Alternative financing for startups usually comes down to one thing: what kind of capital the business can survive right now. I look at it as a set of tradeoffs between speed, control, dilution, and repayment pressure, not as a single bucket of “nontraditional” money. In practice, the right choice depends on whether the company is pre-revenue, already generating cash, or building something that needs more time than a bank or standard lender will allow.

The right funding source depends on stage, cash flow, and how much control you can give up

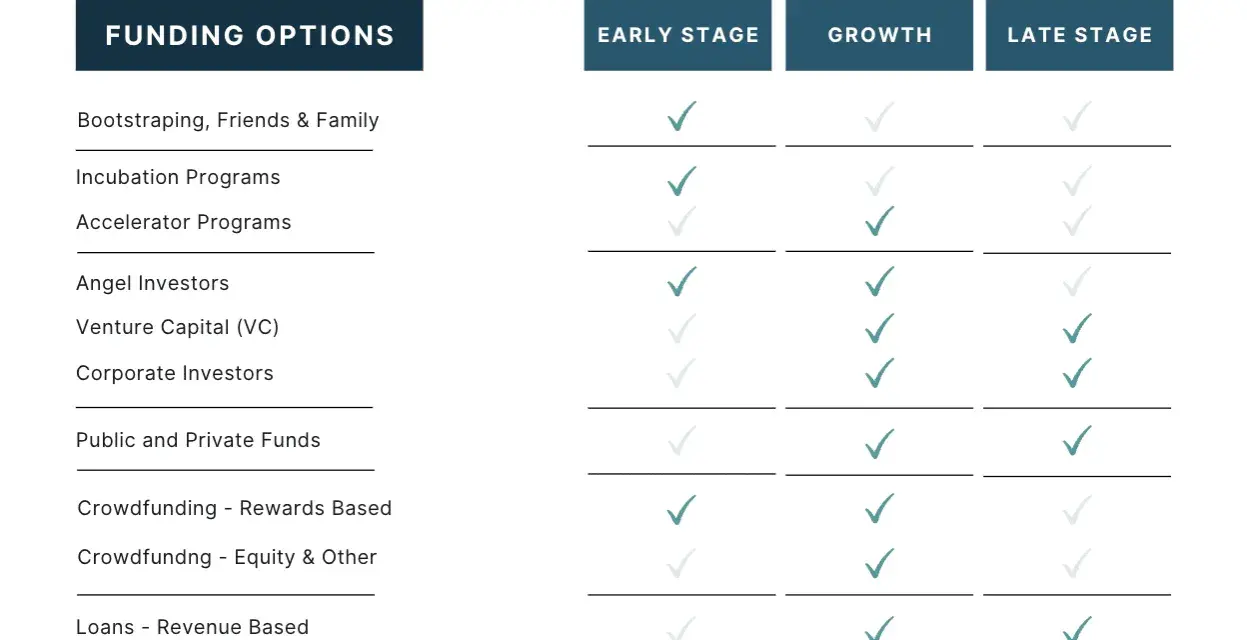

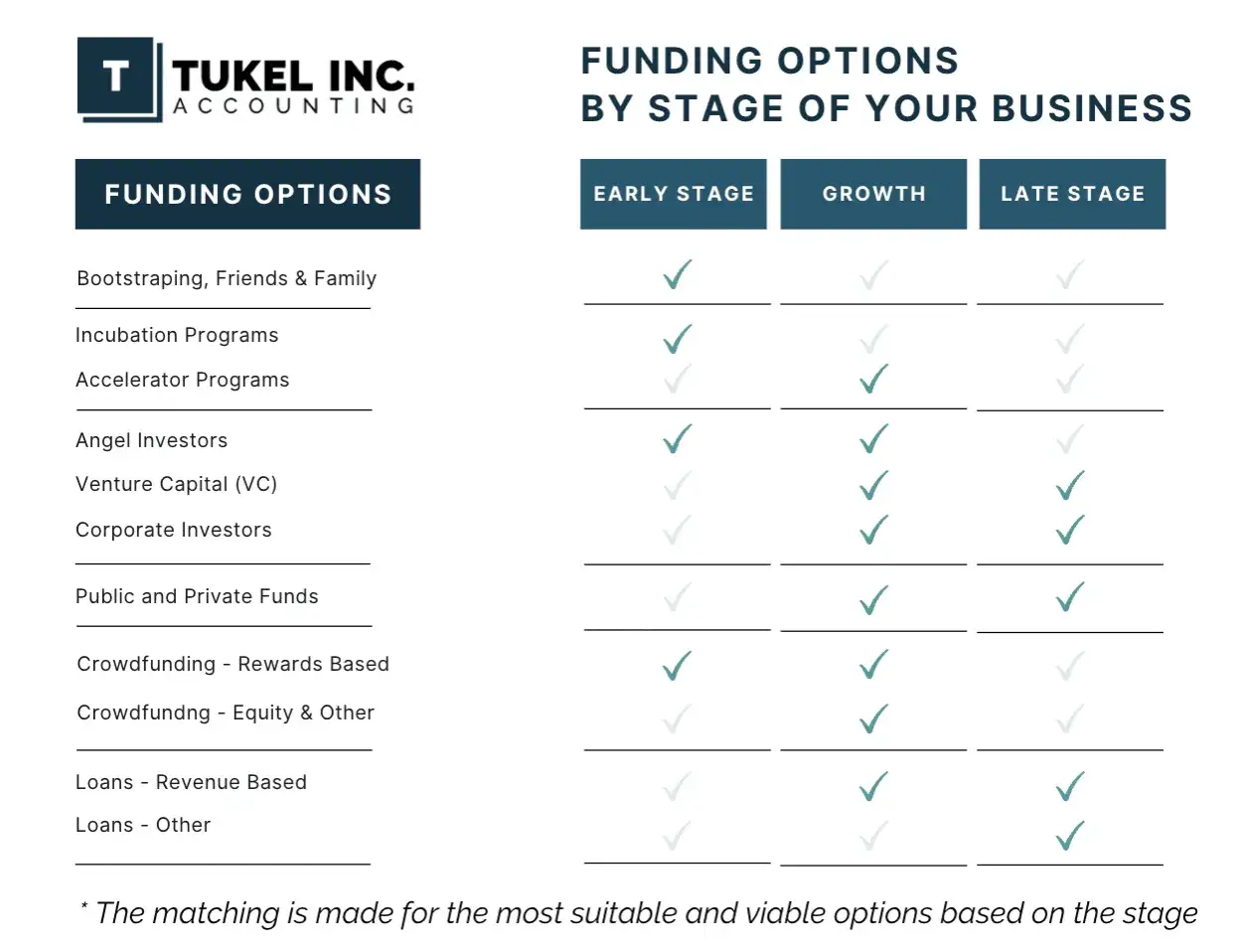

- Pre-revenue startups usually lean on bootstrapping, friends and family, angels, or R&D-focused grants.

- Revenue-based financing and microloans make more sense once the business can show predictable cash flow.

- Venture debt is usually a later-stage tool for VC-backed companies, not a substitute for missing traction.

- Crowdfunding works best when the product has a public story and the team can market it well.

- The headline cost is only part of the story; dilution, fees, covenants, and compliance can matter just as much.

What alternative startup financing actually covers

I usually split startup capital into three buckets. Non-dilutive capital does not give away ownership, but it often comes with restrictions, repayment, or both. Dilutive capital means you sell equity and accept that future upside is shared. Hybrid structures sit in the middle, which is why they confuse founders who want a simple answer.

That distinction matters because the wrong category can wreck a cap table, drain cash flow, or create legal cleanup later. A founder who understands the bucket first can usually ignore a lot of noisy funding advice. Once you separate the capital types, the next question is which sources actually fit each stage.

