Miscellaneous expenses are easy to overuse, especially when a team wants a quick place to park small charges. The better approach is to treat that bucket as a narrow exception, not a dumping ground. In this article I explain what belongs there, what should be coded elsewhere, how I would record it in a U.S. ledger, and what the 2026 tax rules mean for businesses and employees.

The main rule is to keep the bucket narrow, documented, and separate from material spending

- Use the catch-all only for truly small, incidental, infrequent costs.

- Recurring items deserve their own account, even if each charge is small.

- Bookkeeping labels and tax deductions are not the same thing, especially for employees in 2026.

- Receipts, purpose notes, and monthly review matter more than the account name.

- Capital items, payroll, rent, and personal spending should never be buried here.

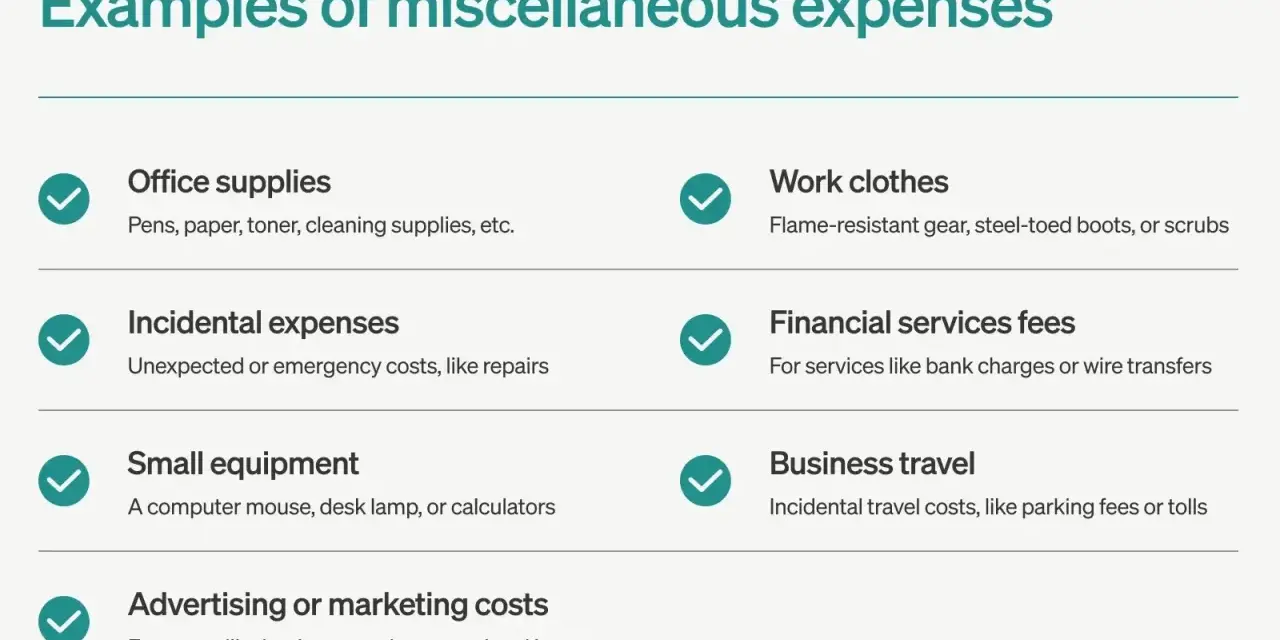

What belongs in a small-incidental-cost bucket

In accounting, I use this label for minor operating costs that are ordinary, necessary, and too small or irregular to justify their own line item. The point is not to hide detail; it is to keep the chart of accounts readable without creating twenty tiny expense accounts that no one will maintain. Materiality matters here: if a charge would not change a reasonable reader’s view of the numbers, it can usually sit in a broader bucket.

The bucket works best when it captures odd, low-value items that do not repeat with much rhythm. Once a cost starts recurring, I prefer to give it a named account because recurring items tell you something useful about operations, vendor dependence, or spending habits.

That boundary matters because the next step is deciding which transactions should sit in the bucket and which should never get near it.

Examples that usually fit and the ones that do not

When I review a ledger, I look for small charges that are real business costs but awkward to classify elsewhere. The list below is not exhaustive, but it covers the types I see most often.

| Cost | Why it fits | When I would split it out |

|---|---|---|

| Bank service charges | Usually small, incidental, and easy to separate from revenue activity | If fees become a meaningful monthly pattern, create a dedicated banking account |

| Postage and small courier runs | Often irregular and tied to one-off operational needs | If shipping becomes part of fulfillment, track it separately |

| Parking and tolls for business travel | Minor trip costs that do not justify a new account on their own | If travel is frequent, use a travel or vehicle subaccount |

| Low-value office supplies | Consumables that get used up quickly | If the purchases are recurring and visible, move them to office supplies |

| Small repairs or replacement parts | Fixes that keep equipment or operations moving | If the work extends useful life or upgrades an asset, it may be capital in nature |

| Petty cash reimbursements | Useful as a temporary landing zone for odd small outlays | If the same vendor or purpose repeats, code it to the real expense account |

What does not belong is just as important: equipment, furniture, rent, payroll, owner draws, charitable gifts, government fines, and personal costs should stay out of this bucket. A catch-all account is not a shortcut around capitalization, compensation, or nondeductible spending rules. Once you know what belongs, the next job is keeping the ledger detailed enough that the bucket does not become a blind spot.

