The decision to pass credit card processing fees to customers changes more than margin; it changes checkout behavior, customer perception, and sometimes your legal exposure. In the U.S., the right answer depends on card-network rules, state law, and whether a surcharge is actually the cleanest way to recover your costs. I am going to break down the practical version of the issue: what is allowed, how much you can charge, how to roll it out, and when a different pricing model is smarter.

Here is the practical takeaway before you change pricing

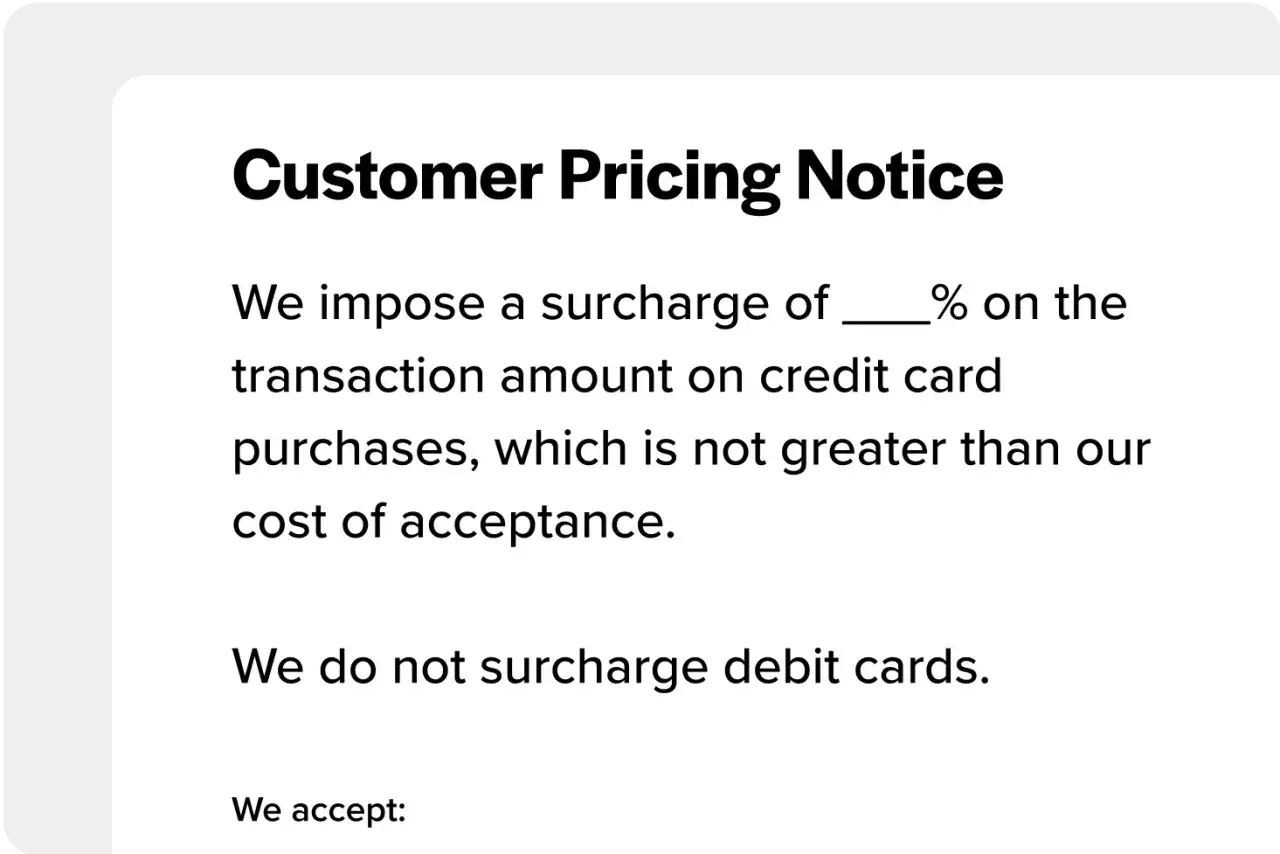

- Credit cards only. Debit and prepaid cards generally cannot be surcharged.

- Use the lower ceiling. Your fee cannot exceed your actual cost of acceptance or the network cap.

- Disclose everywhere. Signage, checkout screens, and receipts all need to match.

- Check state law first. Network permission does not override a state ban or extra notice rule.

- Compare alternatives. A cash discount or a modest price increase can be cleaner than a surcharge.

