Cleaner books rarely come from working harder; they come from removing the repetitive steps that slow the close and invite errors. Bookkeeping automation is the practical use of software to capture transactions, route approvals, match records, and surface exceptions so people can focus on review instead of data entry. In this article, I break down what to automate first, how to choose a system, where the real risks sit, and what a sensible rollout looks like for a U.S. business.

What matters most before you automate the books

- Automate the repetitive, rules-based work first: bank feeds, receipts, invoicing, reminders, and reconciliation.

- The main payoff is not just speed; it is fewer manual touches, cleaner records, and a tighter month-end close.

- Human review still matters for exceptions, unusual journals, new vendors, payroll items, and tax-sensitive decisions.

- Software choice should follow workflow design, not the other way around.

- ROI is usually decided by setup quality, data cleanliness, and how many exceptions the system creates.

What automation changes in everyday bookkeeping

Automation does not magically make accounting strategic. It removes repetitive work so the person reviewing the books can spend time on exceptions, not transcription. In practice, that means bank feeds, receipt capture, invoice routing, recurring entries, and rule-based matching do the heavy lifting while the human role shifts to approval, explanation, and correction.

That shift matters because clean financials are usually built by reducing the number of touches between the transaction and the ledger. The software can catch the obvious items, but it should not be trusted to decide how to treat a split charge, a messy reimbursement, or a new vendor with no history. Once that shift is clear, the next question is which tasks deserve automation first.

The tasks I would automate first

When I map a bookkeeping workflow, I start with the tasks that are frequent, rule-based, and painful to do by hand. Those are the places where automation usually creates the fastest win and the least drama.

| Task | Why it automates well | What still needs review |

|---|---|---|

| Bank transaction import and categorization | Transactions arrive in a consistent format, and vendor patterns are repeatable. | New vendors, split charges, unusual amounts, and account changes. |

| Receipt capture | OCR, or optical character recognition, can read key details from invoices and receipts automatically. | Missing receipts, personal purchases, and mixed-use expenses. |

| Recurring invoicing and payment reminders | Billing cycles, due dates, and reminder sequences are easy to standardize. | Custom terms, disputed invoices, and client-specific exceptions. |

| Bank reconciliation | Matching ledger entries to bank activity follows predictable rules in most cases. | Timing differences, reversals, duplicates, and stale items. |

| Bill approval and payment routing | Approval thresholds can be defined in advance and enforced consistently. | New vendors, high-value payments, and nonstandard bills. |

| Monthly reporting | Standard reports can be generated on a schedule with the same structure each time. | Narrative commentary, unusual variances, and final review. |

If a workflow is high-volume, rule-based, and fed by consistent source data, it is usually a good candidate. If it depends on judgment, exceptions, or a one-off approval path, I keep a human in the loop until the rules are stable. After those priorities are set, implementation is less about buying software and more about designing the process around it.

How to build a workflow that survives month-end close

A good workflow starts with structure, not with features. I usually map the current process on paper first: where the transaction starts, which system touches it, who approves it, and where exceptions go. Then I automate only the repeatable part and leave a visible path for anything unusual.

- Clean the chart of accounts, vendor names, and item labels before you automate anything. Bad labels create bad rules.

- Connect bank and card feeds so transactions arrive daily instead of in a monthly pile.

- Set rules by vendor, amount, location, and account type, then keep the rule set simple enough to explain.

- Create an exception queue for split payments, new vendors, and transactions that do not match historical behavior.

- Use approvals for payments and journal entries that affect cash, payroll, sales tax, or tax filings.

- Pilot one month before scaling, because a workflow that looks good in a demo can still fail under real volume.

When AI is part of the stack, I prefer systems that learn from prior coding decisions but still show why a match was suggested. That matters because a black box may be fast, but it is hard to trust when a lender, auditor, or controller asks for support. That kind of design keeps the close predictable, which is what finance teams actually need before they compare platforms.

