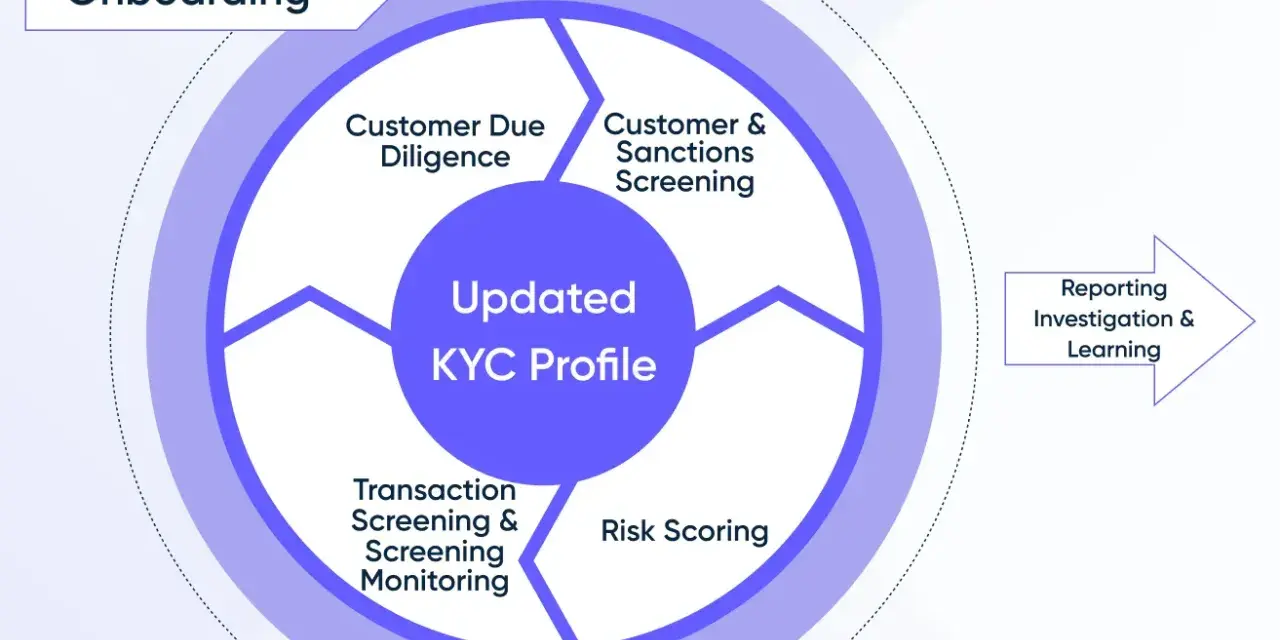

Sanctions screening is the part of KYC that turns customer data into a real compliance decision. The real job of sanctions in KYC is to catch restricted exposure before onboarding, payments, or ownership changes create an enforcement problem. In the U.S., that matters because the risk is not only a direct match on a name list; it can also sit in beneficial ownership, aliases, counterparties, or geography. This article explains how the control works, where it fits in the lifecycle, and what I would tighten first in a practical risk and compliance program.

Key points to keep in view

- KYC answers “who is the customer?” while sanctions screening answers “is this party restricted?”

- The screening layer should cover applicants, beneficial owners, signatories, and relevant counterparties.

- Risk-based design matters more than one perfect tool, because data quality and escalation discipline decide most outcomes.

- False positives are normal; the control fails only when teams cannot triage them quickly and consistently.

- For U.S. firms, sanctions exposure is a governance issue, not just a systems issue.

