In risk and compliance work, the value of a verification system is not in the amount of data it can pull, but in how well it helps a team make a defensible decision. A good due diligence tool should surface ownership, sanctions exposure, adverse media, corporate history, and other signals in a way that fits the way real teams review risk. This article breaks down what the tool actually does, where it fits in U.S. compliance programs, what features matter, and how I would evaluate one before putting it in front of a board, auditor, or regulator.

What matters most before you put verification software into production

- It should help you verify facts, not just collect more documents.

- Risk-based screening beats one-size-fits-all checks in U.S. compliance programs.

- Audit trails, ownership mapping, and ongoing monitoring matter as much as initial screening.

- The best platform fits your real workflow, from intake and review to escalation and recordkeeping.

- False positives are a design problem, not just an analyst problem.

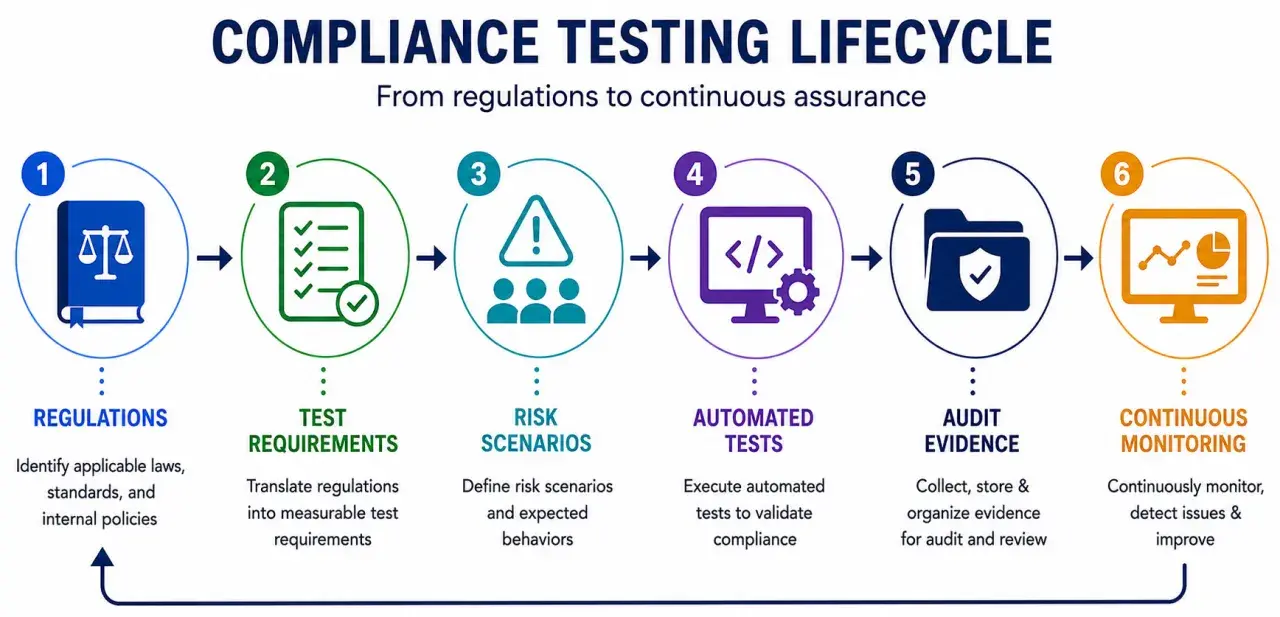

What this kind of tool actually does

At its core, this software is a verification layer. It collects structured and unstructured information, cross-checks it against trusted sources, and helps a compliance team decide whether a person, company, counterparty, or vendor is acceptable to engage. In practice, that usually means identity checks, beneficial ownership mapping, sanctions and watchlist screening, corporate registry review, adverse media searches, litigation checks, and ongoing alerts after onboarding.

The important part is the decision support. A weak system dumps results on an analyst and leaves them to interpret everything manually. A stronger one organizes the evidence, explains why a record matched, and records the review trail so the team can show how it reached its decision. I care about that because compliance failures often happen not from a lack of data, but from an inability to prove what was checked and why a risk was accepted.

That difference becomes clearer once you separate the main compliance use cases.

Where it fits in U.S. compliance work

In the United States, this kind of platform is most useful when a team must make a risk-based judgment and document it. FinCEN’s customer due diligence rule and OFAC’s sanctions framework both point in that direction: controls should be proportionate to risk, not a mechanical checkbox exercise. One practical example is PEP screening, which checks whether a person is politically exposed; that matters because public office can raise corruption and bribery risk. In my experience, that shows up in four places first.

| Use case | What gets checked | Why it matters |

|---|---|---|

| Customer onboarding | Identity, beneficial owners, sanctions, PEPs, adverse media | Helps a firm decide whether to open the relationship and what level of monitoring is needed |

| Third-party and vendor review | Ownership structure, legal history, cybersecurity signals, sanctions exposure | Reduces supply chain, vendor, and outsourcing risk before contracts are signed |

| Deal and investment screening | Litigation, regulatory actions, hidden liabilities, control changes | Supports acquisition, financing, and partnership decisions that can fail on hidden facts |

| Ongoing monitoring | Name changes, new sanctions hits, adverse news, ownership updates | Catches risk that appears after onboarding, not just at intake |

When I look at U.S. programs, I want the system to support these workflows without forcing every case through the same route. A low-risk domestic vendor should not move through the same review path as a new foreign intermediary, and a tool that cannot reflect that distinction will create noise instead of control. Once you know the setting, the next question is which capabilities actually matter.

