A solid startup cash flow forecast is less about predicting the future perfectly and more about spotting the months when cash gets tight. I use it to answer three questions: when money enters, when it leaves, and how much room the business has before it runs into trouble. For founders, that matters more than reported profit, because profit does not pay the rent on time.

The essentials that matter most before you trust the model

- Focus on cash timing, not just revenue totals, because timing is what keeps the business alive.

- Use weekly visibility for the near term and monthly projections for the first 12 months.

- Separate collections, payroll, taxes, inventory, debt service, and one-time startup costs.

- Test at least three paths: base case, slower sales, and delayed collections.

- Refresh the forecast whenever hiring, pricing, payment terms, or funding plans change.

What this forecast should tell you

A cash forecast is not the same as a profit projection. Profit tells you whether the model works on paper; cash tells you whether you can actually keep operating this month. For a startup, I want the forecast to answer four practical questions: when cash dips, how much outside capital you need, how long runway lasts, and which assumption would hurt most if it proves wrong.

That perspective changes how you read the numbers. A business can be profitable and still miss payroll if customers pay 45 days late. It can also be unprofitable for a while and still survive if inflows are disciplined and burn is controlled. Once you see the forecast as a timing tool, the next step is deciding which numbers deserve a line in it.

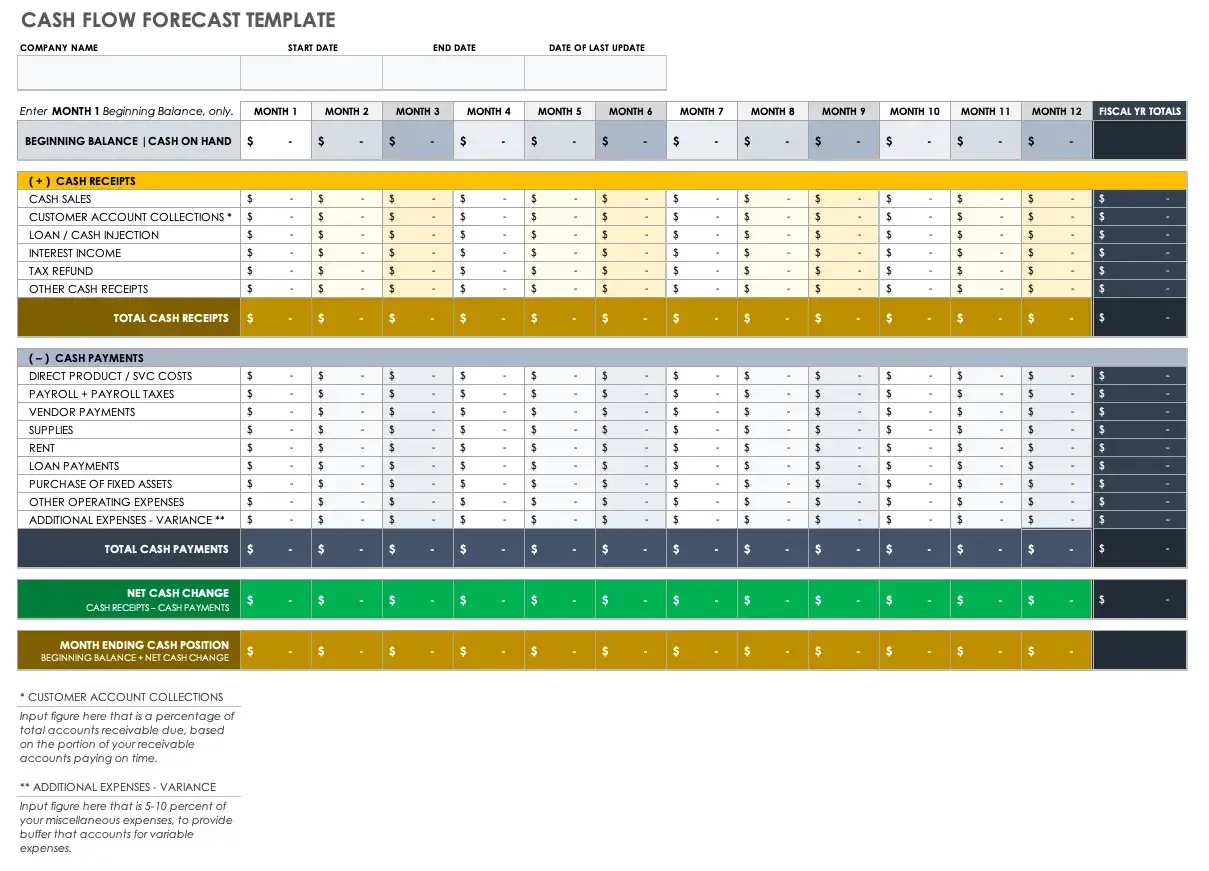

The inputs that matter most

Keep the input list lean but complete. If a line item affects when cash leaves or enters the bank, it belongs in the model.

| Forecast line | What to include | Why it gets missed |

|---|---|---|

| Cash receipts | Immediate sales, invoice collections, subscriptions, deposits, grants | Founders count booked revenue instead of actual collections |

| Payroll | Salaries, contractor payments, benefits, payroll taxes | Hiring costs are usually bigger than base salary alone |

| Operating expenses | Rent, software, insurance, legal, bookkeeping, travel | Small recurring charges are easy to understate |

| Inventory and suppliers | Stock purchases, deposits, freight, packaging | Cash leaves before inventory is sold |

| Taxes and debt | Estimated taxes, sales tax remittances, loan payments | These do not show up evenly every month |

| One-time costs | Equipment, launch campaigns, deposits, incorporation fees | They are forgotten after the excitement of opening day |

In the United States, I keep separate lines for payroll withholding, estimated taxes, and sales tax remittances because they do not move on the same schedule. If the business collects annual subscriptions or takes deposits upfront, I also separate cash received from revenue earned. That matters a lot in subscription, service, and contract-based businesses, where the income statement can look healthier than the bank balance.

