirectly through net income and retained earnings.

- Prepayments and owner withdrawals are the most common places where people misclassify the entry.

Why an expense is neither liability nor equity

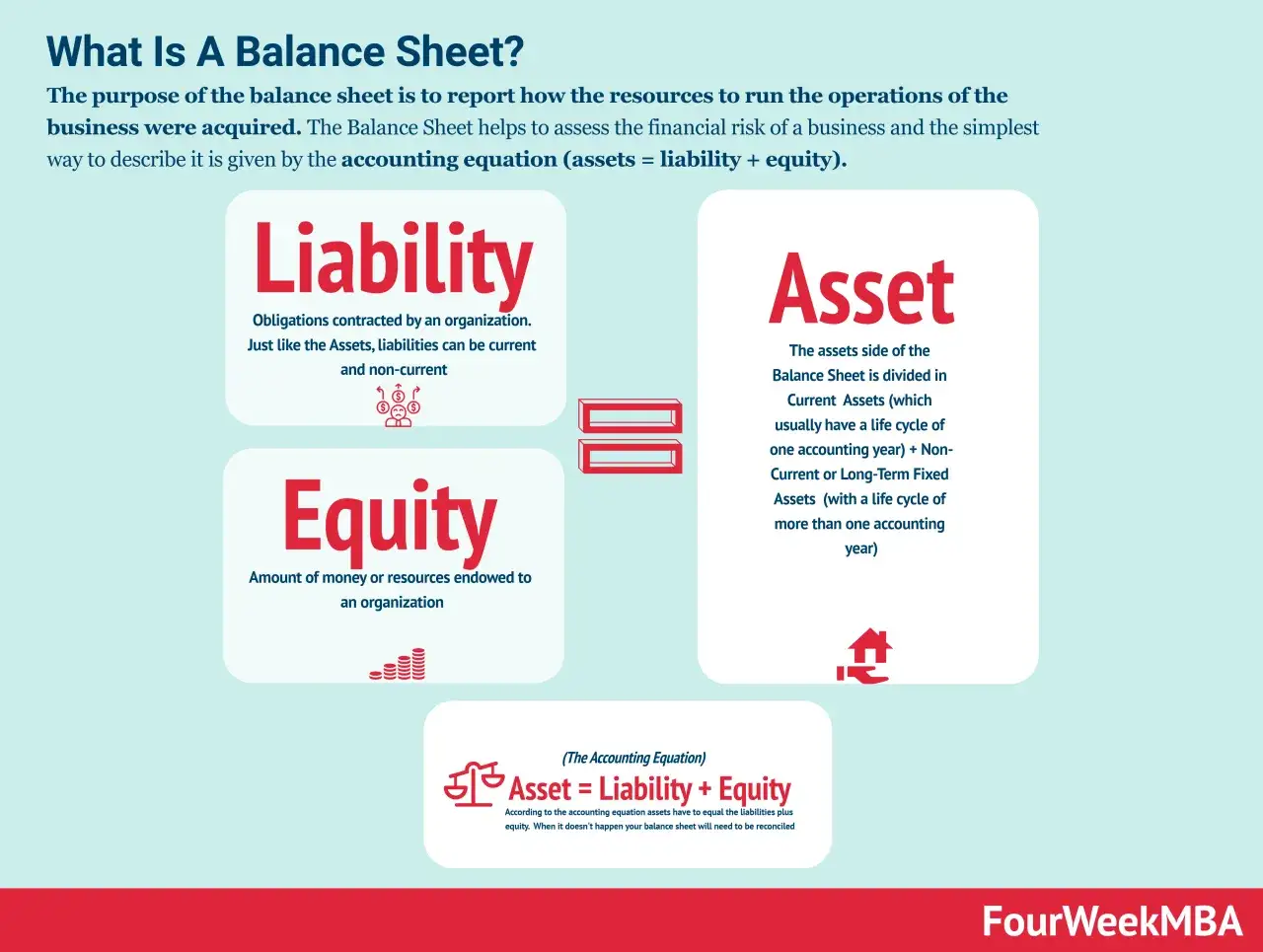

In FASB terms, an expense is an outflow or use of assets, or the incurrence of a liability, from normal operations. A liability is a present obligation to transfer assets or provide services later. Equity is the residual interest after liabilities are deducted from assets. Those are different elements, so an expense is not booked as liability or equity just because it may affect them later.

| Item | Where it appears | What it represents | Simple example |

|---|---|---|---|

| Expense | Income statement | Cost consumed to generate revenue in the period | Rent, salaries, depreciation |

| Liability | Balance sheet | Obligation to pay or perform in the future | Accounts payable, accrued payroll |

| Equity | Balance sheet | Residual claim after debts are settled | Common stock, retained earnings |

So, is an expense a liability or equity? Neither. It is a period result, not a balance-sheet claim. Once you separate the categories this way, the next step is tracing how the same transaction can show up first as a payable and later as an expense.