Features that separate a useful platform from a noisy one

The best systems do not just scrape more data. They reduce uncertainty, make review faster, and preserve evidence. I look for six things every time.

| Capability | What it should do | Why it matters |

|---|---|---|

| Entity resolution | Link spelling variants, subsidiaries, parent companies, and trade names | Prevents missed matches and cuts down on duplicate records |

| Source coverage | Pull from sanctions lists, corporate registries, court records, and credible news sources | Reduces blind spots and improves the quality of the review |

| Explainability | Show exactly which fields matched and why the case was flagged | Makes analyst decisions easier to defend in an audit or inquiry |

| Workflow controls | Route cases, assign reviewers, escalate exceptions, and track approvals | Keeps investigations from getting lost in email or spreadsheets |

| Ongoing monitoring | Rescreen after onboarding and alert on relevant changes | Protects against risk drift and stale approvals |

| Reporting and retention | Export logs, timestamps, notes, and decisions in a usable format | Supports audits, governance reviews, and legal hold requirements |

How to choose one for your risk profile

I would not choose a platform by feature count. I would choose it by the questions my team answers most often and the level of proof we need to retain. A firm doing third-party risk management, for example, needs different depth than a lender focused on customer onboarding or a fund manager doing acquisition screening.

- Start with the risk type. If you screen customers, prioritize KYC, beneficial ownership, sanctions, and ongoing monitoring.

- If you screen vendors, prioritize ownership structure, cybersecurity signals, contract-linked alerts, and third-party risk questionnaires.

- If you screen deals or counterparties, prioritize litigation, regulatory history, adverse media, and source traceability.

- If you operate at scale, prioritize APIs, queue management, and automation that reduces repetitive analyst work.

- If you face audits often, prioritize exportable logs, timestamped decisions, and clear escalation rules.

I would also test how the system behaves under messy conditions, not just clean demo data. Real names are misspelled, ownership trees are incomplete, and records are often inconsistent across sources. Choosing well is only half the job; implementation decides whether the system becomes a control or just another inbox.

How to roll it out without breaking the workflow

A narrow pilot usually works better than a big-bang launch. I would map the review process first, define what counts as a match, and decide which cases need human approval before switching on automation. A focused rollout can be live in a few weeks; a broader deployment with integrations and policy updates often takes a quarter or more.

- Define the trigger. Decide exactly when a review starts: new customer, new vendor, ownership change, periodic rescreen, or event-driven alert.

- Set the evidence standard. Spell out which sources are required and which are optional.

- Calibrate thresholds. A high-risk relationship should produce tighter monitoring and faster escalation than a low-risk one.

- Train reviewers on exceptions. The hard cases are where policy language usually collapses.

- Keep a feedback loop. Review false positives and missed matches every month, then tune the rules.

I like this staged approach because it prevents a familiar failure: the team assumes the platform will create discipline on its own. It will not. The workflow still needs ownership, escalation, and periodic review. The fastest way to ruin the benefit is to assume the tool alone will enforce discipline.

Common mistakes that create false confidence

Most failures are predictable. I see the same six patterns again and again.

- Using one review path for every risk level.

- Equating a clean screen with a clean relationship.

- Ignoring beneficial ownership because it takes more work.

- Letting analysts close alerts without a written rationale.

- Relying on stale data feeds or unverified sources.

- Skipping ongoing monitoring after onboarding.

The biggest problem is usually not the software itself. It is the false sense of control that appears when the first batch of results looks organized. A screened file is not the same thing as a well understood counterparty, and compliance teams get hurt when those two ideas are treated as interchangeable. Before I trust any platform in production, I run it through a simple sign-off checklist.

What I would verify before approving it for production

Before I would sign off, I want five things to be true:

- I can explain why the system flagged or cleared a case.

- I can trace every decision back to a timestamped review record.

- I can see how the platform handles entity changes, ownership updates, and rescreening.

- I can export evidence quickly for audit, legal, or board review.

- I can connect it to the systems my team already uses, instead of asking reviewers to copy data by hand.

If a platform cannot do those five things, it is not really reducing risk. It is just moving the burden from a spreadsheet to a dashboard. The best systems make judgment clearer, review faster, and oversight easier to defend, which is exactly what a serious compliance program should demand.