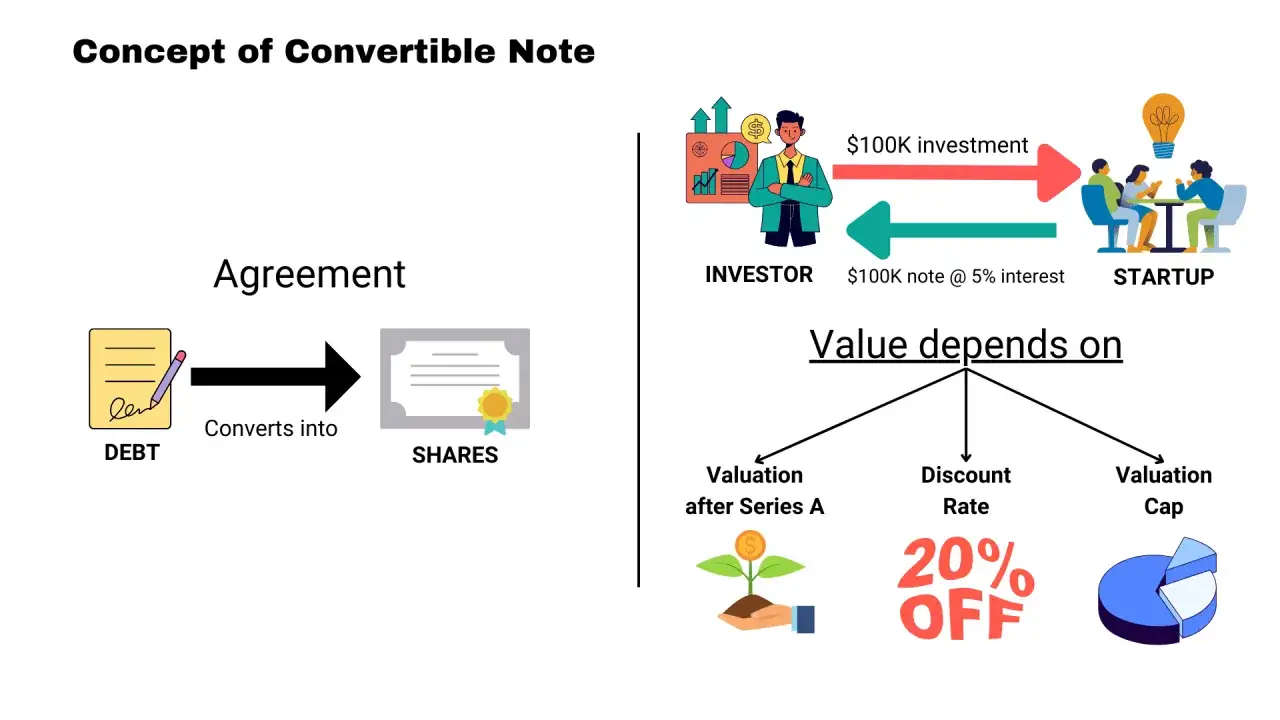

A convertible note is one of the fastest ways a startup can raise money before everyone agrees on a valuation. I usually describe it as short-term debt with an equity conversion feature: the company borrows now, and the investor may later receive shares instead of repayment when a future financing or another agreed trigger occurs. This article breaks down how the instrument works, which terms drive the economics, how it compares with a SAFE and a priced equity round, and where the legal and financial risks actually sit.

Key points to keep in view

- A convertible note starts as debt, not equity, and usually converts only when a future financing or exit trigger occurs.

- Its economics are driven by four terms: interest, maturity, discount, and valuation cap.

- It is often used in U.S. seed-stage financing because early valuation is hard and speed matters.

- It can be cheaper and faster than a priced round, but it also creates repayment and negotiation pressure if conversion does not happen on time.

- Compared with a SAFE, a note adds debt features; compared with priced equity, it usually requires less upfront legal work.

Convertible notes start as debt and may become equity

In the SEC's startup securities guidance, the instrument is treated as a loan that can later become another security. That framing matters because the investor is a creditor on day one, not a shareholder, even though the end goal is often equity. I find that distinction easy to miss when founders focus only on speed and investors focus only on the upside.

In plain English, the company receives cash now, owes the money back if nothing else happens, and may instead issue preferred stock later if the note converts. Once you see that split, the real question becomes when the conversion happens and on what terms.

That takes us to the mechanics, because the trigger matters as much as the label.