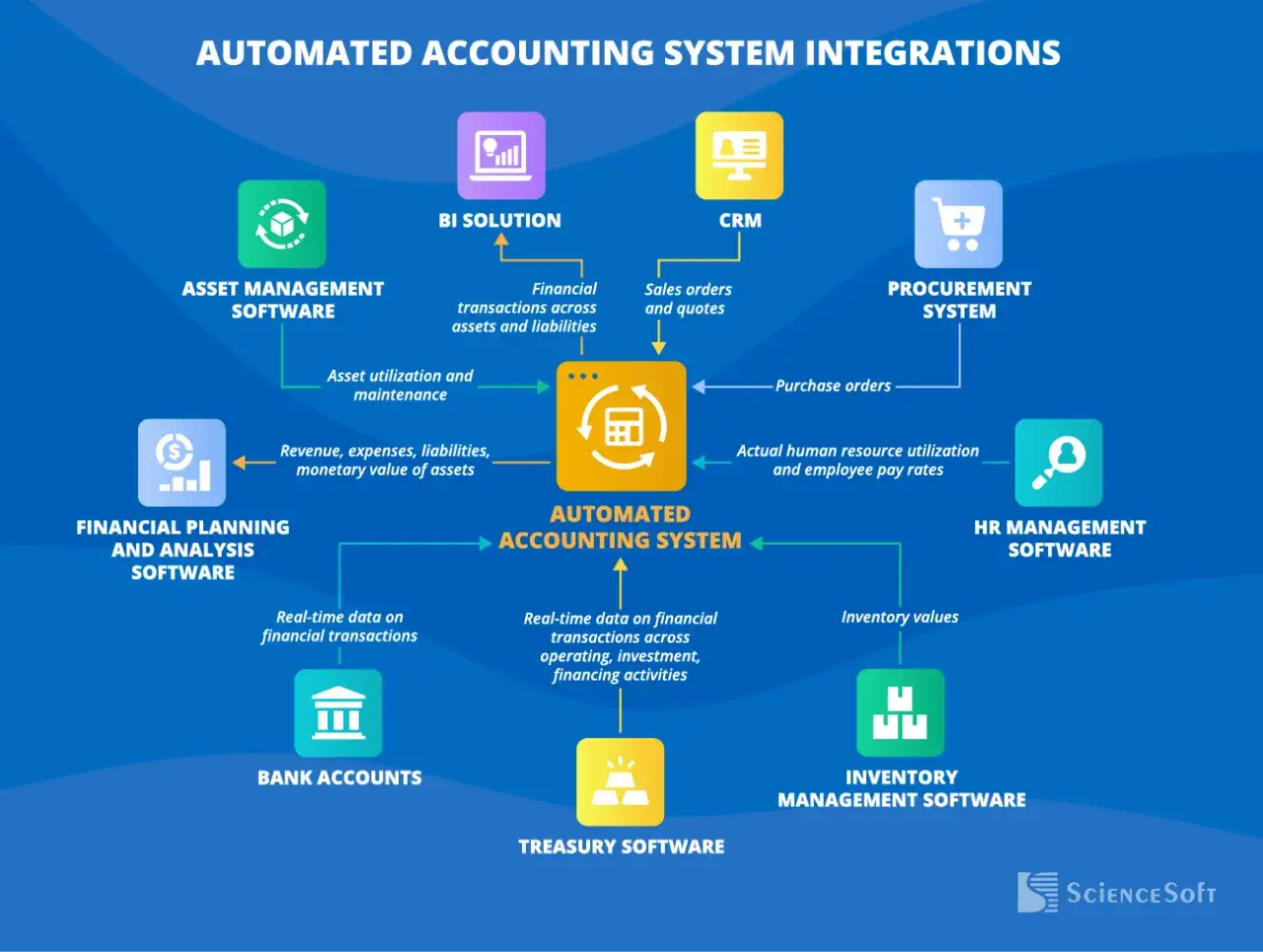

Choosing the right system for a U.S. business

The best tool is the one that fits your workflow, not the one with the longest feature list. In the U.S. market, I usually think in three buckets: all-in-one accounting suites, point tools for specific tasks, and workflow automation tools that move data between apps.