I also keep depreciation out of the cash view. It matters for accounting, but not for liquidity. The equipment invoice is the cash event, not the depreciation schedule. That distinction sounds basic, but it is one of the easiest ways to make a startup model look more stable than it really is.

Once the inputs are clean, the real choice becomes how to structure the forecast, because the method you pick changes what the numbers reveal.

Choose the method that matches your business

There are two common ways to build a forecast: direct and indirect. For early-stage companies, I usually prefer the direct method because it tracks actual receipts and payments. That is the data founders need when the question is survival, not accounting elegance.

| Method | How it works | Best for | Tradeoff |

|---|---|---|---|

| Direct method | Lists expected cash in and cash out line by line | Startups, small teams, short-run liquidity planning | Needs more operational detail, especially collection timing |

| Indirect method | Starts with net income and adjusts for non-cash items and working capital changes | Board reporting, accounting analysis, later-stage businesses | Can hide the timing detail that early founders need |

If I am helping a startup that is raising money, I still build the direct view first and then translate it into a cleaner board or investor version. That keeps the story honest: the operational forecast shows how cash actually moves, and the presentation version explains what the business needs and why.

That also aligns with a basic governance rule I do not skip: the people approving spending should be able to read the model without decoding it. If the forecast cannot survive a founder, CFO, and investor looking at it together, it is not ready.

Build it step by step

I like a 13-week weekly view for the near term and a 12-month monthly view for the rest of the year. That combination catches immediate payroll pressure and the broader trends that matter for planning. It also matches the practical advice to make year-one projections more specific, usually monthly or quarterly.

Formula: ending cash = beginning cash + cash inflows - cash outflows.

- Start with actual opening cash. Use the bank balance you expect on day one, not the balance you hope to have.

- Map inflows by collection date. Put revenue where the cash lands, not where the sale was signed.

- Map outflows by payment date. Payroll, rent, software, ad spend, inventory, and vendor invoices should reflect when the money leaves.

- Separate fixed and variable costs. Fixed costs tell you the base burn; variable costs show how fast the model scales up or down.

- Add a minimum cash floor. I usually want a visible trigger point, not a vague sense that the bank account is getting thin.