How expenses move through the financial statements

I like to think of the flow in three stages. First, a business receives a benefit, such as labor, rent, or utilities. Second, that benefit is either paid for immediately, recorded as payable, or prepaid for future use. Third, the used-up portion becomes an expense and lands in net income.

That is why accrual accounting matters so much. Cash timing and expense timing are not the same thing, and they should not be forced to match unless the underlying benefit was actually consumed in that period.

| Scenario | Typical entry | What it means |

|---|---|---|

| Rent paid immediately | Dr Rent Expense / Cr Cash | The cost is consumed now, so there is no liability left behind. |

| Legal services billed later | Dr Legal Expense / Cr Accounts Payable | The service is already consumed, but the cash payment is still due. |

| Insurance paid in advance | Dr Prepaid Insurance / Cr Cash, then Dr Insurance Expense / Cr Prepaid Insurance | The asset is recorded first and expensed over the coverage period. |

| Wages earned but unpaid | Dr Wage Expense / Cr Wages Payable | The labor cost belongs to the current period even though cash goes out later. |

At period-end, expenses flow into net income, and net income closes into retained earnings. That is how expenses lower equity indirectly without ever becoming equity accounts themselves. The real question then becomes when the unpaid amount belongs on the balance sheet as a liability.

When an expense gives rise to a liability

This is the point that trips people up. The expense is recognized because the business has already consumed the benefit. The liability is recognized because the business still owes something for that benefit. One transaction can therefore hit both statements, but for different reasons.

In practice, I look for a present obligation. If the vendor has delivered the service, the employee has earned the wage, or the government has a claim through taxes, the business usually has a liability even before cash leaves the bank account.

| Transaction | Expense account | Liability account | Why the liability exists |

|---|---|---|---|

| Monthly consulting services received on credit | Professional fees expense | Accounts payable | The service is used, but the invoice is unpaid. |

| Payroll earned by employees before payday | Wage or salary expense | Wages payable | The work is done, and the company still owes cash. |

| Utilities consumed before the bill arrives | Utilities expense | Accrued expenses payable | The benefit has been received, even if the bill is delayed. |

| Income taxes based on current-period profit | Income tax expense | Income taxes payable | The tax obligation arises from the current period’s earnings. |

This distinction is why accounts payable is a liability, not an expense. The payable is the debt. The expense is the cost of the goods or services already used. That separation leads naturally into the equity side, because expenses ultimately change owners’ claims even though they are not equity themselves.

How expenses reduce equity without becoming equity

Expenses reduce equity indirectly through profit or loss. In a corporation, lower net income means lower retained earnings, and retained earnings is part of equity. In a sole proprietorship or LLC, the same effect shows up through owner’s capital or member equity. The mechanism changes a little, but the logic does not.

I find it useful to remember that equity is the residual claim. If the business spends money on salaries, depreciation, rent, or interest, those costs reduce the period’s profit and therefore reduce the amount left for owners after liabilities are covered.

- Salaries expense reduces profit because labor was consumed to run the business.

- Depreciation expense reduces profit even though no cash may leave that month.

- Cost of goods sold reduces profit because inventory has been used to generate revenue.

- Owner distributions reduce equity directly, but they are not expenses.

That last point matters more than it seems. A payment to an owner may feel like a business cost, but if it is a draw, dividend, or distribution, it belongs in equity, not in operating expenses. That is where a lot of bookkeeping noise starts, and it leads straight into the most common mistakes.

The misclassifications I see most often

The errors I run into most often are not complicated. They are timing mistakes, category mistakes, or a mix of both. Once you see them, they are easy to fix.

- Recording an unpaid bill as only an expense and forgetting the payable. That understates liabilities and distorts working capital.

- Expensing a prepaid item too early, such as insurance or software subscriptions that cover future periods. That overstates current-period costs.

- Classifying loan principal as expense. Principal repayment reduces a liability; only interest is an expense.

- Booking owner draws as operating expense. That is an equity transaction, not a business cost.

- Expensing capital purchases immediately when the item will provide benefit for more than one period. Many of those should be recorded as assets and depreciated or amortized over time.

These mistakes matter because they do more than change net income. They also change the balance sheet, the ratios lenders watch, and the story the financial statements tell about the business. A quick checklist is usually enough to keep the entry clean.

A quick posting checklist that keeps the entry clean

When I classify a transaction, I walk through four questions in this order:

- Was a benefit consumed in the current period? If yes, expense is likely part of the entry.

- Is there a present obligation to pay later? If yes, a liability belongs in the entry too.

- Does the payment create future benefit? If yes, start with an asset or prepaid account instead of an expense.

- Is this an owner transaction rather than an operating cost? If yes, use equity, not expense.

That checklist is the cleanest way I know to answer the accounting question behind the classification. An expense is not liability or equity, but it can create a liability when unpaid and reduce equity through net income after it is recognized. If you keep the balance sheet and income statement roles separate, the bookkeeping gets simpler and the financial statements become much easier to trust.