How the conversion works in practice

A note usually follows one of three paths:

- It converts automatically in a qualified equity financing, often a priced preferred stock round.

- It reaches maturity before that round closes, which forces a repayment discussion, an extension, or a restructuring.

- It is covered by a sale or change-of-control clause, which may convert the balance, pay it out, or let the investor choose between outcomes.

Many notes also set a minimum financing size before automatic conversion kicks in. In practice, that floor is often around one to two times the outstanding principal, because investors do not want a tiny round to force an early conversion on weak terms. I like that safeguard when the next round is still uncertain, but it can become a problem if the threshold is set too high and the note never converts when the company actually raises money.

That leads straight into the terms that change the economics, because the document is often won or lost on a few lines of paper.

The terms that change the economics

The headline amount is rarely the whole story. The real economics come from the conversion formula, and I usually check these terms first.

| Term | What it does | Why it matters |

|---|---|---|

| Principal | The amount invested | This is the base amount that converts or must be repaid |

| Interest | Accrues on the balance until conversion or repayment | In U.S. startup notes, 5% to 8% is common, and it increases the amount converting |

| Maturity date | The deadline for the note | Typical terms run 12 to 24 months, so the clock matters |

| Discount | Lets the investor convert at a lower price than the next round | Typical discounts are 15% to 25%, rewarding early risk |

| Valuation cap | Limits the valuation used for conversion math | It protects investors if the next round prices the company much higher |

| Sale or default terms | Sets what happens if the company is sold or misses obligations | This can decide whether the investor gets cash, equity, or a negotiated outcome |

The point of the cap is easy to misunderstand. It is not a public valuation declaration, even though people often treat it like one. It is a ceiling in the conversion formula, and when the cap and the discount both apply, the note usually converts on whichever basis gives the investor the better price. That is why two notes with the same principal can produce very different dilution later.

Once you understand those terms, the comparison with other startup instruments becomes much clearer.

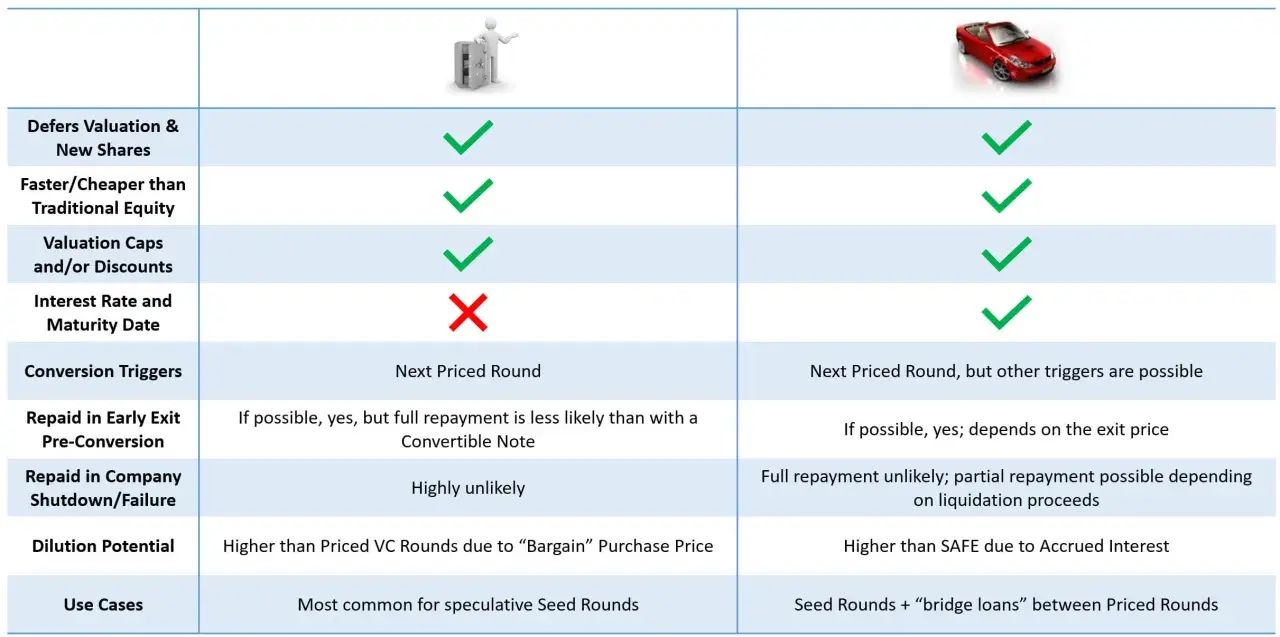

Convertible notes versus SAFEs and priced equity rounds

Founders often compare three paths at the seed stage, and I think that comparison is useful because each one solves a different problem.