| Approach | Best for | Strengths | Limits | Typical spend |

|---|---|---|---|---|

| All-in-one cloud accounting suite | Small and midsize businesses that want one place for invoicing, bank feeds, reconciliation, and reporting. | Simple administration, strong core bookkeeping, fewer vendors to manage. | Can feel rigid as complexity grows, especially with custom workflows. | Often starts around $19 to $137.50+ per month, depending on plan depth. |

| Point tools for AP, expense, or receipt capture | Teams with a lot of bills, reimbursements, or document intake. | Better capture, faster approvals, and cleaner matching for one specific problem. | More integrations to maintain and more places for process drift. | Frequently priced per user or bundled into a broader finance stack. |

| Workflow automation or RPA | Firms stitching together older systems or repeating the same handoffs across apps. | Flexible across tools, useful for repeatable back-office handoffs. | RPA, or robotic process automation, still needs maintenance and careful rule design. | Can be low-cost for basic no-code tools, but enterprise setups are usually quote-based. |

QuickBooks and Xero are the clearest examples of the all-in-one category, and they make sense when the goal is to streamline bookkeeping without building a custom finance stack. The point is not to pick a famous platform; it is to match the tool to the volume, complexity, and approval structure of the business. The next layer is governance, because speed without controls creates hidden risk.

Controls that keep speed from becoming a liability

The governance question is simple: can you show who changed what, when, and why? If the answer is no, the system may be fast, but it is not reliable enough for serious financial work. In a U.S. setting, that matters for payroll, sales tax, 1099 work, and anything that will later be reviewed by management, a lender, a tax preparer, or an auditor.

The AICPA’s automation guidance is consistent on one point: start with repeatable workflows, but keep approval logic visible. I would add a few practical controls that tend to matter more than people expect:

- Separate data entry, approval, and payment authority wherever possible.

- Keep an audit trail of rule changes, overrides, and exception handling.

- Limit who can edit vendor master data, bank rules, and payment settings.

- Require human review for new vendors, manual journals, and any override of a matching rule.

- Store source documents in one place so every posting can be traced back to support.

- Review duplicates, stale reconciling items, and unusual reversals on a fixed schedule.

Those controls are not bureaucratic overhead. They are what keep automation from turning into invisible error propagation. Once those guardrails exist, ROI becomes much easier to measure.

What the numbers usually look like

I like to model payback in plain language: monthly hours saved, loaded labor cost, software spend, and any one-time cleanup or setup work. If automation saves time on paper but creates rework in practice, the math falls apart quickly.

| Example input | 8 hours saved per month |

|---|---|

| Loaded hourly cost | $35 to $50 |

| Monthly labor value | $280 to $400 |

| Software spend | $19 to $137.50+ per month |

| One-time setup or cleanup | $500 to $2,500 is a realistic planning range when data and workflows need cleanup |

| Payback | Often a few months if the process is stable and the team actually uses the workflow |

That is why I do not judge a system by subscription price alone. I watch three operating metrics instead: uncategorized transactions, unreconciled items, and days to close. If those move in the right direction for two or three cycles, the system is doing real work. With the economics visible, the rollout can stay deliberate instead of chaotic.

A 90-day rollout that avoids rework

- Days 1 to 30: map the current workflow, pick one repetitive process, clean the data behind it, and measure the baseline.

- Days 31 to 60: automate that single process, keep human review on the exception queue, and compare results against the baseline.

- Days 61 to 90: add one adjacent workflow, document the controls, tighten permissions, and check whether the close is actually faster and cleaner.

The safest strategy is usually the boring one: automate the repeatable 80 percent, keep the exception path explicit, and review the controls every month. That gives you faster books without losing the audit trail, and it tends to hold up better when tax season, diligence, or lender questions show up.