The main funding routes and where each one fits

When I compare startup funding sources, I care less about the label and more about the fit. A fast round that does not match the business model can be more expensive than a slower source that gives the company room to breathe.

| Funding route | Best fit | Main tradeoff | Practical note |

|---|---|---|---|

| Bootstrapping | Lean service businesses, software prototypes, early validation | Slower growth and more founder cash at risk | Best when the product can reach proof of concept without outside money |

| Friends and family | Very early runway and first hires | Relationship risk if expectations are not written down | Use a real agreement, even for small checks |

| Angel investors | Pre-seed and seed companies with a credible story | Dilution and investor expectations | Angels often bring networks, advice, and early credibility |

| Venture capital | High-growth companies with a large market | Meaningful dilution and stronger governance pressure | Usually a fit when the business can scale very quickly |

| Crowdfunding | Consumer products, community brands, mission-driven launches | Public disclosure, marketing effort, and cap-table complexity | Under SEC rules, eligible companies can raise up to $5 million in a 12-month period through an SEC-registered portal |

| Grants and SBIR/STTR | R&D-heavy, technical, or commercialization-driven startups | Competitive applications and restricted use of funds | Strong non-dilutive capital, but not a general-purpose operating cushion |

| SBA microloans | Working capital, inventory, equipment, small expansion needs | Smaller tickets, collateral, and a personal guarantee | The SBA program goes up to $50,000 and averages about $13,000 |

| Revenue-based financing | Businesses with steady sales and decent margins | Cash flow pressure if revenue dips | Repayment flexes with sales, so it works best when revenue is predictable |

| Venture debt | Investor-backed startups between equity rounds | Covenants, refinancing risk, and the need for discipline | Usually complements equity rather than replacing it |

I read that table as a sequence, not a shopping list. The real question is which source can fund the next milestone without creating a problem the company cannot refinance later. From here, I care more about ownership and governance than the label on the term sheet.

What you give up when the money is not a standard loan

Every funding source has a hidden price. Sometimes it is obvious, like interest or a repayment schedule. Other times it shows up later as dilution, board control, or extra legal work that a first-time founder did not budget for.

Dilution is the quiet cost

When you sell equity, or sign a SAFE that will convert later, you are trading future upside for cash today. A cap table is the ownership ledger of the company, and even a small early round can matter a lot if it is stacked badly.

I usually tell founders to think in percentages of the company they are willing to part with across the next two or three rounds, not just the current one. That is where many “cheap” deals become expensive.

Control can change before ownership feels dramatic

Ownership is not the whole story. Board seats, veto rights, investor consent rights, and liquidation preferences can change how the company is run long before the founder feels heavily diluted. A liquidation preference is the rule that sets who gets paid first in an exit, and that can reshape the economics even when the valuation looks strong.

If you want to keep decision-making flexible, I would avoid overcomplicated terms early unless the capital is buying a real strategic advantage.

Paperwork is where casual money turns into real risk

Money from friends, family, angels, or crowdfunding should be documented cleanly. If the deal is equity-like, you are dealing with securities law, disclosure expectations, and the future need to explain the cap table to lawyers, accountants, and later investors.

A SAFE is a contract that converts into equity later. A convertible note is debt that can convert later and usually includes interest and a maturity date. They are useful tools, but they are not casual promises, and I would not treat them that way.

Once the legal and ownership tradeoffs are clear, the limits of grants and public programs become easier to evaluate.

Why grants and public programs are narrower than most founders expect

There are no federal grants for starting a generic for-profit business. The public-money path is usually research-driven, especially SBIR/STTR-style programs that are built to support innovation, prototyping, and commercialization rather than everyday operating burn.

The upside is obvious: this is non-dilutive capital. The catch is that it usually comes with a slower process, tighter eligibility rules, reporting requirements, and funds that can only be used for specific work. That makes it powerful for the right startup and useless for the wrong one.

- Use grants when the business has a real research, technical, or commercialization milestone.

- Do not count on grant money to solve next month’s payroll problem.

- Assume the application and review cycle will take time.

- Treat the award as strategic capital, not emergency capital.

In practice, the startups that win with grants use them to de-risk the hardest part of the product, then move to private capital once the evidence is stronger. That brings us to the practical part: choosing the right mix for the company you actually have.

