Strong nonprofit finance work starts with a simple question: will the organization have enough cash to deliver its mission without starving next quarter to celebrate this one? Financial planning for nonprofits is about aligning revenue timing, spending discipline, reserves, and board oversight so the mission can survive both busy months and lean ones. In practice, the best plan is not the prettiest spreadsheet; it is the one that helps leaders make faster, calmer decisions when funding shifts.

What matters most in nonprofit finance

- A useful budget connects mission goals to cash timing, not just annual totals.

- Reserve targets should be measured in months of operating expenses, with the exact level shaped by revenue volatility.

- Restricted funds, board-designated reserves, and unrestricted cash need separate rules.

- Internal controls and clean records protect compliance, accountability, and donor trust.

- The board should review a short dashboard every month, not only at year-end.

What nonprofit financial planning has to solve

I think of nonprofit finance as four jobs happening at once: allocating scarce dollars, preserving liquidity, respecting donor intent, and proving accountability. That is very different from a for-profit model, where the main question is often return on capital. Here, the real question is whether the organization can keep serving people without running into a cash crisis.

That means the plan has to deal with both strategy and operations. Strategy answers where the organization is going and what it can afford to do next. Operations answer how bills get paid, how grants are tracked, how payroll is covered, and how leaders react when a payment arrives late. When those pieces are separated, the numbers usually get cleaner, and the board stops treating finance as a once-a-quarter ritual.

In a healthy nonprofit model, the budget is not just an accounting artifact. It is the operating map for staffing, program delivery, fundraising, and risk management. Once that frame is clear, budgeting becomes much less about guessing and much more about choosing.

Build the budget around timing, not just totals

A nonprofit budget that only totals revenue and expense for the year can hide serious problems. I care more about when money arrives and when the organization has to spend it. A grant that reimburses after the work is done, for example, can look strong on paper while quietly creating a cash gap in the middle of the year.

The simplest way to make the budget more useful is to build it around assumptions, not just line items. I usually want management to explain where each dollar comes from, what can delay it, and which expenses cannot be moved without damaging service delivery.

| Budget area | What to model | Common mistake |

|---|---|---|

| Revenue | Grant timing, renewal risk, donor concentration, event seasonality, earned-income cycles | Counting pledged or expected income as if it were already cash |

| Personnel | Salaries, taxes, benefits, hiring lag, overtime, turnover cost | Underbudgeting payroll because vacant roles temporarily lower expenses |

| Program delivery | Direct service costs, supplies, travel, subcontractors, participant support | Forgetting that growth in services usually creates lagging support costs too |

| Occupancy and technology | Rent, utilities, insurance, software, equipment replacement, security | Treating these as fixed and ignoring inflation or contract renewals |

| Timing risk | Receipt delays, reimbursement lag, payment terms, large annual renewals | Ignoring the gap between when revenue is earned and when it lands in the bank |

I also like a scenario check. A base case is not enough. At minimum, I want to see a downside case where one major grant is delayed by 60 to 90 days and a stress case where one funding source falls away entirely. Those two views show whether the organization has a cushion or only a hope. A budget that cannot survive a delay is not really a plan; it is a guess with formatting.

Once the budget is built around timing, the next question is whether the organization has enough liquidity to absorb a shock.

