What matters most in a compliant identity check

- A written program must match the institution’s size, products, and customer base.

- For individuals, the baseline data set is name, date of birth, address, and identification number.

- For business customers, the process must extend to beneficial owners and the nature of the relationship.

- Verification should be risk-based, not a one-size-fits-all checkbox.

- Weak fallback methods, especially knowledge-based questions, create more risk than they solve.

- Good programs are auditable: every decision should leave a record trail.

What customer identity verification really covers

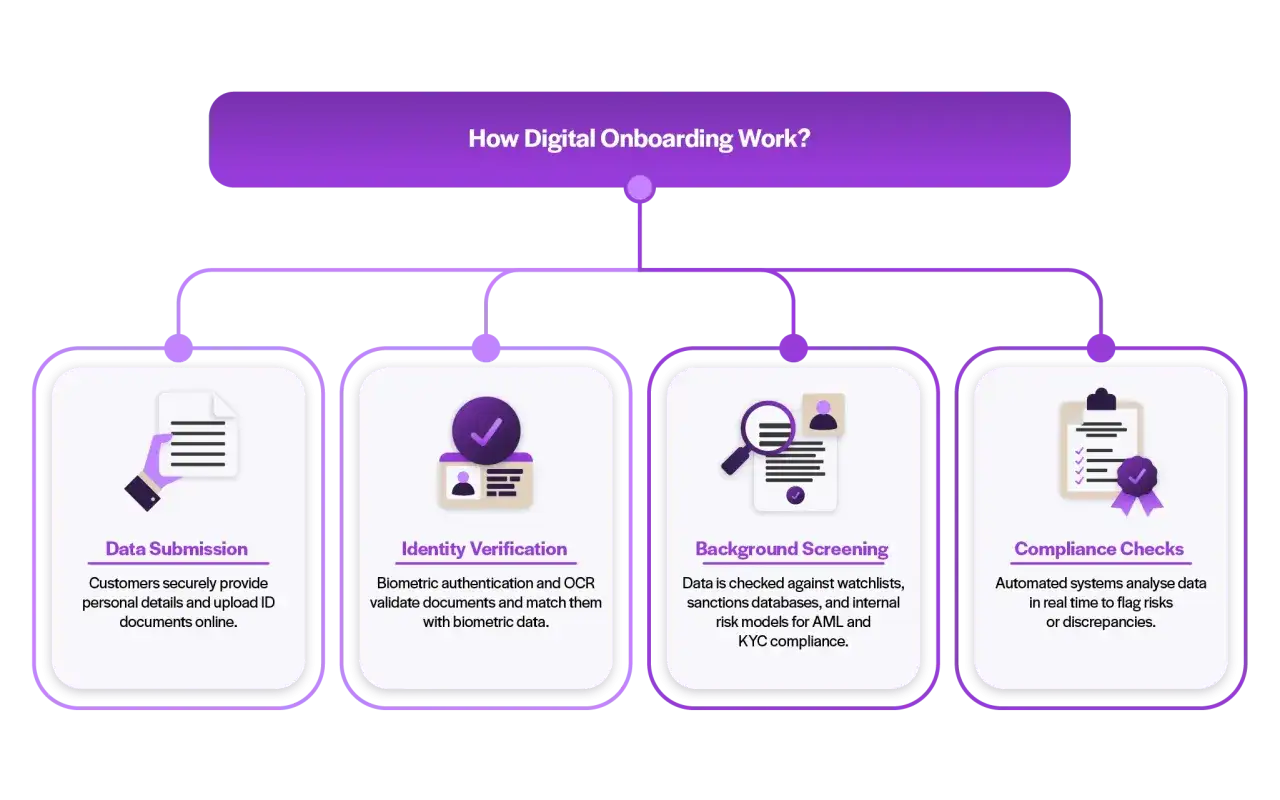

People often talk about onboarding as if it were a single gate. It is not. In practice, I treat it as three linked jobs: collect the right identity data, verify that the data is real and belongs to the applicant, and decide how much ongoing monitoring the relationship deserves.

