A Form 990 is one of the clearest windows into how a nonprofit actually operates. Learning how to read a 990 is mostly about separating the story the organization wants to tell from the evidence it has to provide, and that makes it useful for board members, donors, journalists, and anyone comparing nonprofits with different missions. In the sections below, I break down the parts that matter most, the schedules that reveal the real details, and the red flags that deserve a second look.

What matters most when reading a nonprofit return

- Start with the filing version and the tax year, because a full 990, a 990-EZ, and a 990-N tell very different stories.

- Read Part III before you get lost in the numbers, because mission and results should anchor everything else.

- Use Parts VIII, IX, and X together; revenue, expenses, and balance sheet data only make sense as a set.

- Check governance and compensation for accountability, but do not treat pay alone as proof of good or bad management.

- Open the schedules, especially Schedule O, because that is where many of the real explanations live.

- Compare at least two or three years before drawing a firm conclusion about performance or risk.

Start with the filing version and the tax year

The first thing I check is whether I am looking at a full Form 990, a 990-EZ, a 990-N, or a 990-PF. They are not interchangeable: a full 990 gives the richest picture, 990-EZ is abbreviated, 990-N is basically a notice for very small organizations, and 990-PF is the private foundation return with a different logic altogether.

| Version | Who usually files it | What it tells you | Why it matters |

|---|---|---|---|

| Form 990 | Most larger tax-exempt organizations | Mission, programs, revenue, expenses, governance, schedules | This is the version most readers mean when they ask about a nonprofit’s 990 |

| Form 990-EZ | Smaller organizations under IRS thresholds | Useful, but less detailed | You get some financial context, but not the same level of operational detail |

| Form 990-N | Very small organizations with gross receipts normally at or below 50,000 dollars | Basic notice only | It is not enough for serious financial or governance analysis |

| Form 990-PF | Private foundations | Investment, grantmaking, and payout information | It follows a different interpretive model, so I do not read it like a public charity return |

For context, the IRS says most organizations with gross receipts normally 50,000 dollars or less can file the 990-N, while organizations with less than 200,000 dollars in gross receipts and less than 500,000 dollars in assets may use the 990-EZ. The public copy of the return is generally available for a three-year period, which means the “latest” filing can still describe last year’s operations, not the current reality.

I also check whether the return is original, amended, or final. If I am using the public copy, I assume the schedules and attachments are part of the story, while some contributor details are not publicly disclosed for most nonprofits. Once the filing context is clear, I can move to the part that explains what the organization actually does.

Read the mission and program results first

Part III is where I look for the simplest truth: does the narrative match the mission? This section should describe the primary exempt purpose and the organization’s program service accomplishments, often with measures such as the number of people served, units delivered, or other output that actually lets me judge scale.

When the language is specific, I can tell whether the nonprofit is focused on direct services, grantmaking, advocacy, arts programming, education, or something else. When it is vague, I slow down. “Promoting community welfare” sounds nice, but it tells me very little about what changed during the year.

I pay attention to three things: new program lines, major changes in delivery method, and whether the organization is describing outputs or outcomes. Outputs are counts; outcomes are effects. A food pantry can count households served, but if it also tracks repeat visits or food insecurity reduction, I learn much more about whether the program is working.

If Part III is thin, generic, or obviously recycled from prior years, I treat it as a signal to read the schedules more carefully. That brings me to the financial sections, where the real shape of the organization becomes easier to test.

