Nonprofit leaders rarely lose money because of one big mistake; more often, the leak is in how they plan, classify, and review the cost of raising money. In practice, fundraising expenses are not just vendor invoices or gala budgets, but the full mix of staff time, overhead, software, printing, and event costs tied to securing gifts. This article breaks down what counts, how to allocate shared costs, how the IRS expects them to appear on Form 990, and how I would judge whether the spending is actually worth it.

Here is the practical way to think about fundraising costs

- The IRS treats fundraising spending broadly, including allocable overhead tied to soliciting gifts, grants, and bequests.

- Direct event costs are not the same as total fundraising function costs, and they are reported separately.

- Shared salaries, rent, software, and administrative support need a documented allocation method.

- Under current Form 990 instructions, professional fundraising services above $15,000 and fundraising event activity above $15,000 can trigger Schedule G reporting.

- A healthy cost structure is measured by net revenue, donor retention, and payback period, not just by a single efficiency ratio.

- The safest system is disciplined tracking and honest allocation, not trying to make the overhead line look artificially thin.

What counts as fundraising costs

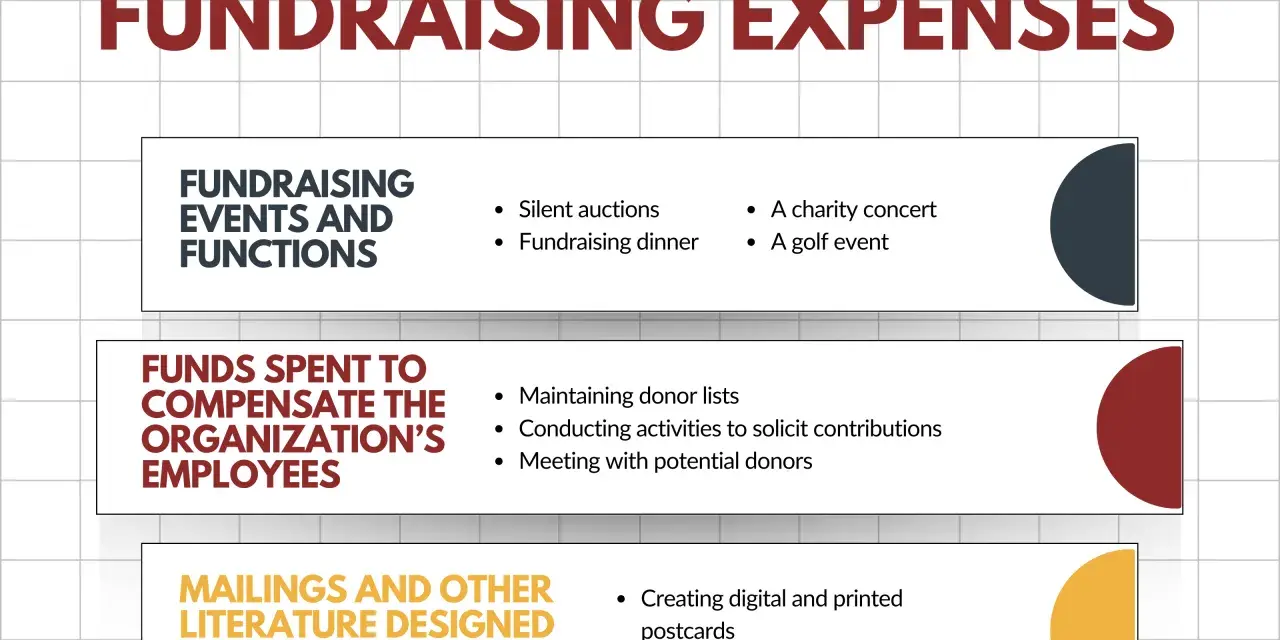

