A donation acknowledgement letter does two jobs at once: it thanks the donor and gives them the written record they may need for U.S. tax reporting. For a nonprofit, that means the letter has to be precise enough for compliance and simple enough to scale across cash gifts, events, recurring donors, and noncash contributions. I’m focusing on the parts that actually matter in operations: the tax threshold, what to include, when to send it, and where organizations most often get tripped up.

What matters most before you send one

- For gifts of $250 or more, the donor generally needs a contemporaneous written acknowledgment to support a federal deduction.

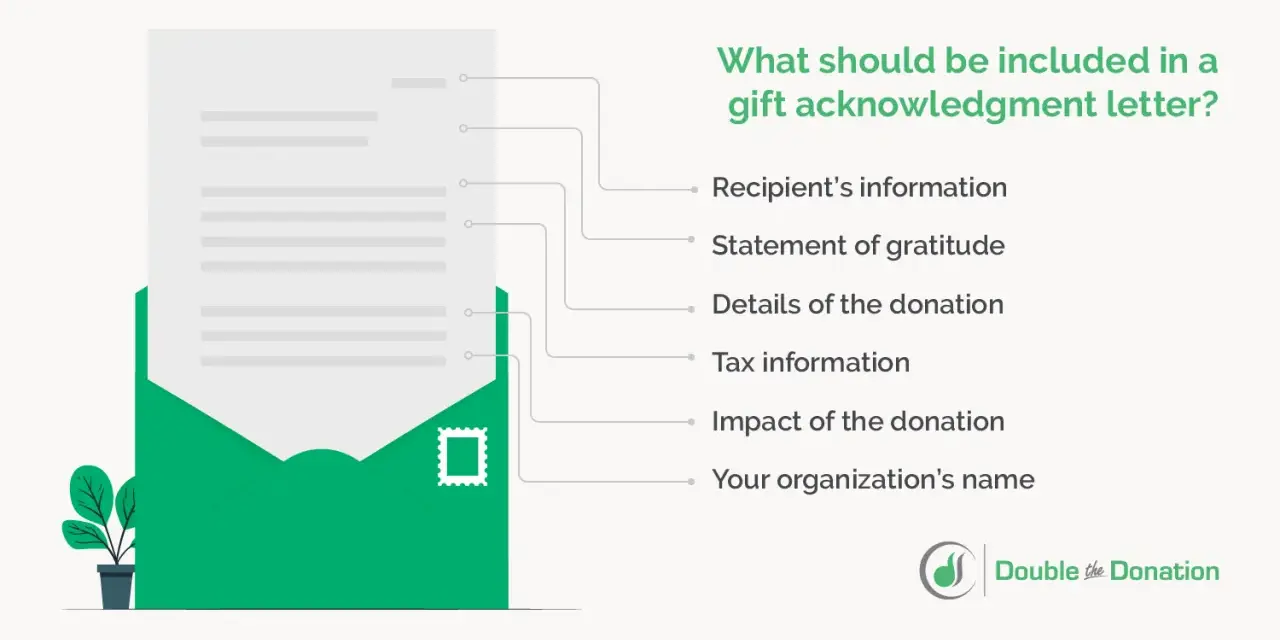

- The letter should identify the organization, state the cash amount or describe noncash property, and disclose any goods or services received in return.

- Quid pro quo gifts over $75 require a separate disclosure statement with a fair-market-value estimate of the benefits provided.

- Email is acceptable, and there is no IRS form for the acknowledgment itself.

- Recurring gifts can be summarized, but each qualifying contribution still has to be identified correctly.

Why this letter matters for donors and your records

In practice, this is not just a polite thank-you note. It is part stewardship, part recordkeeping, and part risk control. A donor may need the document to support a deduction, while your organization needs it to show that gifts were classified correctly, benefits were handled properly, and year-end reporting did not drift into guesswork.