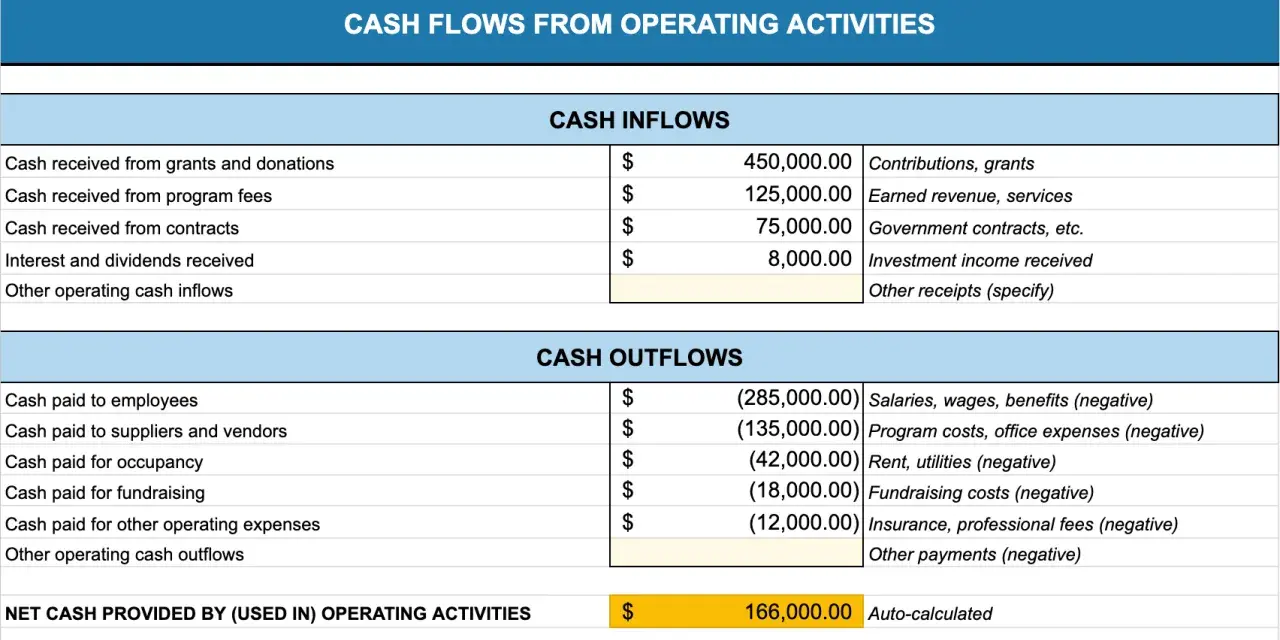

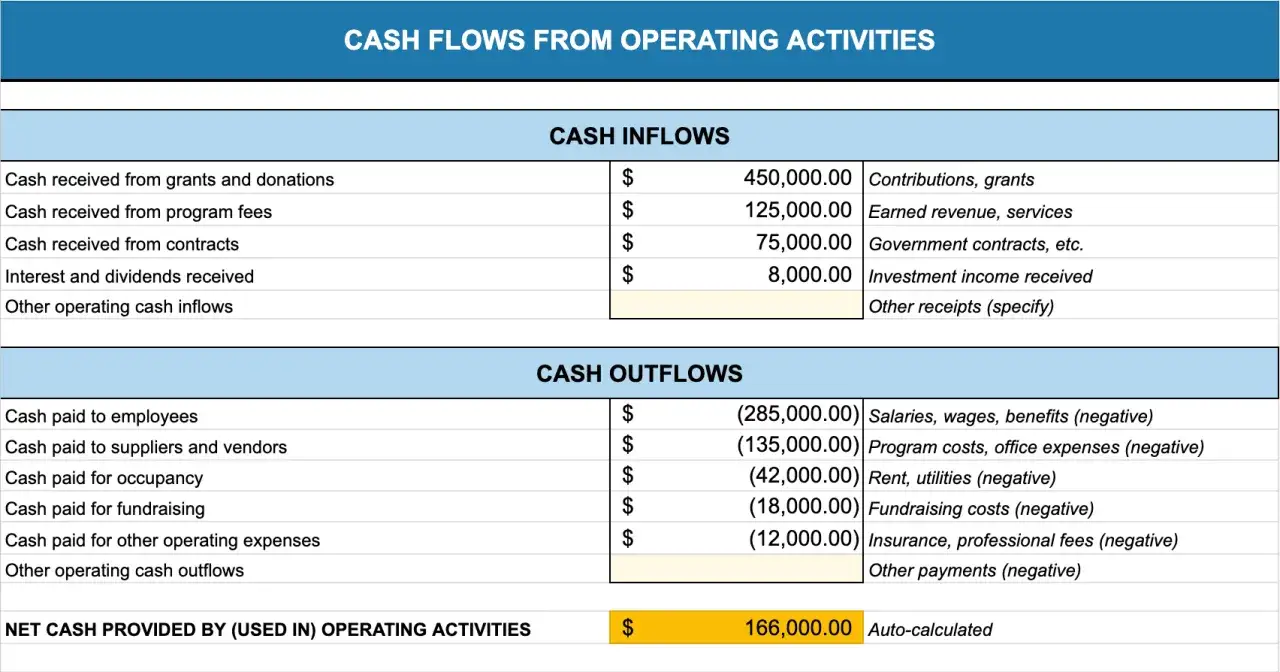

Protect liquidity with reserves and cash-flow forecasting

Liquidity is where many nonprofits feel strong in March and fragile by October. I treat two tools as essential: a rolling cash-flow forecast and an operating reserve policy. They solve different problems. The forecast protects the next 13 weeks. The reserve protects the next 13 months.

A 13-week cash forecast is one of the most practical tools in nonprofit operations because it reveals trouble early enough to respond. It does not need to be fancy. It needs to show expected inflows, scheduled outflows, the weekly opening and ending cash balance, and the timing of any large grant receipts or payroll runs. If the organization has uneven grant timing or reimbursement-based funding, I would not operate without it.

Reserve policy is the longer-range backstop. A common starting target is three to six months of operating expenses, but I would never treat that as universal. A membership-based organization with predictable revenue may live comfortably at the lower end. A service provider with delayed reimbursements, concentrated funders, or expensive payroll obligations may need more. If annual expenses are $1.2 million, for example, monthly operating cost is $100,000, so four months of reserve coverage means $400,000 and six months means $600,000.

The formula is simple:

Months of coverage = unrestricted net assets ÷ average monthly operating expenses

That number matters because it turns a vague comfort level into an actual decision. It also helps the board decide when reserves can be used and how quickly they should be rebuilt.

If I were writing a reserve policy from scratch, I would make sure it states the purpose of the reserve, the target level, the source of contributions, who can authorize a draw, what the funds may be used for, and how replenishment will happen. A reserve that can be spent but never replenished is not a policy; it is a slow decline with nicer language.