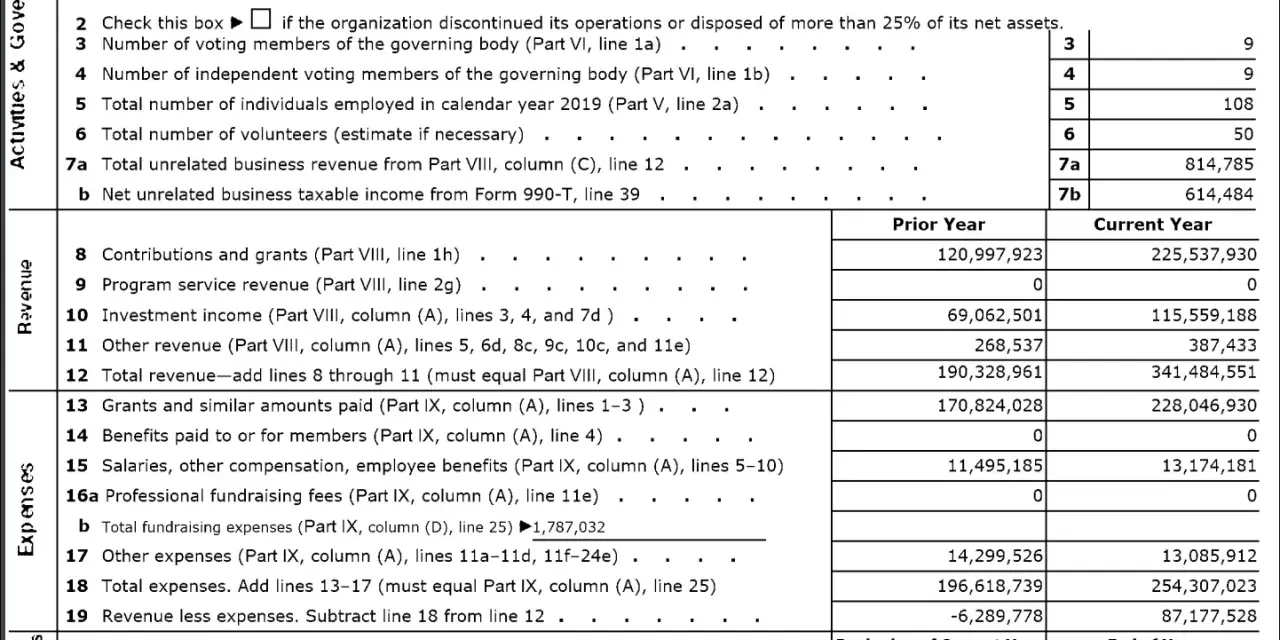

Follow the money through revenue, expenses, and net assets

I read Parts VIII, IX, and X together because each one answers a different question. Revenue tells me where the money came from, functional expenses tell me where it went, and the balance sheet tells me what the organization still has, what it owes, and how much flexibility it actually has.

| Part | What it tells me | What I look for | Common trap |

|---|---|---|---|

| Part VIII | Revenue by source | Contribution mix, earned income, investment income, unusual spikes | One-time grants that make a year look healthier than it is |

| Part IX | Functional expenses | Program, management, and fundraising spending | Thinking one ratio proves efficiency |

| Part X | Assets, liabilities, and net assets | Liquidity, debt, reserves, and restrictions | Ignoring restricted funds or assuming all cash is free cash |

There is no universal “good” program expense ratio. I have seen nonprofits with modest program percentages that were making rational investments in fundraising, compliance, or technology, and I have seen organizations with flattering ratios that were thin on mission delivery. The IRS also allows reasonable allocation methods when expenses are not captured that way in the accounting system, so I care more about consistency and explanation than about a single percentage.

The fastest way to misuse Part X is to treat it like a profit-and-loss statement. It is a snapshot. If liabilities keep climbing, unrestricted net assets keep shrinking, or a large share of assets is locked up for a specific purpose, the organization may look healthier on paper than it is in practice. When I compare at least two or three years, patterns usually become much clearer.

Once the financial picture makes sense, I check who is steering the organization and whether the compensation trail supports the story.

Use governance and compensation as accountability checks

Part VII lists the people responsible for governance and day-to-day leadership: officers, directors, trustees, and key employees. I want to know whether the board is mostly independent, whether leadership turnover is normal, and whether pay levels are understandable for the size and complexity of the mission.

- Large compensation is not automatically a problem if the organization is complex and the role is specialized.

- Compensation becomes more concerning when it is high, poorly explained, or routed through related entities.

- A board made up mostly of insiders or family members deserves closer scrutiny, especially if related-party transactions show up elsewhere.

