A strong reserve is not a sign that a nonprofit is hoarding money. It is usually a sign that leadership understands payroll timing, grant delays, seasonal revenue, and the difference between a temporary dip and a real liquidity problem. The answer to how much money can a nonprofit have in reserve is less about a fixed ceiling and more about whether the balance is defensible for the organization’s risk profile, mission, and board policy. This article breaks down the practical benchmark, what counts as reserve money, how to build a policy that stands up to scrutiny, and when a balance starts to look excessive.

Most nonprofits should think in months of operating expenses, not one fixed dollar amount

- There is no universal federal maximum for nonprofit reserves in the United States.

- A common starting point is 3 to 6 months of operating expenses.

- Reserves should be liquid, board-approved, and separate from donor-restricted funds.

- Grant-heavy, seasonal, or reimbursement-based organizations often need a larger cushion.

- Extra cash is not automatically a problem if the board can explain the purpose and timing.

There is no federal cap, but there is a governance standard

In the U.S., no federal rule says a nonprofit may only hold a certain dollar amount in reserve. The IRS does not publish a universal reserve ceiling for charities. What it does expect is that the organization operates for its exempt purpose, files accurate public reports, and can defend its financial decisions if questioned.

The National Council of Nonprofits makes the practical point plainly: each organization needs to determine the right level of cash reserves for its own operations, and no single policy fits everyone. That is the right frame for boards. The legal question is not “Is there a magic number?” The real question is whether the reserve level is reasonable, documented, and tied to actual operational risk.

That distinction matters because a reserve that is clearly explained usually reads as stewardship, while an unexplained balance can trigger unnecessary doubt. The next step is deciding what a reasonable target looks like in practice.

What a realistic reserve target looks like in practice

For many nonprofits, the most useful starting point is 3 to 6 months of operating expenses. That benchmark is common because it gives an organization enough time to handle payroll, rent, insurance, and program delivery when revenue slows or a grant payment arrives late. I treat it as a starting point, not a law.

If you want a simple formula, use monthly recurring cash outflow multiplied by your target months. For example, if your nonprofit spends $80,000 per month on core operations, a 3-month reserve is $240,000 and a 6-month reserve is $480,000. That is much more useful than guessing from the annual budget alone.

| Risk profile | Practical reserve target | Why it makes sense |

|---|---|---|

| Stable earned income or diversified donor base | 2 to 3 months | Cash flow is more predictable, so the buffer can be smaller. |

| Typical charity with payroll, rent, and normal grant timing | 3 to 6 months | Enough room to absorb routine timing gaps and a moderate shock. |

| Seasonal revenue, reimbursement delays, or one major funder | 6 months or more | The organization is more exposed to sudden cash strain. |

| Major capital project or future expansion plan | Separate designated fund | Those dollars should not be mixed with day-to-day operating reserves. |

In other words, the right reserve is not the biggest balance you can accumulate. It is the smallest balance that keeps the organization stable when revenue slips or expenses rise. Once that number is set, you need to be clear about which dollars actually count toward it.

What counts as reserves and what should stay out of them

Not all nonprofit cash is reserve cash. A reserve is usually a pool of unrestricted or board-designated funds that the organization can use for emergencies, timing gaps, or other approved purposes. It should also be liquid enough to access quickly, because money tied up in illiquid assets does not help with payroll next week.

| Money bucket | Counts as operating reserve | Why or why not |

|---|---|---|

| Board-designated unrestricted cash | Yes | This is the cleanest form of reserve money if the board has approved the designation. |

| Operating cash in checking or savings | Usually yes | It is liquid, but it should still fit within the reserve policy. |

| Donor-restricted funds | No | Those dollars must be used for the donor’s stated purpose. |

| Endowment principal | No | Endowment money follows separate legal and governance rules. |

| Buildings, equipment, or other fixed assets | No | They may have value, but they do not pay payroll quickly. |

| Line of credit | No | Useful as backup liquidity, but it is borrowing capacity, not cash. |

