Startup compensation is rarely just a salary conversation; in early-stage companies it is a trade between guaranteed cash, ownership upside, and the legal terms that determine when that upside becomes real. In the U.S., the structure matters as much as the headline number because vesting, taxes, dilution, and benefit design can change the true value of an offer. I read these packages by asking one simple question: what am I paid today, and what risk am I taking for tomorrow?

This guide breaks down the moving parts, shows how pay changes as a company matures, and gives you a practical way to judge whether an offer is fair before you sign.

What matters most in early-stage pay

- Most startup offers blend salary with equity, but the balance shifts as cash becomes tighter or the company gets more mature.

- Recent data show early-stage firms often keep base pay around the 40th to 50th percentile and lean harder on equity, often in the 70th to 90th percentile range.

- Equity only has value if you understand the grant type, vesting schedule, strike price, and dilution that may come later.

- In the U.S., stock options, restricted stock, and RSUs do not behave the same way at tax time.

- The smartest offer review looks at the whole package, not just salary.

What early-stage pay is actually made of

I usually split an offer into six pieces. Salary is the cash you can count on. Equity is the upside you may never see, but should still understand clearly. The rest of the package is where many candidates underestimate value or miss risk.

| Component | What I check | Why it matters |

|---|---|---|

| Base salary | Is it W-2 cash, paid on a regular schedule, and enough to cover my life without assuming a future exit? | This is the only guaranteed part of the package. |

| Equity grant | Is it stock options, restricted stock, or RSUs, and how many shares or what percentage does it represent? | Equity is where the upside lives, but the instrument changes the real value. |

| Bonus or commission | Is the target realistic, and what triggers payment? | Variable pay can look meaningful on paper and still be hard to earn. |

| Benefits | Health coverage, PTO, parental leave, remote stipend, and whether there is a 401(k) match. | Benefits often decide whether a lower salary is still workable. |

| Sign-on or relocation | Is there a clawback if I leave early? | One-time cash helps with transition costs, but repayment clauses can be brutal. |

| Severance and protection | What happens if the company cuts the role, gets acquired, or changes direction? | At a startup, job security is part of compensation even when nobody labels it that way. |

One mistake I see constantly is treating salary as the whole offer. At an early-stage company, the better question is whether the cash, equity, and protections together match the amount of risk the role asks you to take. Once that is clear, the next question is how those terms shift as the company moves from seed to scale.

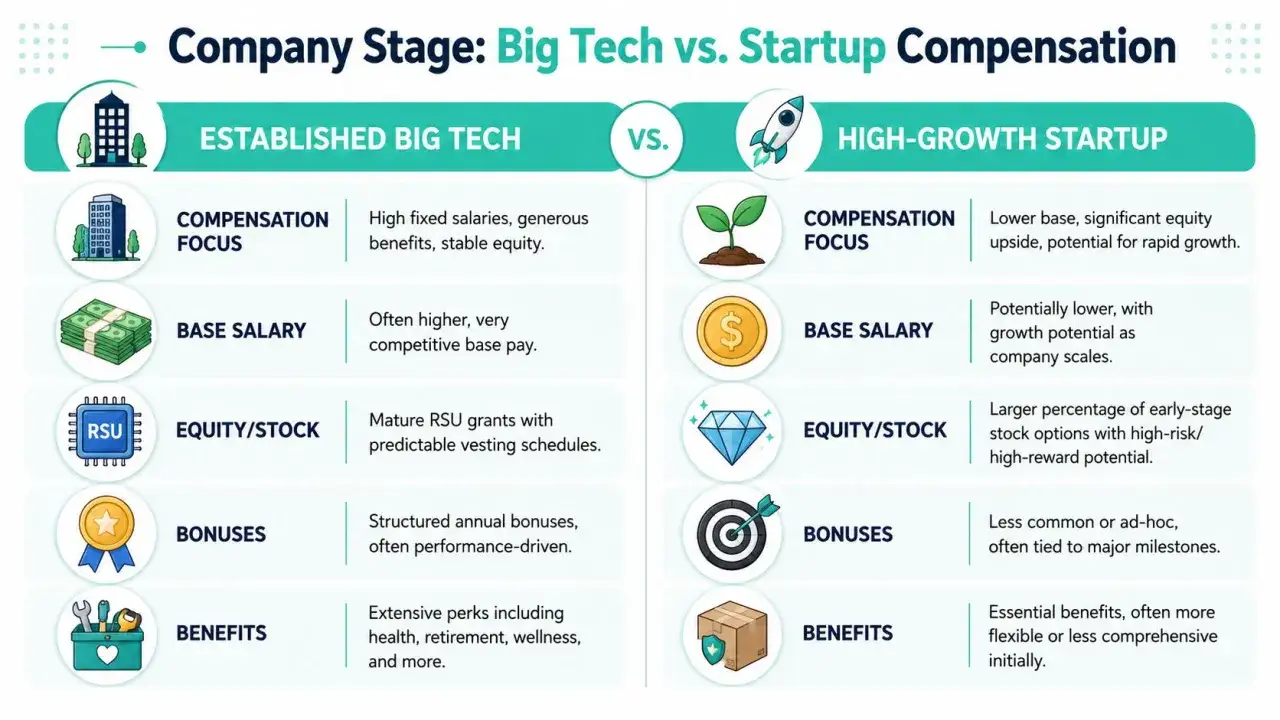

How the package changes by stage

Recent startup compensation data show early-stage founders often keep base pay around the 40th to 50th percentile and push more value into equity, often in the 70th to 90th percentile range. That approach is not about stinginess, it is about runway. Cash is usually the scarcest resource in the first years, so the package has to do more work than a normal market-rate salary.