How to choose the right mix for your stage and model

I usually ask four questions before I recommend a funding route: Is there revenue, is it predictable, how fast must the company grow, and how much ownership is the founder willing to trade? Those answers usually point to one or two sensible options and rule out the rest.

Pre-revenue startups

If the business is still pre-revenue, I usually start with bootstrapping, friends and family, angel capital, or grants. Crowdfunding can also work if the product is easy to explain and has a visible audience.

- Bootstrapping makes sense when the product can be tested cheaply.

- Friends and family work when the amount is modest and the agreement is explicit.

- Angels help when the story is credible and the market is large enough to matter.

- Grants fit technical work that has a research or commercialization angle.

I would avoid revenue-based financing here, because the company does not yet have the predictable revenue stream that makes that structure tolerable.

Early revenue businesses

Once a startup has steady sales, the menu expands. Microloans, revenue-based financing, and small angel rounds all become more realistic. If the company needs inventory, equipment, or working capital, the SBA microloan path can be especially practical.- Microloans are useful for small tickets and local support.

- Revenue-based financing fits businesses with repeatable sales and manageable margins.

- Angel capital still matters when the founder wants growth without a heavy bank-style repayment schedule.

The test I use is simple: if a slow month would make the financing feel dangerous, the structure is too tight for the business.

Scale-up companies

When the startup is chasing a large market and needs speed, venture capital starts to make more sense. At that point, venture debt can become useful too, but usually only after a priced equity round has already de-risked the company.

- VC is best when the market opportunity is large enough to justify aggressive growth.

- Venture debt works best as runway extension, not as the first serious funding source.

- Hybrid financing can help bridge the gap between rounds without forcing a big equity raise too early.

Venture debt is not a replacement for traction; it is a tool for companies that already look investable and need extra time or flexibility.

Read Also: Business vs. Personal Credit Card - Which Is Right for You?

R&D-heavy startups

For deep-tech, biotech, climate, hardware, and other research-heavy businesses, I would look at grants first, then bring in angels or strategic investors, and only then consider VC if the market really supports scale.

- SBIR/STTR can de-risk the hardest technical work.

- Angels and strategics can bridge the company to the next milestone.

- VC becomes relevant when the tech path is credible and the commercial upside is large.

For these companies, financing should follow the milestone map, not the other way around. Even with the right match, founders still make avoidable mistakes that raise the real cost.

The mistakes that make nontraditional capital more expensive than it should be

I see the same errors repeatedly, and most of them are avoidable. The issue is rarely that the capital is “bad”; it is usually that the founder chose the wrong tool for the job or failed to price the tradeoff honestly.

- Taking the fastest money instead of the money that fits the model.

- Using high-cost capital, including merchant cash advance style products, to solve a problem that really needs product validation or equity.

- Accepting investor money without understanding dilution, preferences, and governance rights.

- Leaving friends and family funding informal and undocumented.

- Assuming a grant is won before the award is signed.

- Matching a short repayment period to a product that will not generate cash for 12 to 24 months.

If a lender quotes a factor rate instead of a transparent cost, I would immediately convert it into an apples-to-apples comparison before saying yes. My rule is simple: if the financing structure forces the company to behave like a different business, it is probably the wrong structure.

The capital stack I would choose first in 2026

If I were building a startup in 2026, I would think in stacks rather than single rounds. The right sequence depends on the business model, but the pattern is usually the same: prove the idea cheaply, de-risk the hardest part, then scale with the least painful form of capital available.

- Lean software startup - bootstrap to MVP, then use angels or a SAFE if traction is real, then consider venture debt only after recurring revenue is stable.

- Consumer brand or e-commerce business - use pre-sales or crowdfunding to validate demand, then bring in angel capital, then add revenue-based financing once sales are predictable.

- Deep-tech or biotech startup - start with grants or SBIR/STTR, then add angels or strategic capital, then use VC when the technical path is de-risked.

- Local service business - bootstrap and use microloans before anything dilutive, because control and cash discipline matter more than a large headline check.

The practical advantage of thinking this way is that it keeps you from overcommitting to one source too early. In most cases, the strongest funding plan is a sequence: prove, de-risk, then scale.