That distinction matters because the same customer can look low risk at collection and high risk after deeper review. A consumer opening a checking account and a shell-heavy LLC opening a treasury account do not belong in the same control path, even if the front-end form looks similar. The job of the onboarding team is to make that difference visible early, not to discover it after the account is live. That takes us to the rule set behind the workflow.

The US compliance baseline that shapes the workflow

In the United States, the compliance stack is built around identity, ownership, and monitoring. FinCEN’s customer due diligence rule requires covered financial institutions to identify and verify customers, identify and verify beneficial owners of legal-entity customers, understand the nature and purpose of the relationship, and monitor for suspicious activity on an ongoing basis.

That translates into a few practical expectations that I would not ignore:

- For individuals, collect the core identifiers before or at account opening, or within a reasonable time if your process is designed that way.

- For business customers, map ownership and control, then verify the people behind the entity, not just the entity name.

- Screen names against sanctions and other prescribed lists where your program requires it.

- Keep records of what you collected, how you verified it, what failed, and what you did next.

- Make sure third-party providers do not become a blind spot; outsourcing a step does not outsource the obligation.

| Control layer | What it does | Why it matters |

|---|---|---|

| CIP | Collects core identity data and verifies the person opening the account | Proves you know who the customer is |

| CDD | Builds risk context, including ownership, purpose, and ongoing review | Turns identity into a usable risk profile |

| Sanctions screening | Checks names and transactions against restricted parties and rules | Prevents prohibited relationships and payments |

Once the baseline is clear, the next question is operational: what does a defensible flow actually look like when a customer clicks “open account”?

How I would structure a defensible onboarding flow

The cleanest onboarding flow is the one that separates capture, verification, review, and decisioning. That sounds obvious, but many programs blur those steps together and end up with a process that is fast in the demo and brittle in production.

- Classify the customer and product first. Consumer, sole proprietor, LLC, nonprofit, and cross-border relationships do not belong in the same risk lane.

- Collect the required identity fields. For individuals, that means the core data set. For entities, it means the business record plus the people who ultimately own or control it.

- Validate evidence before trusting it. A document can look clean and still be fake, expired, altered, or mismatched to the applicant.

- Verify the person is real and present. In remote flows, this is where liveness, selfie comparison, or other approved identity proofing controls belong.

- Run screening and risk checks. That includes sanctions, internal watchlists, device or velocity signals, and any adverse risk markers your policy uses.

- Route edge cases to human review. If the signal set is incomplete or conflicting, a trained reviewer should make the call rather than forcing an automatic pass or fail.

I also prefer to separate the method from the decision. Documentary verification, non-documentary checks, and manual review solve different problems, and the program should say which one is primary in each scenario.

| Method | Best use | Limitations |

|---|---|---|

| Documentary | Mainstream consumer onboarding with reliable government ID | Can be defeated by forged or manipulated documents |

| Non-documentary | Checks against credible data sources, device intelligence, and behavioral signals | Depends heavily on data quality and coverage |

| Manual review | Exceptions, mismatches, and higher-risk cases | Slower and more expensive, but often necessary |

| Knowledge-based questions | Legacy systems only, if used at all | Current digital identity guidance does not support it as a verification method |

That last row matters more than many teams admit. I would not build a modern onboarding program around security questions. The better move is to collect stronger evidence, validate it against credible sources, and use the human review layer only where the signals justify it. That becomes even more important when the customer or structure is inherently higher risk.

When standard checks are not enough

Some cases need enhanced due diligence, not just a stricter version of the same checklist. The trigger is usually not one detail on its own; it is the combination of ownership opacity, unusual activity, product complexity, and jurisdictional exposure.

| Risk signal | Why it matters | Extra control I would add |

|---|---|---|

| Complex legal entity structure | Ownership can be layered or obscured | Deeper beneficial ownership mapping and documented approvals |

| High-value or rapid movement of funds | Can indicate layering or account misuse | Source-of-funds review and tighter monitoring thresholds |

| Cross-border exposure | Increases sanctions, corruption, and traceability risk | Extra screening and periodic refresh |

| Repeated verification failures | May signal fraud, poor UX, or both | Manual review with a documented escalation path |

For legal entities, I want the process to answer four questions quickly: who is the customer, who owns or controls it, what is the expected purpose of the account, and what activity would look inconsistent with that purpose. If you cannot answer those questions confidently, the account is not ready for routine treatment.