| Stage | What the package often looks like | What to watch |

|---|---|---|

| Pre-seed | Lower cash, large uncertainty, and the highest dependence on equity upside. | Runway, credibility of the plan, and whether the company can survive long enough for the grant to matter. |

| Seed | Slightly more salary structure, more formal equity grants, and still meaningful ownership. | Whether the company has a real compensation philosophy or is improvising offer by offer. |

| Series A | Closer to market on salary, smaller equity grants, and better-defined roles. | Whether the company is paying like a mature business while still offering startup-level risk. |

| Series B and beyond | More cash, more benefits, and equity that is usually narrower but more predictable. | Whether the upside is still big enough to justify leaving a safer employer. |

For the first handful of mission-critical hires, ownership requests around 1% or more are not unusual, especially when the company needs someone who will shape the product, go-to-market motion, or engineering foundation. I also like to check whether the company has reserved enough equity for the future. Many startups set aside roughly 13% to 20% of fully diluted equity for the employee option pool, because early hires and later refresh grants both have to come from somewhere.

That stage logic matters because the paper value of the grant depends on the equity mechanics behind it, and that is where a lot of people get their first real surprise.

How equity really works in a startup offer

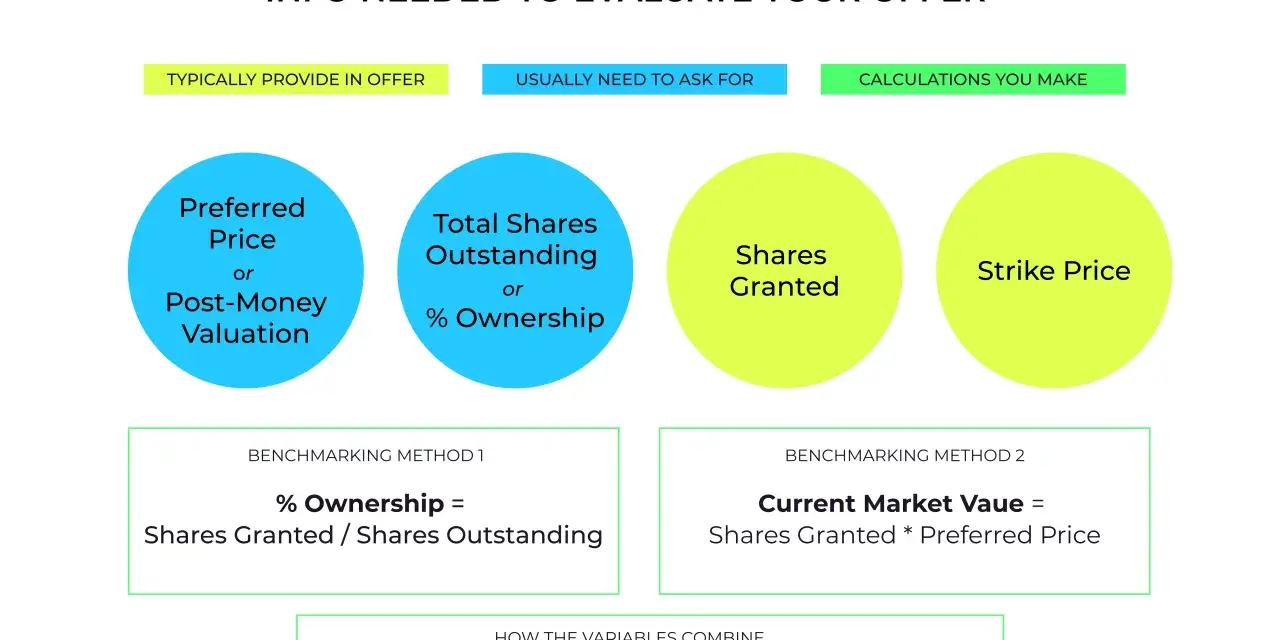

Equity is where early-stage pay becomes part finance, part law. The instrument, vesting schedule, and strike price all affect what you actually own and when you can benefit from it. I never review an equity grant as a simple percentage without asking how the company is calculating that percentage.

| Equity type | Where you usually see it | Tax timing | Main issue to understand |

|---|---|---|---|

| Incentive stock options | Common for U.S. employees at private startups | Usually no ordinary income at grant or exercise, though AMT can apply | Exercise cost, tax at sale, and whether the company lets you exercise long enough after you leave |

| Nonqualified stock options | Employees, advisors, and sometimes mixed roles | Ordinary income is often triggered on exercise | The spread between strike price and fair market value can create a real cash tax bill |

| Restricted stock | Very early hires and founders | Can be taxed when transferred unless an 83(b) election is filed | The 30-day filing deadline is easy to miss and hard to fix later |

| RSUs | More common as companies mature | Typically taxed when they vest or settle | Withholding and settlement rules matter, especially if you expect to leave before liquidity |

The strike price is the price you pay per share when you exercise an option. In private companies, it is usually tied to fair market value on the grant date through a 409A valuation. That is why a grant can look generous and still end up being useless if the company is slow to grow, the strike price is high, or the exit never arrives.