What sanctions screening adds to KYC

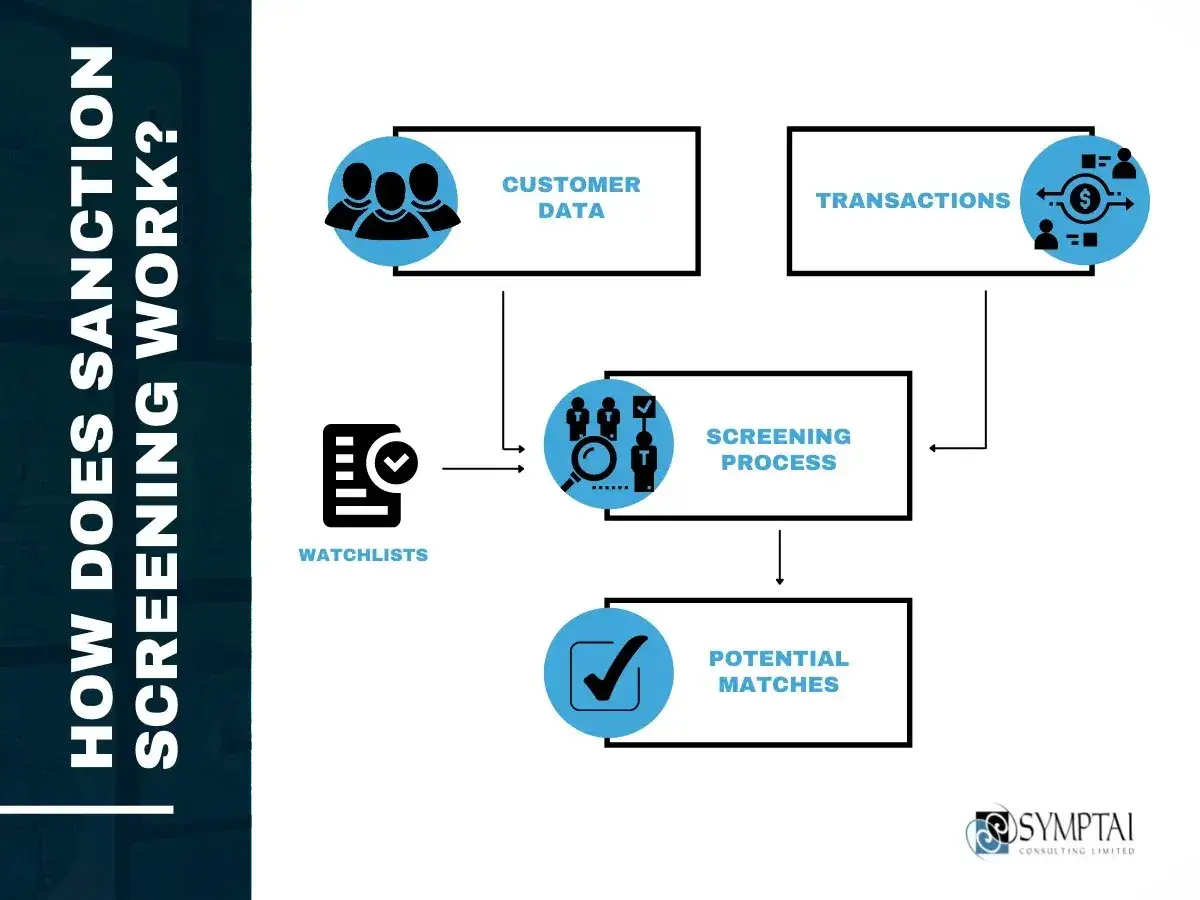

I separate identity verification from sanctions screening because they solve different problems. KYC tells me whether the customer exists, whether the ownership picture is credible, and whether the relationship makes commercial sense. Sanctions screening asks a narrower but more urgent question: does this person, entity, owner, or related party appear on a restricted list, or match a pattern that should be treated as restricted until cleared?

That distinction matters. A clean ID document does not eliminate sanctions risk, and a clean sanctions result does not prove the customer is low risk. In practice, the screening layer sits on top of the KYC file and uses that file to test names, aliases, dates of birth, addresses, ownership links, and, where relevant, countries or counterparties. The better the underlying customer data, the less noise the screening team has to manage.

| Layer | Primary question | Typical inputs | Output |

|---|---|---|---|

| KYC identity verification | Who is the customer? | Government ID, formation documents, ownership records | Verified identity and ownership profile |

| Sanctions screening | Is any party restricted? | Names, aliases, DOB, addresses, ownership links, geographies | Clear, possible match, or escalation |

| Ongoing review | Has the risk changed? | New lists, ownership updates, transaction activity, new counterparties | Update, restrict, or exit decision |

For covered institutions, FinCEN’s CDD Rule pushes the same logic further by requiring risk-based ongoing customer due diligence, including understanding the nature and purpose of the relationship and maintaining or updating customer information. That is why I treat sanctions screening as a living control, not a one-time onboarding step. Once that is clear, the next question is where the checks belong across the customer lifecycle.

Where sanctions screening belongs in the customer lifecycle

The most common mistake is placing screening only at account opening. That is too narrow for any business with changing owners, fast payments, or cross-border exposure. A workable program screens at several points, because sanctions risk can enter through the customer, the account, the transaction, or the ownership structure after the relationship is already live.

| Lifecycle stage | What to screen | Why it matters |

|---|---|---|

| Onboarding | Applicant, beneficial owners, directors, signers, known aliases | Catches obvious prohibited parties before the relationship starts |

| Periodic review | Updated customer data and refreshed lists | Captures list changes and customer changes that happened after onboarding |

| Event-driven review | Ownership changes, new jurisdictions, new product use, new counterparties | Red flags can appear when the business model changes |

| Transaction review | Originators, beneficiaries, intermediaries, related parties | Stops indirect exposure that never showed up in the original file |

There is also a practical U.S. point here: OFAC does not prescribe one mandatory software stack or a single screening frequency, but institutions still need controls that stop them from dealing with blocked parties or failing to block property. That means the workflow has to be fast enough to be useful and controlled enough to survive an audit. The next step is designing the workflow so it works under real volume instead of only in a policy document.