Liquidity discipline leads naturally to fund discipline, because not every dollar in the bank is available for the same purpose.

Keep restricted, unrestricted, and board-designated money separate

One of the fastest ways to damage a nonprofit budget is to confuse cash with spendable cash. A donation, grant, or surplus may sit in the same bank account, but that does not mean it can be used for any problem that appears. I have seen more finance mistakes come from bad classification than from bad arithmetic.

| Fund type | What it means | What it can pay for | Planning implication |

|---|---|---|---|

| Without donor restrictions | Money the organization can use for ordinary operations unless the board has set a policy limit | Payroll, rent, utilities, program costs, general operating needs | This is the core operating fuel and should be watched closely |

| With donor restrictions | Money given for a specific purpose, time period, or project | Only the restricted use allowed by the gift or grant terms | Budgeting must track release timing and compliance, not just cash balance |

| Board-designated reserve | Unrestricted money the board has formally set aside for stability or future use | The purpose named in the board policy, such as working capital or emergency response | Useful for stability, but it should not be treated like an unlimited backup drawer |

That distinction matters in daily operations. If a grant is restricted to youth programming, it cannot be used to cover rent unless the grant agreement allows that use. If the board designates a reserve, the funds are still part of assets without donor restrictions, but they should be managed as if they are intentionally off-limits. That discipline protects trust and prevents the organization from spending itself into a corner while still looking solvent on paper.