Fully diluted basis is another term I watch carefully. It means the ownership percentage is calculated after including the shares already issued, the option pool, and other convertible securities that could eventually exist. If someone tells you that you are getting 0.3 percent, I want to know whether that is before or after dilution assumptions, because that difference can be real money.

Vesting also matters more than many candidates expect. A standard vesting schedule is there to keep ownership tied to continued service, and a shorter post-termination exercise window can force you to decide quickly after leaving. I treat dilution and vesting as normal startup mechanics, not red flags by themselves. What matters is whether the company explains them clearly and uses them consistently.

Once the equity instrument is clear, the tax layer becomes the next filter, because that is where an otherwise good offer can become expensive.

Taxes and compliance that can turn a good offer into a bad surprise

The IRS treats salary, options, and restricted stock differently, and those differences affect both timing and cash flow. I do not think candidates need to memorize tax code, but they do need to know when a grant creates ordinary income, when it does not, and what forms the employer has to issue.

- Salary is simple. If you are a W-2 employee, withholding handles most of the mechanics automatically.

- ISOs are usually tax-efficient at the start. They generally do not create ordinary income at grant or exercise, but exercise can trigger alternative minimum tax, and tax consequences show up when you sell.

- NSOs are more immediate. The spread between strike price and fair market value is often treated as ordinary income when you exercise.

- RSUs are taxed later. They are typically taxed when they vest or settle, and the value usually appears on your W-2.

- Restricted stock can be front-loaded for tax purposes. If you receive stock that is still subject to forfeiture, the 83(b) election has to be filed within 30 days of transfer.

- Worker status matters. If a company pushes contractor paperwork instead of employee status, that is not a small administrative detail, it changes taxes, benefits, and legal protections.

The tax point I see people miss most is timing. A person can have a paper gain and still owe real tax before seeing any liquidity. That is especially true with RSUs and exercised options. If you are considering an equity-heavy offer, I would ask how the company expects withholding to work, whether you will need cash to exercise, and whether the tax consequences line up with your personal liquidity.

With the legal and tax pieces in view, negotiation becomes less about asking for everything and more about improving the few terms that move total value the most.

How to negotiate for the right mix of cash and upside

I would not negotiate a startup offer as "salary versus equity." I would negotiate it as a total risk package. That means I want to know which parts are fixed, which parts are contingent, and which parts only pay off if the company performs well over several years.

- Ask where base salary sits against market. I want to know the target percentile for my level, location policy, and function.

- Ask for equity in clear terms. I want the number of shares and the percentage on a fully diluted basis, not just a vague promise of upside.

- Ask what kind of equity it is. Options, restricted stock, and RSUs do not behave the same way, and the differences matter.

- Ask about vesting and cliffs. If I leave early, I want to know exactly what I keep and what I lose.

- Ask about the exercise window. A short window can force a cash decision before the company has created real value.

- Ask about severance and acceleration. A good offer protects me if the company is acquired or if the role changes faster than expected.

- Ask about refresh grants. If the company plans to dilute employees over time, there should be a credible policy for topping up key people later.

The biggest tradeoff is simple: a $10,000 salary increase is visible immediately, but a 0.1 percent equity difference can matter more if the company exits at scale. I think the right answer depends on your cash needs, your risk tolerance, and how confident you are in the company's path. If you need stability, push for cash. If you can absorb risk and believe in the team, use that leverage to improve ownership terms and protection on the back end.

That comparison leads naturally to the final question I ask myself before saying yes: whether the offer still works if the best-case story never happens.

The checks I would run before accepting the offer

Before I say yes, I want to know whether the offer makes sense in a normal or even disappointing outcome, not only in the best case. If the math only works when everything goes right, I treat that as a warning sign.

- Can I cover my living costs on salary alone for at least 12 to 18 months?

- Do I know the exact equity type, share count, and diluted ownership percentage?

- Are vesting, cliff, exercise window, and acceleration terms written down?

- Is the company transparent about dilution, option pool size, and refresh policy?

- Would I still be comfortable if the equity ended up worthless?

- Am I being hired as a real employee on W-2 terms, not pushed into contractor status to save the company money?

If most of those answers are yes, the offer is probably coherent. If the package only looks attractive when you assume a perfect exit, I would slow down and push for better terms or clearer paperwork. In my view, the best early-stage offers do not hide the risk. They make it visible, price it honestly, and give you enough upside to justify taking it on.