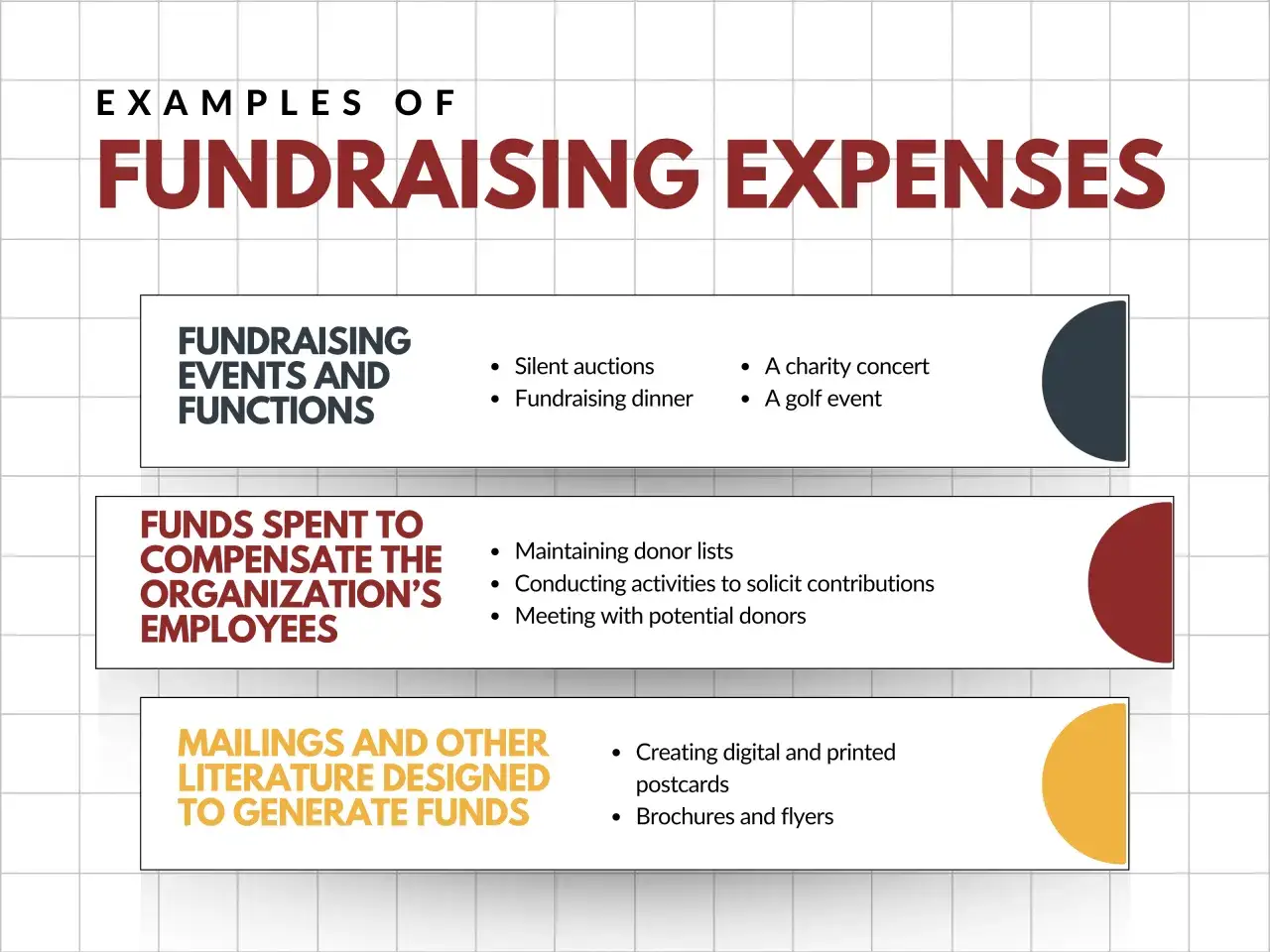

At a basic level, these are the costs an organization incurs to solicit cash and noncash contributions, gifts, and grants. The IRS definition is broad enough to include publicizing campaigns, preparing solicitation materials, seeking bequests, and the allocable overhead attached to those activities. In plain English, if a dollar of spending exists because the organization is trying to raise money, there is a good chance it belongs here.

That usually includes staff compensation, benefits, donor database tools, direct mail production, postage, online ads, grant writing support, consultant fees, and the logistics of fundraising events. It can also include a slice of office rent, accounting, IT, and executive time if those resources support fundraising work. I prefer to think of this as revenue production cost, because that framing forces the organization to ask whether the cost is generating durable support or just activity.

There is one important caveat: not every donor-facing effort is automatically a fundraising cost in every context. A stewardship email, a volunteer appreciation piece, or a community awareness campaign may support development, but the classification depends on its actual purpose and how closely it is tied to solicitation. The next step is separating the costs you can point to directly from the ones you have to allocate.