Once the money is properly classified, the back office has to prove it. That is where controls and records come in.

Put internal controls and recordkeeping on autopilot

The IRS expects exempt organizations to keep books and records that document receipts and expenditures, and that expectation is not optional. In practice, good recordkeeping is less about pleasing a regulator and more about making the organization auditable, understandable, and fundable. If the chart of accounts is messy, Form 990 prep gets harder, management reporting gets slower, and board oversight gets weaker.

I start with a small set of internal controls that are simple enough to follow every month:

- Segregate duties so the person who approves a payment is not the only person who can create or release it.

- Require dual review for payments above a set threshold, especially vendor setup, wire transfers, and payroll changes.

- Reconcile bank and credit card accounts monthly and have someone independent review the reconciliation.

- Keep grant files and donor letters together so restrictions, reporting deadlines, and reimbursement rules are easy to verify.

- Document expense and travel policies so staff know what is allowed before the reimbursement request is submitted.

I also like a clean close process. Every month should end with a basic financial packet: balance sheet, income statement, budget-to-actual report, cash position, and a short explanation of variances that need attention. If a nonprofit is always surprised at month-end, the problem is usually not the month-end close. The problem is the daily workflow.

With controls in place, the board can focus on oversight instead of cleanup, which is the right division of labor.

Make the board accountable for financial oversight

BoardSource is right that board oversight is fiduciary work, not ceremonial work. In plain terms, the board should not just receive the numbers; it should understand them well enough to challenge assumptions and approve strategy with confidence. That is especially important in smaller organizations where a finance committee may be light on staff support and heavy on volunteer judgment.

I want the board to see a short, consistent dashboard every month or at least every quarter. It should not be 40 pages long. It should answer the questions that matter most.

| Board metric | What it tells you | Why it matters |

|---|---|---|

| Cash on hand | How much cash is available right now | Shows whether payroll and bills can be covered without drama |

| Days of liquidity | How long the organization can operate on current cash | Turns the reserve question into something the board can actually monitor |

| Budget variance | Where actual results differ from plan | A variance over 5% on a material line deserves an explanation, not a shrug |

| Grant receivable aging | Which grants or reimbursements are still outstanding | Reveals whether cash timing risk is building quietly |

| Reserve coverage | How many months of operating expenses the reserves can cover | Shows whether the organization is resilient or exposed |

The best boards ask practical questions. What happens if one funder pays 90 days late? Which program is subsidized by unrestricted dollars, and by how much? If reserves are used, what is the replenishment plan and who owns it? I prefer boards that ask those questions early, because early questions are cheaper than late rescues.

Once the board is using the same data management is using, the organization can stop reacting to surprises and start running a finance reset on purpose.

A 90-day finance reset I would run before the next board meeting

If I had to tighten a nonprofit’s financial planning quickly, I would keep the first 90 days simple and practical. The goal is not to redesign everything at once. The goal is to create visibility, control, and enough discipline to support better decisions.

- Weeks 1 to 2 - Build a 13-week cash forecast, clean up the chart of accounts, and make sure restricted and unrestricted funds are not being mixed in reporting.

- Weeks 3 to 4 - Draft or refresh the reserve policy, define who can approve reserve use, and set a replenishment rule that is realistic.

- Weeks 5 to 8 - Review grant agreements, donor restrictions, receivable aging, payroll timing, and any expenses that regularly land outside the original budget.

- Weeks 9 to 12 - Put a board dashboard in place, test a downside scenario, and decide what the organization will do if revenue slips or expenses rise faster than expected.

That sequence works because it attacks the highest-risk failures first: bad cash visibility, weak reserve discipline, and reporting that the board cannot actually use. If I had to reduce the whole process to one rule, it would be this: plan for timing, guard liquidity, and make the board see the same numbers management sees. That is what turns nonprofit finance from a reporting exercise into an operating advantage.