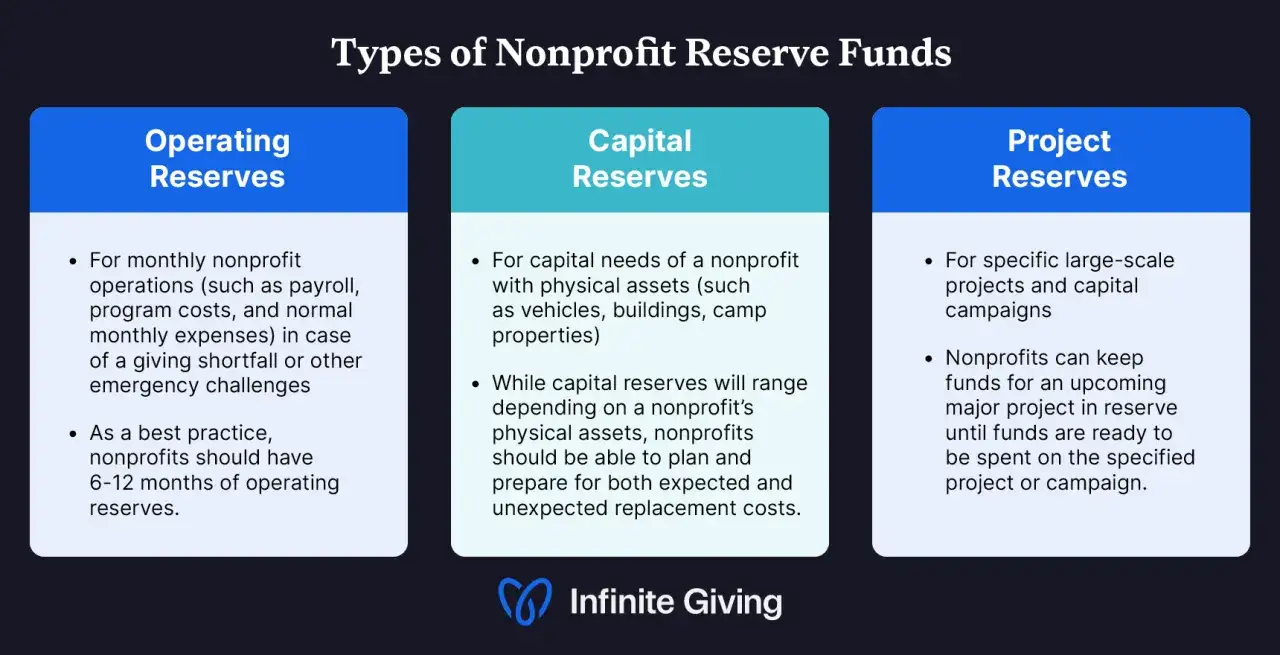

I would also separate operating reserves from capital reserves and strategic reserves. Operating reserves cover short-term survival. Capital reserves cover replacements like HVAC systems, vehicles, or technology refreshes. Strategic reserves support a board-approved growth plan, such as opening a new site or launching a program. Mixing those buckets is one of the fastest ways to make a nonprofit’s finances hard to read. With that distinction in place, the policy becomes much easier to write.

How I would build a reserve policy that a board can defend

A reserve policy is not paperwork for the file cabinet. It is the board’s operating rulebook for when the reserve exists, when it can be used, and how it gets rebuilt. The policy should be short enough to use and specific enough to answer a tough question without improvising.

- Set the target in months, not vibes. Base the number on recurring monthly operating costs and the organization’s revenue volatility.

- Define the trigger for using reserves. Spell out what qualifies, such as delayed grants, a sharp revenue drop, emergency repairs, or a temporary cash-flow bridge.

- Assign approval authority. Decide whether the executive director, finance committee, or full board must approve a draw.

- Set a replenishment plan. State how the reserve will be restored and over what period, even if that period is flexible.

- Keep the money liquid. Reserve funds should be readily available, not locked into assets that take time to sell.

- Review the policy regularly. A yearly review is usually enough, but faster-moving organizations may need quarterly monitoring.

The policy should also answer one practical question: if the reserve gets used, what happens next? A board that can answer that question has already done more than many nonprofits. It has moved from a vague safety blanket to a real risk-management tool.

Why too much cash can still be a problem

Holding a strong reserve is prudent. Holding an excessive amount without explanation is different. The problem is not that the money exists; the problem is that unused cash can become a governance issue if the board cannot explain why it is there and what it is for. Because IRS Form 990 filings are public, large balances are visible to donors, watchdog groups, journalists, and peers.

There are also three practical costs to leaving too much idle cash. First, inflation slowly erodes purchasing power. Second, donors may wonder whether the organization is underinvesting in mission delivery. Third, leadership can drift into a comfort zone where extra cash substitutes for planning. None of those issues means the reserve is wrong, but they do mean the board should be intentional.

When a reserve is larger than the organization needs for short-term stability, I usually recommend assigning the surplus to a different purpose instead of letting it sit in a vague bucket. That might mean a capital replacement fund, a strategic growth reserve, or a board-designated future program fund. Clear labels make a financial statement easier to trust.

That is why the real question is not simply whether a nonprofit can have more cash. It is whether the cash has a purpose, a policy, and a timeline that match the mission.

What I would tell a board before approving the reserve amount

If you are still asking how much money can a nonprofit have in reserve, the clean answer is that there is no single federal cap, but there is a point where the board must be able to justify the number in writing. I would ask four questions before approving the amount: How many months of core expenses does it cover? Is the money unrestricted and liquid? What event allows the board to use it? And how will it be rebuilt after a draw?

- Below 3 months can be thin for any nonprofit with payroll, rent, or grant delays.

- Between 3 and 6 months is the most defensible range for many organizations.

- Above 6 months is often fine if the revenue model is volatile or the board can explain a future use.

- Above 12 months usually deserves a separate bucket, such as a capital, strategic, or quasi-endowment fund.

My rule of thumb is simple: start with recurring monthly operating costs, test the number against your funding risk, and separate emergency reserves from long-term cash. The right reserve is not the largest balance a nonprofit can hold; it is the smallest balance that keeps payroll safe, programs steady, and the board able to sleep at night.