That matters even more in 2026, because some taxpayers who do not itemize can still deduct limited cash gifts to certain qualified organizations, up to $1,000 or $2,000 if filing jointly. I would not build an entire donor communications strategy around that rule, but it is one more reason clean receipts now carry real value.

| Document | Best use | What it must do |

|---|---|---|

| Thank-you note | Stewardship and relationship building | Can be warm and general, but may not be enough for tax substantiation |

| Written acknowledgment | Tax support for qualifying charitable gifts | Must include the required factual statements |

| Quid pro quo disclosure | Gala tickets, dinners, auctions, or membership gifts with benefits | Must explain the deductible portion and the value of benefits received |

I usually treat these as three different jobs, even when they end up in one email. Once that distinction is clear, the content requirements become much easier to manage.

What federal tax rules expect to see in the letter

The content is more specific than many nonprofits realize, but the structure is still straightforward. For a qualifying gift of $250 or more, the acknowledgment should cover the donor’s contribution and any return benefits with enough clarity that the donor can use it for tax records.

| Required element | Why it matters | Common slip |

|---|---|---|

| Organization name | Shows who received the gift | Using a program name instead of the legal entity name |

| Cash contribution amount | Supports the deductible amount for cash gifts | Listing only a running total without the actual gift amount |

| Description of noncash property | Identifies what was donated without assigning value | Adding a value when the acknowledgment should only describe the item |

| Statement that no goods or services were provided, if true | Confirms the gift was not part sale, part donation | Leaving this out on a standard cash gift receipt |

| Description and fair market value of any benefits received | Allows the donor to calculate the deductible portion | Stating the full payment is deductible when event benefits were received |

| Statement for intangible religious benefits, if applicable | Covers a narrow religious exception | Using this language outside its proper context |

FMV, or fair market value, is the amount a willing buyer would reasonably pay for the goods or services received. That is the number that matters in mixed-benefit situations, not the sticker price of the donation or the emotional value of the event.

The IRS does not prescribe a form, so a letter, postcard, or computer-generated receipt can all work if the facts are right. I also prefer to keep donor identification lean, because the acknowledgment should not ask for a Social Security number or tax ID number. Once the content is right, the next issue is timing, and that is where many otherwise solid systems break down.

When to send it and how to handle recurring gifts

The key timing rule is simple: the donor must receive the acknowledgment by the earlier of the date they file the original return for that year or the return due date, including extensions. In day-to-day nonprofit operations, I still treat January 31 of the following year as the practical deadline for year-end gifts, because it gives donors time and gives staff a buffer.

Another rule that often gets missed is aggregation. Separate contributions of less than $250 are not combined just to hit the threshold. A donor who gives $25 every week does not suddenly have one $250+ gift every four weeks for acknowledgment purposes. That is why recurring giving needs a clean system, not a spreadsheet patched together in March.

| Scenario | What I would send | What to watch |

|---|---|---|

| One cash gift of $50 | Optional thank-you note or receipt | Not required for the $250 substantiation rule |

| One cash gift of $250 or more | Written acknowledgment with the required tax language | Make sure the donor receives it on time |

| Monthly gifts of $25 | Regular stewardship communications, plus a year-end summary if useful | Do not aggregate small gifts just to reach $250 |

| Several gifts of $250 or more during the year | One annual summary can work if it lists each qualifying gift and date | Do not lose the individual gift dates |

| Payroll deduction gifts | Acknowledgment or annual summary tied to each qualifying deduction | Each deduction amount is treated separately for the threshold |

When I see delays, the root problem is rarely the letter itself. It is usually weak gift coding, unclear year-end batching, or a team that waits until tax season to reconcile records. Once timing is under control, the real skill is writing the letter so it sounds human without diluting the compliance language.

How to write one that feels human and still holds up in an audit

The strongest letters are short, specific, and calm. I like to think of them as receipts with a human pulse. They should not sound like a legal memo, but they also should not sound like a fundraising blast that forgets the tax implications.

For a plain cash gift, a clean version can be as simple as this:

Standard cash gift

Thank you for your generous contribution of $500 received on March 12, 2026. No goods or services were provided in exchange for this contribution.

If the donor received something in return, the language has to change:

Mixed-benefit event payment

Thank you for your payment of $250 for attendance at our annual gala. The fair market value of the dinner and entertainment provided was $80. The deductible portion of your payment is limited to the amount that exceeds that value.

