A SAFE note is one of the cleanest ways to raise early capital when a startup is too young for a fully priced round but too promising to wait. I’ll explain how it converts, which terms actually move the economics, how it compares with a convertible note and priced equity, and what I would review before signing one in the United States.

The essentials at a glance

- It is not debt. A SAFE is a contract for future equity, so there is no interest payment or maturity date.

- Conversion happens later. The instrument typically turns into stock when the company raises a priced round or hits another trigger in the document.

- The valuation cap matters most. It sets the ceiling for the conversion price and often drives founder dilution more than the headline check size.

- Post-money SAFEs are easier to model. They let founders and investors see the ownership sold at the time of signing.

- It is fast, but not casual. The paperwork is short, yet the securities-law and cap-table consequences are real.

What the instrument is and why startups use it

In plain English, the investor wires money now and receives a contractual right to future shares later. It is usually faster than a priced equity round because the company is not negotiating a full valuation, liquidation preference stack, and board package at the same time.

Y Combinator introduced the original SAFE in 2013 and later refined it into the post-money form that many founders use now. I like the post-money approach because it makes the ownership sold at signing much easier to model, which is a real advantage when a company is raising money in pieces instead of one clean close.

It still is not current equity. Until a trigger happens, the holder usually has no ordinary stockholder rights, which is why the instrument feels lightweight even though it is legally meaningful. The real difference shows up when the next financing closes, because that is when conversion mechanics start to matter.

That leads naturally to the part founders and investors care about most: how the money turns into shares, and what decides the price.

How conversion works when the next round closes

A SAFE usually converts when the company closes a future equity financing, but the exact trigger depends on the document. Some forms also convert at acquisition or IPO, and some include specific payout or dissolution language if the company never reaches the expected round.

- The startup and investor sign the SAFE and the check is funded.

- The company records the instrument on the cap table, the ownership ledger, as a convertible security rather than stock.

- When the trigger event happens, the SAFE converts into shares under the formula in the document.

- If the SAFE has a valuation cap, that cap often sets the conversion ceiling; if it has a discount, the investor may receive the better of the two outcomes.

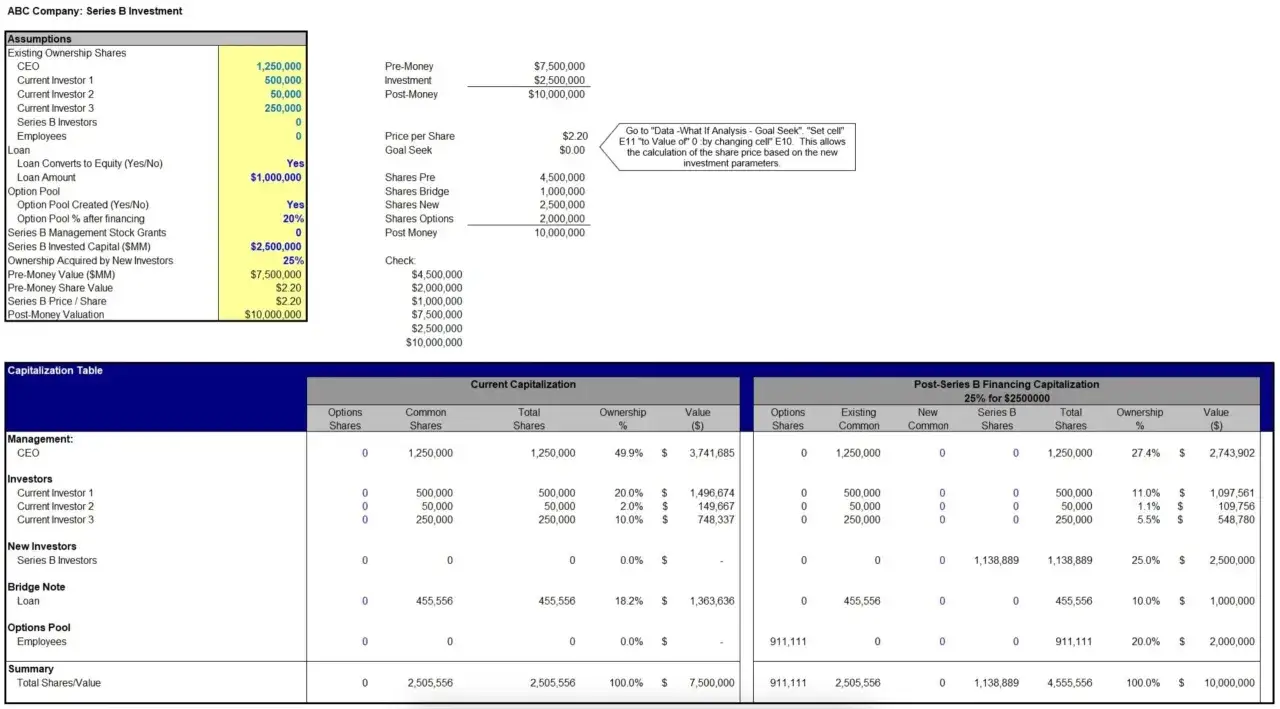

Example: if I invest $100,000 on a SAFE with a $10 million cap, and the next priced round implies a $20 million valuation, the conversion price is based on the capped terms, not the later round price. That difference can be material, especially once several SAFEs have stacked up.

