The practical answer to what happens when a nonprofit loses its status is that the organization stops getting the federal tax treatment it depended on and has to unwind the damage before it can rebuild trust. The impact usually shows up in three places at once: tax filings, donor deductibility, and public listing status. Here I break down the consequences, the IRS rules that trigger revocation, and the steps I would prioritize if I had to fix it quickly.

The immediate fallout is tax, filing, and fundraising risk

- Three consecutive years of missed required filings can trigger automatic revocation under federal law.

- Once revoked, the organization is generally no longer exempt from federal income tax and may have to file Form 1120 or Form 1041.

- A section 501(c)(3) organization loses the ability to receive tax-deductible contributions until reinstatement is approved.

- The IRS removes the organization from its public exempt-organization listings and sends a revocation letter.

- Reinstatement is possible, but it requires a new application, a user fee, and careful cleanup of any filing gaps.

How revocation actually happens

Automatic revocation is not a vague warning; it is a statutory consequence. Most tax-exempt organizations, aside from certain church-related exceptions, must file an annual return or notice. That usually means Form 990, Form 990-EZ, Form 990-PF, or Form 990-N, depending on the organization’s structure and size. If the organization misses those filings for three consecutive years, the federal exemption is revoked automatically, and the revocation is effective on the original due date of the third annual return or notice.

For small organizations that file Form 990-N, the due date is the 15th day of the 5th month after the close of the tax year. A calendar-year filer, for example, is generally due by May 15. The IRS does not assess a late-filing penalty for a late 990-N, but that is not the same as being safe. If the organization still fails to file for three straight years, the exemption is lost anyway. The IRS also publishes an automatic revocation list monthly and sends notice to the organization, so the change becomes public quickly. Once that is clear, the next question is what the loss actually changes in day-to-day operations.

What changes the moment exemption is lost

Once tax-exempt status is gone, the organization is no longer exempt from federal income tax. That can push it into filing one of the regular corporate or trust returns, such as Form 1120 or Form 1041, and it may owe income tax on taxable income earned during the revoked period. In practice, that means the revocation is not just a compliance issue; it can become a cash-flow issue.

| Area | What changes | Why it matters |

|---|---|---|

| Federal tax | The organization may need to file Form 1120 or Form 1041 and pay applicable income taxes | Unexpected tax liability can drain reserves fast |

| Donations | A section 501(c)(3) organization can no longer receive tax-deductible contributions while revoked | Fundraising language and donor receipts have to change immediately |

| Public status | The organization is removed from the IRS public exempt-organization listings until reinstated | Outside parties lose the easy verification they rely on |

| State and local rules | State and local laws may also be affected | A separate review is often needed in each jurisdiction |

There is one important nuance I do not like boards to miss: donors can still deduct contributions made before the organization’s name appears on the Automatic Revocation List. After that point, the deduction problem becomes much harder to ignore. I usually treat that as the line between a contained filing issue and a broader governance problem. From there, the priority shifts to what the organization should do immediately.

The first 30 days should focus on control, not explanations

I usually separate the first month into a cleanup phase and a restoration phase. The cleanup phase is about facts, records, and deadlines, not public statements. The biggest mistake is waiting for the IRS to “fix” the situation on its own.

- Confirm the exact revocation date and the three filing years that caused it.

- Identify which annual form the organization should have filed, including whether it was a 990-N filer or a full-return filer.

- Check the revocation letter and the IRS list against the organization’s internal records.

- Assign one person, usually with board oversight, to manage the IRS application and any cleanup filings.

- Review state registrations, solicitation filings, and other local compliance items that could be affected.

- Pause any claim that donors can rely on tax deductibility until the status is restored.

One procedural point matters here. If the revocation was automatic for nonfiling, the IRS says the organization does not need to file the returns that were already delinquent at the time of automatic revocation, but it must comply with filing requirements after revocation to avoid new penalties. That distinction saves time, but only if the organization reacts quickly and keeps later filings current. Once that is under control, the next step is reinstatement itself.