- Former executives who remain highly paid can signal transition issues or hidden consulting arrangements.

I also read Schedule J when compensation needs more detail and Schedule L when there may be transactions with interested persons, loans, or other related-party dealings. When those details are absent, I do not assume the organization is clean; I assume I still need more context.

That is why the schedules matter so much. They are where the form stops being a snapshot and starts becoming a narrative.

Open the schedules that explain the main return

The main form gives me the skeleton, but the schedules fill in the muscle. I rarely trust the headline numbers until I have checked the supporting schedules, because that is where the form explains the messy or unusual parts of the year.

| Schedule | Why I open it | What it can reveal |

|---|---|---|

| Schedule A | Public charity status and public support | Whether the organization relies on broad public support or a narrower funding base |

| Schedule B | Contributors | Where large gifts came from, with names often redacted on the public copy for most organizations |

| Schedule C | Lobbying and political activity | Whether advocacy activity is material and properly reported |

| Schedule D | Supplemental financial details | Endowment, donor-advised funds, collections, escrow arrangements, and other special assets |

| Schedule G | Fundraising and gaming | How much outside fundraising help was used and how costly events really are |

| Schedule I | Grants and assistance | Where grant money went and how much support was delivered directly |

| Schedule J | Compensation practices | More detail on pay and benefits when compensation is complex |

| Schedule L | Interested-person transactions | Loans, leases, and related-party deals that deserve attention |

| Schedule O | Narrative explanations | The place where yes/no answers and odd situations get explained |

Schedule O is the one I rarely skip. It is where yes/no answers get explained, changes in programs are described, and odd accounting or governance situations get context. If the main form feels polished but Schedule O is full of caveats, that tension is itself information.

I also remember that the public copy does not show every contributor name for most organizations, so missing donor names are not automatically suspicious. After I finish the schedules, I am left with the final task: separating true signals from noise.

Spot red flags without overreacting to one bad ratio

Once I know where the details live, I look for patterns that deserve a second look. I am not trying to catch a nonprofit out on a technicality; I am trying to see whether the organization is operating in a way that matches its mission, model, and resources.

- Mission and results do not line up. The organization says it serves people, but Part III stays vague or counts activity without showing what was accomplished.

- Expense mix changes without explanation. Fundraising or management spending jumps while program delivery stays flat.

- Net assets keep weakening. Repeated deficits, shrinking reserves, or rising liabilities can point to cash stress.

- Compensation looks outsized or circular. Pay through related entities, consulting arrangements, or former executives still drawing large fees deserves context.

- One donor dominates the story. Heavy concentration is not illegal, but it increases funding risk and can affect independence.

- Schedules add more questions than answers. If Schedule O, L, or J reads like a series of apologies, I treat that as a signal, not a footnote.

One bad ratio rarely tells the whole story. A charity can have high management costs and still be effective if it is building infrastructure, complying with complex rules, or scaling responsibly. The better question is whether the spending pattern matches the model, the mission, and the stage of the organization. When I compare the current return with prior years and with similar nonprofits, the outliers become easier to spot and the false alarms become easier to ignore.

I also cross-check with audited financial statements when they exist, because the 990 is public and useful, but it is not the same as a full audit. That extra step helps me avoid treating a single filing as the whole truth.

What I check before I trust the story

My usual reading order is simple: confirm the filing type and tax year, read Part III for mission and results, scan Parts VIII through X for the financial shape, and then use the board, compensation, and schedules to test whether the story holds together. That sequence keeps me from overreacting to one number and helps me separate real risk from normal nonprofit complexity.

- Start with the cover page and confirm the return type.

- Read the mission and program description before you look at ratios.

- Test revenue, expenses, and net assets together, not separately.

- Check governance, compensation, and related-party disclosures.

- Compare at least two prior years and, when possible, a peer nonprofit.

If the form still leaves gaps, I treat those gaps as the next due-diligence question, not a reason to guess. That is the most reliable way I know to turn a public tax return into a useful view of nonprofit operations.