The part founders sometimes miss is that the instrument can sit unresolved if the company never hits a triggering event. That is not a reason to avoid the structure, but it is a reason to document the conversion path clearly from the start. Once the conversion path is clear, the next question is which terms are doing the real economic work.

The terms that change the economics

Not all SAFEs are the same. The label on the front page tells you almost nothing about the actual economics; the cap, discount, trigger, and side-letter rights do the heavy lifting.

- Valuation cap. This is the ceiling used to calculate conversion price. It is not the company’s current valuation, and founders should not talk about it as if it were.

- Discount. This gives the investor a percentage break from the price in the next priced round. If a document offers both a cap and a discount, the investor normally gets the more favorable conversion result.

- Post-money versus pre-money. Post-money makes dilution easier to calculate because the SAFE pool is measured after the SAFE money is counted. Pre-money leaves more room for confusion if several checks close at different times.

- Most-favored-nation clauses. An MFN right lets an earlier investor match better terms granted to a later investor, which can matter more than it sounds when a round is being filled in pieces.

- Pro rata rights. These help a lead investor maintain ownership in later rounds. They are important, but they are not free; founders should think about how much future room they want to reserve.

- Trigger language and fallback rights. Acquisition, dissolution, or special repayment language can change the result dramatically if the company exits early or stalls.

I always read those terms before I look at the headline amount, because the amount alone tells only half the story. That comparison is easier once you put the SAFE beside the two common alternatives.

How it compares with convertible notes and priced equity

The practical distinction is simple: a note gives you a repayment clock, while a SAFE gives you a conversion agreement without the debt layer. A priced round is the opposite end of the spectrum; it costs more time and legal effort, but it gives everyone a current valuation and cleaner governance terms.

| Feature | SAFE | Convertible note | Priced equity round |

|---|---|---|---|

| Current legal form | Contract for future equity | Debt that may convert | Shares issued now, usually preferred stock |

| Interest and maturity | No | Usually yes | No |

| Pricing today | Usually deferred | Usually deferred, but debt terms create pressure | Set now |

| Founder speed | Fast | Moderate | Slower |

| Investor protections before conversion | Limited | Some creditor-style protections | Full shareholder rights |

| Best use case | Early seed or pre-seed capital | Bridge financing when debt terms are useful | When the company is ready to lock valuation and control terms |

In my experience, founders choose the SAFE when speed matters most, but they move to priced equity when the round is large enough that precision matters more than convenience. The deciding factor is not taste; it is the company’s stage and how much uncertainty everyone can tolerate. That stage question is where the structure either fits neatly or starts to cause friction.

When it fits and when it creates problems

Good fit. I reach for this structure when the company is early, the investor base is relatively small, and everyone expects a priced round once product and traction improve. It is also useful when the founders need to close money in pieces rather than wait for a single all-hands closing.

Poor fit. The structure starts to strain when a company is piling on multiple SAFEs across several months, when investors want current voting power, or when no one can explain how the next round will actually convert the stack. Three $250,000 SAFEs may feel harmless in isolation, but together they are already $750,000 of future dilution that has to be modeled correctly.

The other weakness is timing. If the business might not raise a priced equity round soon, or at all, the instrument can linger on the balance sheet without a natural cleanup moment. That is why I treat conversion path and timing as more important than the headline check size. If the structure still fits after that test, the last job is to get the documents and cap table right.

What I would check before signing one

Before I sign or recommend one, I want six things checked, in writing and on the model.

- Cap table math. Model every outstanding SAFE, the option pool, and the next priced round together instead of one by one.

- Trigger events. Confirm whether conversion happens only on a future equity financing or also on acquisition, IPO, or dissolution.

- Economic terms. Read the valuation cap, discount, MFN language, and any side letter before you look at the check size.

- Governance and approvals. Make sure the company has the right internal approvals and that the issuance fits the charter and securities-compliance process.

- Later-round compatibility. Ask whether a Series A lead will accept the stack as drafted or want cleanup before closing.

- Tax and accounting review. A short document can still create real tax and reporting consequences, so this should not be a purely business-side decision.

The SEC’s guidance is a useful reminder here: a SAFE is not current stock, and not every version behaves the same. That is why a quick legal review now is cheaper than unwinding a bad assumption later. With those checks done, the question becomes less about paperwork and more about strategy.

The practical takeaway for founders and investors

The best way to think about the instrument is as a speed tool with ownership consequences. It helps early capital move quickly, but it does not remove dilution, and it does not excuse sloppy modeling.

If I were advising a founder in the U.S. market, I would use this structure when the round is genuinely early, the pricing conversation would be premature, and the team can still keep the cap table disciplined. I would not use it as a way to avoid making hard valuation decisions forever. The form is simple; the outcome is not.

That is the balance that matters: use the simplicity, but price the future ownership honestly, document the trigger cleanly, and keep the financing stack easy for the next investor to understand.