How to record them without losing the trail

I prefer a simple three-part rule: separate, document, and review. Separate means the account should stay narrow. Document means every entry should carry the vendor, date, business purpose, and receipt when available. Review means someone should look for recurring patterns before month-end close, not six months later when the file is already messy.

- Create a narrow account for true leftovers, then add subaccounts if a pattern appears.

- Use the account only when no better category exists.

- Attach a short memo that explains why the charge belongs to the business.

- Move repeated items into their own account as soon as they stop being unusual. My rule of thumb is simple: if I see the same type of charge three times, it gets its own account.

For cash-basis books, the timing is simple: record the expense when paid. For accrual books, record it when incurred. The categorization discipline is the same either way, and that discipline matters because the tax treatment can be very different from the way the expense appears in your books.

What the U.S. tax rules mean in 2026

For tax purposes, the first question is not whether a cost feels miscellaneous; it is whether it is a deductible business expense at all. For a business owner, ordinary and necessary operating costs are generally deductible if they are not capital expenditures or another type of nondeductible outlay. On Schedule C, the catch-all section is for ordinary and necessary business expenses not deducted elsewhere, with each type listed separately.

| Taxpayer type | Typical treatment | Practical note |

|---|---|---|

| Sole proprietor or self-employed business owner | Usually deductible if the cost is ordinary, necessary, and not capital | Use the other-expenses section for true leftovers, not as a dumping ground |

| Employee | Most unreimbursed job costs are not deductible federally in 2026 | Use an employer reimbursement process instead of relying on a personal deduction |

| Special categories of workers | A few narrow exceptions still get separate treatment | Check the specific rule before assuming an exception applies |

That label does not create a deduction by itself. A charge can be legitimate in the books and still be treated differently on a return. One useful rule in 2026 is the de minimis safe harbor for tangible property: if you elect it, you may generally deduct eligible items up to $2,500 per item or invoice without an applicable financial statement, or up to $5,000 with one. That is helpful for small equipment and similar purchases, but it is still a tax election, not a reason to blur ordinary expense categories.

For employees, the narrow exceptions that still matter include certain reserve members, qualified performing artists, fee-basis state or local officials, impairment-related work expenses, and some educator costs. I mention those because people often assume every small work expense is deductible if it feels fair. It is not that simple in 2026. This is where many people make an avoidable mistake: they let bookkeeping shortcuts spill into tax assumptions. Once the tax line is clear, the next issue is governance, because the best control for a small bucket is a narrow policy that people can actually follow.

Controls that keep the bucket honest

I would not trust this account without a few guardrails. The goal is not bureaucracy; it is preventing a tiny category from becoming the place where uncertain spending disappears.

- Define the account in one sentence. If the team cannot explain what qualifies, the account is too vague.

- Require a receipt and a short business-purpose note. Small charges are easy to forget, so the documentation standard has to be simple and consistent.

- Review it monthly. That is usually frequent enough to catch patterns without slowing the close.

- Have someone other than the spender review it. A second set of eyes catches both coding drift and personal spending mistakes.

- Promote recurring items out of the bucket. If the same charge shows up every month, it is no longer miscellaneous.

- Watch for red flags. Personal purchases, government penalties, and capital items should trigger a correction, not a debate.

The best sign that the controls work is boringness. When the account stays small, predictable, and easy to explain, it is doing its job. With those controls in place, the closing process becomes a review exercise instead of a cleanup exercise.

What I would standardize before the next close

If I were tightening this for a client, I would start with four things: a written definition, a named reviewer, a receipt standard, and a trigger for moving recurring charges into their own account. That keeps the chart of accounts useful without turning it into a maze.

- Write one rule for what qualifies and one rule for what never qualifies.

- Move any repeating vendor, subscription, or travel pattern into a dedicated account.

- Keep tax treatment separate from bookkeeping labels, especially for employees and reimbursements.

- Ask whether the account helps management understand the business or merely hides detail.

The cleanest books do not eliminate small costs; they make them visible in the right place. When the catch-all account is tightly controlled, it becomes a practical tool instead of a hiding spot, and that usually makes both the monthly close and the tax file much easier to defend.