What it really means to shift card fees to the customer

When businesses try to recover card-processing costs, they usually choose between a surcharge, a cash discount, a broader price increase, or simply absorbing the fee. I treat those as pricing models, not payment settings, because the customer experiences them very differently.

| Approach | What the customer sees | Best fit | Main trade-off |

|---|---|---|---|

| Surcharge | An added fee when paying by credit card | Direct cost recovery when margins are tight | More disclosure work and more checkout friction |

| Cash discount | A lower price for cash or another low-cost method | Businesses that want to reward cheaper payment methods | Easy to mislabel and accidentally turn into a surcharge |

| Price increase | A single posted price for everyone | Simplicity and brand consistency | All customers absorb the cost, even those not paying by card |

| Absorb the fee | No separate fee at checkout | Customer experience matters more than cost recovery | Lower margin on every card sale |

The distinction matters because networks look at substance, not labels. If the final card price is created by adding a fee at checkout, it is a surcharge even if the menu or POS system calls it something friendlier. That is where a lot of businesses get into trouble: the policy sounds simple, but the implementation changes the legal classification.

Once you decide which model fits your pricing philosophy, the next question is whether your state and card-network rules actually allow it.

Where the rules draw the line in the United States

In the U.S., the legal frame is narrower than many owners expect. A surcharge is generally limited to credit cards only; debit and prepaid cards are not supposed to be treated the same way. If you operate in more than one state, you also have to remember that local law can be stricter than network policy.

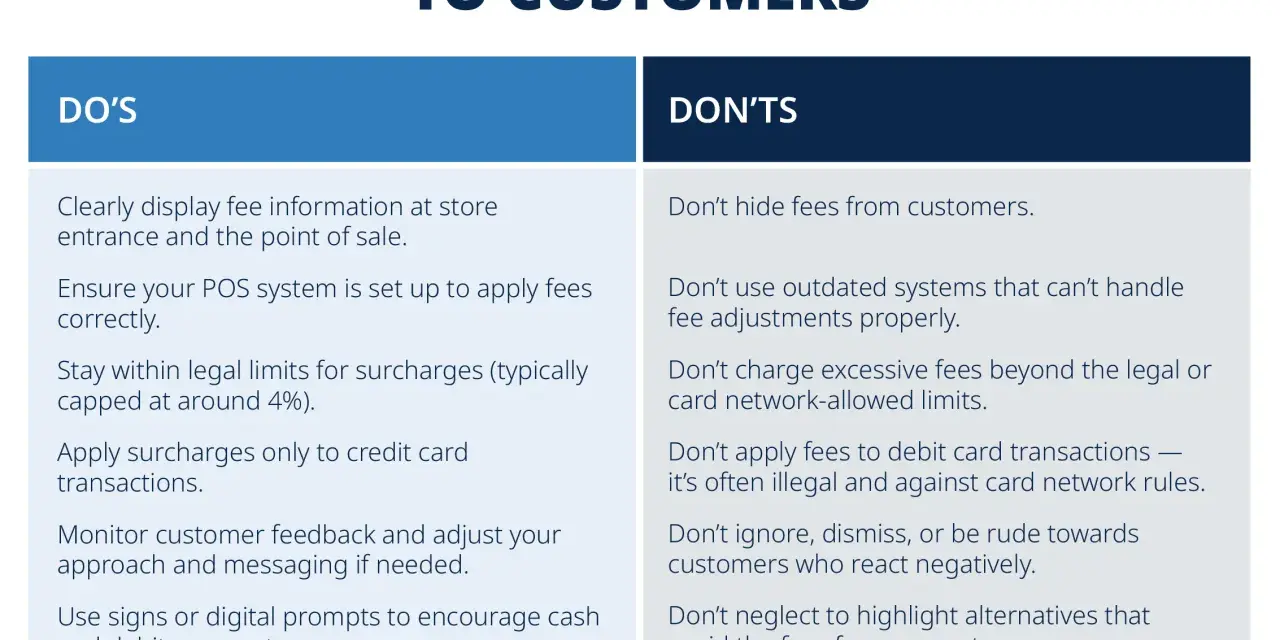

- Notify your acquirer before launch. The standard notice period is 30 days.

- Disclose the fee clearly. The customer should see it at entry, at checkout, and on the receipt.

- Limit the fee to credit cards. Debit and prepaid cards should not be surcharged.

- Respect state restrictions. A state ban or special notice rule overrides a generic national rollout.

- Keep the policy consistent. If you sell in multiple locations, the rule has to work store by store, not just at headquarters.

I would not launch a surcharge program nationally without a state-by-state review and a quick pass from your payments partner or counsel. The payment network may allow the concept, but that is only one layer of the problem. The real operational question is whether you can comply cleanly in every location where the fee will appear.

That legal frame is also what determines the real price ceiling, which is where many merchants miscalculate.

How the fee cap usually works

The basic rule is straightforward: the surcharge should not become a profit center. It is meant to recover the cost of card acceptance, not inflate margin. In practice, that means you need to know your effective merchant discount rate, not just guess from a processor invoice.