| Instrument | What it is | Main advantage | Main tradeoff | Best fit |

|---|---|---|---|---|

| Convertible note | Debt that may convert into equity later | Fast, familiar, and often cheaper than a priced round | Creates maturity pressure and repayment risk if conversion never happens | Early financing when the company expects a future equity round |

| SAFE | A right to future equity, not debt | Simpler, with no maturity date or interest | Less creditor protection and different economic tradeoffs | Very early fundraising when simplicity matters more than debt features |

| Priced equity round | Shares are sold at an agreed valuation now | Immediate clarity on ownership and dilution | Slower, more negotiated, and usually more expensive to document | When the company can support a current valuation and wants cleaner ownership terms |

In the U.S. market, SAFEs are now common at the earliest stage, but convertible notes still show up when parties want debt features, interest, or a maturity date. I reach for a note when the company is too early to price cleanly but still needs capital in weeks, not months. That practical reason is why the instrument has not disappeared, even if the SAFE has taken more of the spotlight.

The next question is why anyone still chooses a structure that can create debt pressure later.

Why founders and investors still use them

There is a reason convertible notes survived the rise of SAFEs: they solve a real timing problem. A startup can take money quickly without locking into a valuation that might look ridiculous six months later. That flexibility matters when product traction is still forming, customer data is thin, and both sides know that a priced round would be more guesswork than finance.

- They are faster to document than a preferred stock round.

- They postpone valuation until the company has more evidence.

- They can be cheaper in legal and negotiation costs than a priced equity financing.

- They give early investors downside protection through debt status before conversion.

- They can bridge the company from one milestone to the next without restarting the whole fundraising process.

That same flexibility is also the weak point. If a startup is unlikely to raise a next round on time, a note can turn into a liability instead of a bridge. That is the point where a shortcut becomes a problem.

The risks people underestimate

I have seen the same mistakes repeat often enough to treat them as patterns rather than surprises. Founders tend to focus on the money coming in and ignore what happens if the next round slips. Investors, meanwhile, sometimes assume the note is safer than it really is because it sounds like debt. Both reactions are incomplete.

For founders

- The maturity date can create repayment or renegotiation pressure if no financing closes.

- A low cap can cause more dilution than expected once the note converts.

- Multiple notes issued at different times can complicate the cap table and the next round.

- A sale clause may force an outcome that is more expensive than the company planned.

Read Also: Inventory Financing - Is It Right For Your Business?

For investors

- If the note is unsecured, recovery can be limited if the company fails.

- A weak discount or high cap may not compensate for early-stage risk.

- Conversion timing can be delayed if the next round does not satisfy the financing threshold.

- Legal and securities compliance still matter, because this is not an informal promise between friends.

I also pay attention to the balance between simplicity and protection. A note that is too founder-friendly can leave investors underprotected, but a note loaded with extra provisions can make the bridge financing feel almost as heavy as a priced round. That tension shows up best in a worked example.

A seed-stage example shows the math clearly

Imagine a startup raises $500,000 on a note with 6% annual interest, a 20% discount, a $5 million valuation cap, and an 18-month maturity. If the next priced round closes at a $10 million pre-money valuation, the note does not convert at the full $10 million figure. The investor gets the better of the discount or the cap math, which means the conversion price is lower than the price paid by the new investors. In that sense, the early money is rewarded for taking more risk.

If the company never closes that round and the interest is simple rather than compounded, the balance would grow to about $545,000 before fees over 18 months. That is not a trivial difference when a young company is managing cash tightly. When I walk through these numbers with founders, I focus less on the headline raise and more on the ownership and repayment pressure that can follow.

That is why the final check is not just whether the note is common in the market, but whether the document matches the company’s likely path forward.

The real decision is whether the bridge matches the business

Before signing a note, I would want five things clear: the exact trigger for conversion, how the cap and discount interact, what happens at maturity if no round closes, whether the note is secured or unsecured, and how a sale or default is treated. If any of those answers are fuzzy, the instrument is not simple enough for the situation.

For a company that truly expects a near-term equity round, a convertible note can be an efficient bridge. For a business that already has a credible valuation or no clear financing path, I usually prefer a structure that makes the economics more explicit from day one. The instrument is useful, but only when it fits the timeline, the cap table, and the company’s real fundraising prospects.