How to build a screening workflow that actually works

A sound workflow is less about sophistication and more about discipline. I look for seven things: complete data at intake, standardised name handling, list management, meaningful match logic, documented escalation, clear disposition rules, and re-screening when facts change. If one of those pieces is weak, the whole control degrades.

- Collect complete legal names, aliases, addresses, dates of birth, registration numbers, and ownership links.

- Standardise the data so transliteration, spacing, punctuation, and local naming patterns do not break the match logic.

- Screen against current sanctions lists and internal watchlists before the account is approved or the transaction is released.

- Triage hits with rules that separate obvious false positives from possible matches that need human review.

- Escalate uncertain cases quickly, with a documented decision trail and supporting evidence.

- Re-screen when lists update, ownership changes, or the customer’s risk profile changes.

- Test the control periodically so the team knows whether the logic still behaves as intended.

The judgment call I see teams get wrong most often is over-trusting the vendor score. A good platform helps, but it does not own the decision. When the case is ambiguous, the institution has to be able to explain why it cleared, escalated, or rejected the match. That becomes even more important when the program starts missing the same types of issues over and over, which is where the next section matters.

The failure modes that create real risk

Most sanctions failures are not dramatic. They are boring, repetitive process problems that sit unnoticed until a regulator, auditor, or payment exception exposes them. In my experience, the most expensive errors usually come from ordinary weaknesses rather than exotic typologies.

- Stale list data - if sanctions lists are not updated reliably, the program is already behind.

- Incomplete customer records - missing aliases, dates of birth, or ownership data turn accurate screening into guesswork.

- Poor transliteration and fuzzy matching - names from different scripts or languages are easy to miss if the rules are too rigid.

- No beneficial ownership mapping - the customer may look clean while the real risk sits one layer up.

- Overly aggressive tuning - if every common name becomes a false positive, analysts stop trusting the queue.

- Weak audit trails - if you cannot show why a hit was resolved, the control is harder to defend.

Another subtle failure is treating the vendor as the owner of the control. The institution owns the policy, the risk appetite, the escalation thresholds, and the final disposition. A tool can surface the issue, but it cannot decide how much risk the firm is willing to carry. Those weaknesses become more dangerous when the business has cross-border exposure or higher-velocity products, which is where U.S. tuning becomes essential.

How U.S. compliance teams should tune the program

For U.S. firms, sanctions screening is inseparable from enterprise risk management. I would not design the same controls for a domestic payroll platform, a cross-border payments business, and a trade-finance lender. The OFAC posture is risk-based, which means the control needs to fit the business model, the customer base, and the volume of transactions the institution actually processes.

| Risk profile | Typical exposure | What I would tighten |

|---|---|---|

| Lower risk | Domestic customers, limited cross-border activity, simple ownership | Daily list refresh, standard matching, clear escalation rules |

| Medium risk | Consumer fintech, marketplace flows, some international activity | More frequent review, tighter alias handling, stronger case management |

| Higher risk | Cross-border payments, trade, virtual assets, complex ownership, rapid volume growth | Enhanced review of beneficial owners, counterparties, geographies, and recurring transactions |

One practical rule is to keep the sanctions program aligned with the risk that can change fastest. If customer ownership shifts frequently, screen ownership changes aggressively. If transactions move quickly, build faster interdiction and review times. If the business touches higher-risk jurisdictions, the geography logic needs to be tighter than a generic blacklist. The point is not to make every program heavy; it is to make the control proportionate and defensible. That leads directly to the last thing I would lock down first.

The controls I would lock down first in a U.S. program

If I had to prioritise only a few controls, I would start with the ones that reduce preventable mistakes. A strong sanctions process does not need theatrical complexity; it needs consistent execution, clear ownership, and fast escalation.

- Data quality at onboarding - capture full legal names, aliases, and ownership data before the account is opened.

- List refresh discipline - make sure sanctions data is updated on a schedule that matches the risk and transaction velocity.

- Escalation ownership - every possible match should have a named reviewer and an internal deadline.

- Disposition standards - define what evidence clears a hit and what evidence requires restriction or exit.

- Independent testing - verify that the rules still work as the business, products, and customer base change.

- Management reporting - track hit rates, aging cases, overrides, and repeat false positives so leadership sees control drift early.

When sanctions screening is built into KYC as a living control, it stops being a box to tick and becomes what it should be: a practical barrier against prohibited exposure before money, ownership, or reputation are put at risk.