For a noncash gift, I would keep the acknowledgment descriptive and avoid assigning value:

Noncash contribution

Thank you for your contribution of one office printer received on June 4, 2026. This acknowledgment confirms receipt of the property described above. No value is assigned in this letter.

That last point matters. A nonprofit should describe noncash property, not appraise it in the acknowledgment. If you want to make the letter more donor-friendly, add one sentence telling the donor to keep it with their records, but do not clutter it with extra claims. Clean wording is usually the safest wording. From there, the hardest cases are the ones that involve benefits, events, or property with separate substantiation rules.

Special cases that deserve manual review

Some donations are routine enough to automate, while others need a human check before anything goes out. If the gift involves a benefit, property, or event admission, I would route it for review instead of letting the CRM fire off a generic receipt.

| Special case | What the acknowledgment should do | Why manual review helps |

|---|---|---|

| Gala tickets and dinners | State the fair market value of the meal or event benefit and the deductible excess | The donor cannot deduct the full ticket price if a benefit was received |

| Charity auctions | Acknowledge only the deductible amount above fair market value | Winning the bid does not automatically mean the full payment is deductible |

| Noncash gifts over $5,000 | Describe the property and confirm receipt, but do not replace valuation paperwork | The donor may also need a qualified appraisal and Form 8283 support |

| Payroll deductions | Track each deduction separately and summarize qualifying amounts accurately | Small deductions are not bundled together just because the annual total looks large |

| Faith-based gifts with intangible religious benefits | Use the special exception language only when it truly applies | That exception is narrow and easy to misuse |

There is also a separate layer for noncash donations: property over $5,000 can trigger appraisal and Form 8283 requirements, and the acknowledgment does not replace those steps. I would never let a standard receipt pretend to do the work of a valuation file. That is the kind of shortcut that looks harmless in February and creates a mess later.

If your organization runs membership drives, gala campaigns, or sponsorship packages, the safest rule is to separate the charitable portion from the benefit portion before the receipt is generated. That habit prevents the next problem, which is usually not a missing signature but a letter that says too much or the wrong thing.

Common mistakes that weaken the record

The errors I see most often are not complicated. They are usually a mix of overconfidence and automation without review. The good news is that they are all fixable if you know where to look.

- Using the same template for every gift. A plain cash gift, a gala ticket, and a property donation do not belong in the same language block.

- Claiming or implying full deductibility after benefits were received. If the donor got dinner, merchandise, or admission, the receipt must say so.

- Putting a value on donated property in the acknowledgment. For noncash gifts, the letter should describe the item, not appraise it.

- Sending the letter too late. A perfect receipt that arrives after the donor files is still a compliance problem for the donor.

- Forgetting annual summaries for recurring donors. Monthly giving is easy to overlook when records are fragmented across payment systems.

- Mixing stewardship language with tax language until neither is clear. Warmth is good, but the tax statement has to remain unmistakable.

I also see one quieter mistake: organizations assume the donor will fix the record if something is missing. That is a risky assumption. The better model is to make the first version correct, then let the donor simply keep it with their tax files. Once that mindset is in place, the process becomes a controls question, not just a communications task.

The workflow I would use for a clean year-end close

If I were designing this process for a nonprofit in 2026, I would treat acknowledgments as a governance workflow, not a clerical afterthought. The goal is to create a repeatable system that protects the donor, supports the finance team, and reduces corrections in January and February.

- Classify every gift at entry as cash, recurring cash, event-related, or noncash.

- Tag any gift with benefits so the deductible portion is calculated before the receipt is sent.

- Use an automated template for standard cash gifts, but send manual review cases to development or finance.

- Reconcile gift records monthly so the year-end summary is a confirmation step, not a rescue mission.

- Batch qualifying year-end acknowledgments early enough to reach donors well before filing season.

- Keep a version-controlled template library so staff do not improvise wording during busy periods.

My preference is to keep the letter short, the data fields disciplined, and the review step visible. That is usually the difference between a nonprofit that merely says thank you and one that has a reliable, audit-ready donor record. For most organizations, the biggest win is not a prettier receipt, but a cleaner process that makes the right receipt hard to get wrong.