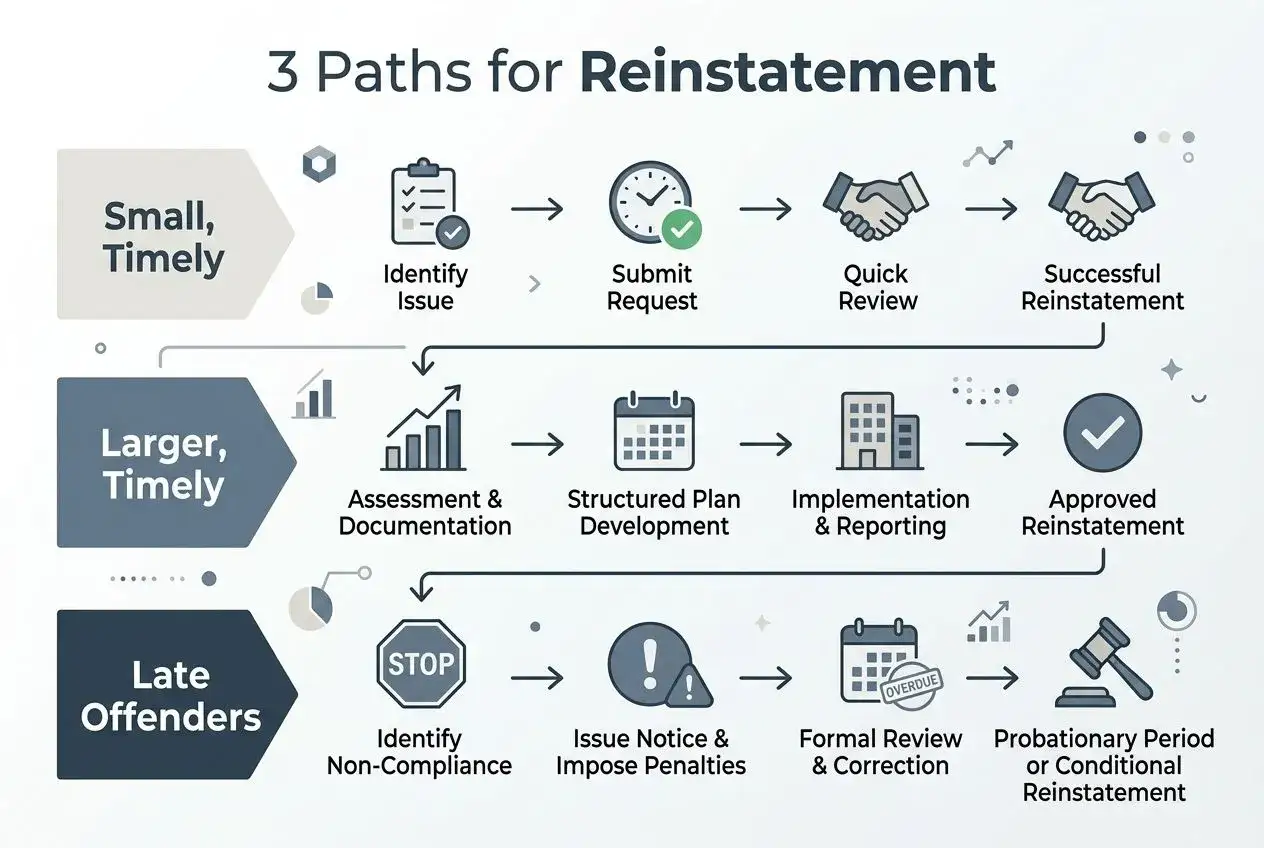

How to restore exemption and what the IRS expects next

Reinstatement is not automatic, even when the revocation was clearly caused by missed filings. The organization must apply for recognition of exemption again, using the appropriate form for its tax category, and it must pay the required user fee. For section 501(c)(3) organizations, that usually means Form 1023 or Form 1023-EZ. Other exempt organizations may use Form 1024 or Form 1024-A, or a letter in some cases.

The organization also does not need a new EIN. It must use the EIN it already has. The IRS will not automatically expedite a revoked organization’s reinstatement application, although expedited review may still be requested if the organization independently meets the existing criteria. If the application is approved, the IRS issues a new determination letter and updates the public records so the organization can again be treated as eligible to receive tax-deductible contributions.

| Reinstatement path | Typical use | Practical effect |

|---|---|---|

| Standard reinstatement | Forward-looking fix after the application is filed and approved | The effective date usually starts on the application filing date |

| Retroactive reinstatement | Used when the organization wants status treated as restored back to the revocation date | Requires reasonable cause and IRS approval |

If the organization is still waiting on approval, the filing rules depend on size. A group eligible to submit Form 990-N generally does not have to file that notice until the reinstatement application is approved. An organization that is not eligible for Form 990-N must keep filing annual information returns for each taxable year that ends while the application is pending, marking the return as application pending. That detail matters because many organizations accidentally create a second compliance problem while trying to solve the first one. The more complex issue is whether the organization can recover the revoked period retroactively.

Retroactive relief can clean up the gap, but only if you document it

In many cases, the organization can ask the IRS to make the reinstatement effective as of the date of automatic revocation. That is not a default outcome; it depends on how the application is prepared and whether the IRS accepts the organization’s reasonable-cause explanation for the missed filings. If the request is granted, the organization can reduce the damage caused by the gap between revocation and reinstatement.

The timing also affects how hard the filing process becomes. The IRS has separate procedural lanes for requests made within 15 months of the later of the revocation letter date or the date the organization appeared on the revocation list, and requests made after that window. The later route is stricter because the organization must establish reasonable cause for all three missed years. If the organization already paid income tax or received penalty notices during the revoked period, it can ask the IRS for abatement or a refund after reinstatement by sending a letter with the new determination letter, or by filing an amended return if tax was already paid. That is one reason I prefer a paper trail that is tight from the start: the IRS wants evidence, not just a story.

The mistakes that make recovery slower than it should be

I see the same errors repeatedly, and they are usually avoidable. The nonprofit is rarely hurt by a single bad filing alone; it is hurt by the confusion that follows.

- Assuming a late Form 990-N is harmless because there is no late-filing penalty.

- Waiting for the IRS to restore status automatically instead of filing the reinstatement application.

- Applying for a new EIN when the organization is supposed to use the old one.

- Stopping all filings while the reinstatement request is pending, even when annual returns are still due.

- Sending donor-facing materials that imply tax deductibility before the public IRS record is updated.

- Failing to document reasonable cause clearly enough for retroactive relief.

The real governance mistake is treating revocation like a bookkeeping issue. It is a board-level compliance failure, and if the organization responds with a board-level fix, recovery is usually much cleaner. That leads to the part that matters after the IRS letter is resolved: how to keep this from happening again.

A stronger compliance system is the real fix

The best long-term response is not just regaining the exemption. It is building a compliance system that makes future loss much less likely. I would start with a filing calendar that names one owner, one backup reviewer, and one board reporting cadence. Then I would add reminders tied to the organization’s actual tax year, not a generic calendar note that gets ignored.

I would also keep the reinstatement letter, the effective date, and any reasonable-cause file in the same compliance folder as the board minutes, banking records, and donor materials. If the organization works with grantmakers, banks, or state agencies, that paper trail should be ready before anyone asks for it. The point is simple: recovering exemption is valuable, but proving you can stay compliant is what protects the organization next.

That is the real lesson here. A nonprofit that restores its status but leaves the same controls in place has not solved the problem; it has only paused it.