- Include one-time startup items. Licenses, deposits, setup fees, and equipment can distort the first few months if you hide them in general overhead.

When you build the sheet this way, the forecast becomes readable in plain English. If month 3 looks safe only because customer payments are assumed to arrive immediately, you can see the risk before it turns into a crisis. That is the kind of visibility founders actually need, and it leads naturally into stress-testing the model.

Stress-test the forecast before you rely on it

A base case is not enough. The most useful forecast is the one that shows what happens when two assumptions are wrong at the same time.

- Revenue comes in 20% below plan. This tells you whether the business can absorb a slower launch without scrambling for emergency funding.

- Customer payments arrive 15 to 30 days late. This is especially important if you invoice clients or sell annual contracts with deferred collection.

- One hire starts a month earlier than planned. A small staffing change can move runway more than founders expect.

- Supplier or software costs rise 5% to 10%. This is a simple way to test pricing pressure and contract exposure.

- A one-time legal, tax, or compliance bill lands unexpectedly. This is the kind of event that rarely appears in optimistic plans but often shows up in real life.

For example, if you start with $180,000 and burn $30,000 a month, raw runway looks like six months. But if collections slip and a portion of receipts arrive a month late, the practical runway is shorter than the spreadsheet suggests. That is why I do not trust a forecast that cannot explain a payroll crunch in plain language.

If the downside case breaks the company, the forecast has done its job early. It has shown you where to change the plan, raise money, reduce burn, or renegotiate terms before the cash problem becomes visible to everyone else.

Avoid the errors that make the numbers lie

Most bad forecasts do not fail because the math is hard. They fail because the assumptions are sloppy.

- Using booked revenue instead of collected cash. This is the most common mistake and the fastest way to overestimate runway.

- Forgetting timing gaps. A business with strong sales can still run short if vendors get paid before customers do.

- Mixing one-time and recurring costs. Launch costs should not disappear into monthly overhead where they are easy to forget.

- Ignoring tax timing. Estimated taxes, payroll taxes, and sales tax remittances can create sudden cash pressure.

- Building only an optimistic case. A single-line forecast gives comfort, not decision support.

- Never updating actuals. A forecast that is not compared with real bank activity turns stale within weeks.

I also see founders underestimate working capital, which is the cash tied up in receivables, inventory, and vendor timing. If you need to buy product before you sell it, or invoice before you collect, the forecast has to show that gap. Otherwise the model looks fine until the balance drops faster than expected.

Once those errors are out of the way, the forecast becomes more than a spreadsheet. It becomes a control tool that supports decisions about spending, hiring, and capital raising.

Use the forecast like a control tool, not a decoration

Investors, lenders, and founders all read the same forecast differently, and that is useful. Lenders want to know whether debt service is realistic. Investors want to know when growth turns into additional capital needs. Founders want to know what to do next week if collections slip or a vendor bill lands early.

I like to keep the model tied to three operating questions:

- How much cash do we need? This is the funding question.

- When do we need it? This is the timing question.

- What happens if the assumption breaks? This is the risk question.

That framing is practical for governance too. It forces the team to explain major changes in spending, hiring, or contract terms rather than treating them as background noise. If the model says you have four months of runway, the board should know whether that figure assumes stable revenue, delayed hiring, or unusually fast collections. Silence is where bad surprises grow.

For startups with external capital, I also want version control. Keep the current forecast, the last approved version, and a short note explaining what changed. That simple discipline makes investor conversations cleaner and keeps internal decisions from drifting without anyone noticing.

The discipline that keeps it useful after launch

The first forecast is rarely the final one. The real value comes from updating it, comparing it to actuals, and changing course while there is still time to act. I would rather see a rough model that is updated every month than a polished one that no one touches after the pitch deck is finished.

As a rule, I review actual cash against forecasted cash at least once a month, and I explain any variance above 10 percent. That is usually enough to catch a slow customer, an expensive hire, a missed invoice, or a cost line that has drifted higher than planned.

If you keep the model current, it stops being a spreadsheet and becomes a decision system. That is the point: a startup cash plan should help you spend with discipline, raise money with confidence, and spot the next problem before the bank balance does.