One nuance is worth calling out. Not every mismatch is suspicious, and not every higher-risk case should be rejected. In some cases the right answer is a slower approval with tighter limits and stronger monitoring. That is why the next section matters: a compliant flow still has to feel usable.

How to keep legitimate customers moving

A lot of onboarding pain is self-inflicted. The customer is not always the problem; the form, the upload flow, or the fallback design often is. If you want lower abandonment without weakening controls, the answer is usually better orchestration, not looser standards.

- Explain the reason for each request. People cooperate more when they understand why a document or field is needed.

- Pre-fill what you can. OCR, autocomplete, and validated source data reduce typos and name mismatches.

- Give precise photo instructions. A surprising number of failures come from glare, cropping, and unreadable edges.

- Offer alternate evidence paths. Thin-file users, recent immigrants, and some business owners need a route that is not built around a single data source.

- Use save-and-resume flows. Onboarding is often interrupted; a broken session is not the same as a bad applicant.

- Make manual review visible. Silence creates support tickets, and support tickets create churn.

When I see a high drop-off rate, I do not assume the customer base is low quality. More often, the process is too rigid, the messaging is too vague, or the fallback path is missing. That is a product problem with compliance consequences, and it leads directly to the mistakes teams keep repeating.

The mistakes that create avoidable risk

The most expensive failures in onboarding are rarely dramatic. They are ordinary design mistakes that scale quietly until auditors, fraud analysts, or regulators notice them.

- Treating all customers the same. A retail checking account and a layered business structure do not deserve the same review depth.

- Optimizing only for speed. Fast approval is useful only if the underlying decision is defensible.

- Using weak fallback methods. Security questions and shallow checks create a false sense of confidence.

- Ignoring exceptions. The cases that fall outside the happy path are where the policy is actually tested.

- Failing to document decisions. If a reviewer cannot explain why a customer passed or failed, the control is weak even if the outcome was right.

- Assuming the vendor owns the risk. A provider can run a check, but your institution owns the program.

I also think teams underestimate how often a good process fails because it was not trained well. The policy can be sound and the workflow can still break if reviewers do not understand when to escalate, when to accept alternate evidence, or when to refuse an account. Measurement is what keeps those gaps visible.

What to measure once the program is live

A live onboarding program should be managed like a control system, not a launch project. The question is not whether it works on day one; the question is whether it still works when customer mix, fraud tactics, and operational volume change.

- Completion rate by channel. Web, mobile, branch, and assisted channels usually behave differently.

- Manual review rate. If this spikes, either the risk mix changed or the front-end controls are too noisy.

- Time to decision. Slow decisions can be a sign of weak automation or weak escalation design.

- Exception volume and reasons. Repeated exceptions point to a process that does not fit real customers.

- Post-onboarding alerts. If too many problems surface after approval, the front-end verification is too shallow.

- Vendor and model drift. If the tools get worse over time, the program needs recalibration, not just more volume.

For me, governance closes the loop. I want sampling, reviewer training, periodic testing, and a clear owner for each control. If a third-party provider is involved, I want evidence that the institution can explain the decision chain from input to final action. That is the point where compliance stops being theoretical and becomes operational.

The controls I would not launch without

If I were signing off on an onboarding program in the US, I would insist on four non-negotiables before launch:

- A written policy that distinguishes individual and entity customers, standard and high-risk paths, and automated and manual decisions.

- A verification method that uses strong evidence and credible validation, not just convenience.

- A documented escalation path for mismatches, exceptions, and unresolved identities.

- A reporting layer that shows whether the program is drifting, failing, or simply catching more risk than expected.

That combination is what turns identity verification into a defensible compliance process instead of a collection of vendor features. Get that right, and the rest of the onboarding experience becomes easier to improve without losing control.