Merchant discount rate is the all-in percentage you pay to accept a card, usually including interchange, assessments, and processor markup. If your actual acceptance cost is 2.4%, you cannot charge more than that simply because a network allows a higher ceiling.

| Your effective cost of acceptance | Maximum practical surcharge on a $100 sale | What that tells you |

|---|---|---|

| 1.9% | $1.90 | You recover the full cost, but nothing more. |

| 2.8% | $2.80 | The surcharge still stays below the common network ceiling. |

| 3.4% | $3.00 on a stricter network cap | The network limit starts to matter, even if your actual cost is higher. |

For most merchants that accept multiple major networks, I would plan around the strictest commonly applicable rule rather than the most generous one. That keeps the policy simpler at the register and reduces the chance that your staff accidentally applies different logic to different cards. The safer habit is to calculate the surcharge from a trailing 60- to 90-day effective rate, then test that number against the network cap before you roll it out.

Even a legally clean fee can create operational headaches if the rollout is sloppy, so the execution matters just as much as the math.

How to roll it out without creating friction

The operational side is where good ideas fail. I usually tell businesses to treat a surcharge program like a policy rollout, not a payment tweak. If the customer sees the fee too late, or staff cannot explain it clearly, you will create more dissatisfaction than savings.

- Audit your last few months of processing statements. Use a real effective rate, not a rough average.

- Decide whether surcharge, cash discount, or price increase fits your brand. The cheapest option on paper is not always the best one in practice.

- Configure only credit transactions. Test the POS or checkout flow so debit and prepaid cards do not pick up the fee.

- Put disclosures in three places. The point of entry, the point of sale, and the receipt all matter.

- Train staff on a one-sentence explanation. If employees sound uncertain, customers will assume the fee is arbitrary.

- Test online checkout separately. The fee should appear before the final payment step, not as a surprise after the customer is committed.

I also recommend checking refund and support workflows before launch. A surcharge program that is technically compliant but operationally messy still becomes a customer service problem. If a cashier, support rep, or e-commerce script gives a different explanation than the signage, the business ends up looking careless rather than cost-conscious.

That is why the choice also depends on your business model, which is where the alternatives deserve a direct comparison.

When it makes sense and when it backfires

In practice, I often prefer a simple price increase when the fee is small enough to disappear into normal pricing. It is boring, but boring is often better. Customers usually react less to a slightly higher posted price than to a visible add-on at the end of checkout.

| Strategy | When it fits | Why it works | Where it struggles |

|---|---|---|---|

| Surcharge | Thin margins and strong need for direct cost recovery | Targets the cost to the payment method that creates it | Can create friction and requires more compliance discipline |

| Cash discount | You want to encourage lower-cost payment methods | Feels more consumer-friendly when structured cleanly | Can become confusing if the pricing ladder is not obvious |

| Price increase | You want one clean price across channels | Simpler to explain and usually easier to manage | All customers absorb the card cost, including cash buyers |

| Absorb the fee | Customer experience is the priority and margins can handle it | Fastest, least visible checkout | Lowest protection for profit |

The strategic point is this: surcharge is not automatically the best way to recover cost. If your average ticket is low, the fee can feel disproportionate. If your brand competes on trust, convenience, or premium service, the visible fee may cost more in lost goodwill than it saves in processing expense. For some businesses, the least glamorous answer is the best one: fold the cost into pricing and move on.

After that comparison, the remaining risk is usually not strategy but execution mistakes.

The mistakes I see most often

- Charging debit or prepaid cards. That is the fastest way to step outside the rule set.

- Using the fee as a profit lever. If the charge is bigger than your actual cost or the network ceiling, the program stops being a cost-recovery tool.

- Hiding the fee until the last screen. Surprise is what turns a pricing policy into a complaint.

- Mixing different rules across channels without a clear system. In-store, online, and phone orders can each need slightly different handling.

- Assuming processor settings equal compliance. A POS toggle does not replace legal review or disclosure discipline.

- Ignoring state-specific limits. A policy that works in one state can be illegal a few miles away.

If you cannot explain the fee in one sentence, your customers will usually assume it is a markup. That is why I prefer businesses to keep the language plain, the receipt line item obvious, and the policy narrow. Complexity rarely helps here; it usually creates the exact suspicion the business is trying to avoid.

With those errors out of the way, the decision usually becomes much simpler.

The decision rule I use in 2026

If your goal is simply to recover card costs, I would use a surcharge only when three things are true: your margins are genuinely tight, your checkout system can disclose the fee cleanly, and your state-by-state legal review says the program is allowed where you operate. If any of those pieces is missing, I lean toward a price adjustment or a structured cash-discount model instead.

That is the rule I keep coming back to. Passing the cost through is a pricing decision, not a shortcut. If the economics are meaningful and the rollout is disciplined, it can make sense. If the savings are modest or the compliance burden is messy, the cleaner answer is usually to build the cost into your price and keep checkout friction low.