How I separate direct, indirect, and shared costs

This is the part where many nonprofit budgets get fuzzy. A direct cost can be linked to one fundraising activity with a high degree of accuracy. An indirect cost supports more than one activity and has to be distributed using a reasonable allocation method. That allocation process is often called functional allocation, which simply means assigning shared spending to program, management, or fundraising based on actual use.

| Cost type | Typical examples | Usual treatment | Common mistake |

|---|---|---|---|

| Direct fundraising | Appeal printing, postage, gala venue, ticket platform fees, grant writer invoices, donor ad spend | Charge to fundraising because the expense is tied to a specific solicitation activity | Parking it in general overhead just to make fundraising look cheaper |

| Shared staff time | Development director, executive director, communications staff, finance support | Allocate by time, project logs, or another consistent method | Charging 100% of salary to one function when the person works across several functions |

| Shared overhead | Rent, utilities, insurance, IT support, software used across departments | Allocate on a documented basis that reflects usage or benefit | Leaving overhead unassigned because the accounting system is not set up for allocation |

| Event-related expenses | Catering, auction items, décor, event staffing, registration materials | Separate the direct event cost from broader fundraising function spending | Mixing event costs with unrelated solicitation expenses and losing visibility into margin |

When I review nonprofit books, this is usually where cleanup creates the fastest improvement in credibility. Once the allocation rules are clear, the reporting side becomes much easier to defend.

How the IRS wants nonprofit fundraising costs reported

For Form 990 purposes, the fundraising function sits in Part IX, column D. The IRS treats fundraising as the expense of soliciting cash and noncash contributions, gifts, and grants, including allocable overhead. Direct expenses of fundraising events are reported separately on Part VIII, line 8b, while some indirect event costs, such as certain advertising, belong in the fundraising function instead. That distinction is more than technical; it changes how revenue and expense appear on the return.

There are also reporting triggers worth knowing. Under current instructions, a nonprofit generally completes Schedule G, Part I if it reports more than $15,000 of expenses for professional fundraising services. It completes Schedule G, Part II if fundraising event gross income and contributions exceed $15,000. If the organization uses outside fundraisers, it should also keep clear records of contracts, oral agreements, and the split between service fees and reimbursable expenses.

The dinner example in the IRS instructions is useful because it shows how easy it is to misread event income. If a guest pays $250 for a dinner with a $100 meal value, the organization reports $100 as gross income from the event and $150 as a contribution related to the event. That is a classic quid pro quo contribution, meaning the donor receives something of value in exchange for part of the payment. The organization should not shove the whole amount into program revenue just because the event supported the mission.

One practical habit I recommend is to document three things for every campaign or event: what was bought, who benefited, and how the cost was allocated. That simple file often saves a great deal of trouble later, especially when a board member, auditor, or grantmaker asks why a line item moved.

Once the reporting mechanics are clear, the harder question becomes whether the spending level is healthy in the first place. That is where performance metrics matter.

What a healthy cost structure looks like

There is no universal benchmark that tells me a nonprofit is spending the “right” amount on development. I would be wary of any rule that says low fundraising spend is always good, because some of the best fundraising programs are expensive upfront and highly profitable over time. What matters is whether the organization is buying future support, not just paying for the appearance of efficiency.

These are the metrics I find most useful:

| Metric | How to read it | What I watch for |

|---|---|---|

| Cost per dollar raised | Total fundraising cost divided by fundraising revenue | How much it costs to generate one dollar of support |

| Net revenue from campaign | Revenue minus direct and allocated campaign cost | Whether the activity actually produced cash for the mission |

| Donor retention | Percentage of donors who give again | Whether the organization is building repeat support instead of constantly replacing donors |

| Payback period | Time needed for a donor acquisition cost to be recovered | Whether the campaign is too slow to justify its upfront cost |

A simple example makes this concrete. If a campaign costs $12,000 and raises $40,000, the cost to raise one dollar is $0.30 and the net revenue is $28,000. That can be perfectly acceptable if the campaign also converts first-time donors into repeat givers. But if the same $40,000 requires $28,000 in total cost, the remaining margin shrinks to $12,000, and I would want a very good explanation for why that campaign deserves to continue.

This is also where board conversations need discipline. A low cost ratio can be meaningless if the organization is underinvesting in donor cultivation, and a high ratio can still be rational if the campaign is building a major gifts pipeline or unlocking restricted support. In other words, the metric is a signal, not a verdict.

With that in mind, the real job is not to chase the lowest possible cost; it is to make the spending controllable, understandable, and worth repeating. That leads directly to the operational side of the equation.

How to keep costs under control without weakening results

The best cost control starts before the campaign launches. I would rather see a nonprofit build a narrow, well-measured fundraising plan than scatter money across too many channels and hope the averages work out. The goal is to reduce waste, not to starve the development function.

- Choose the channel based on expected donor value, not just short-term cash.

- Budget stewardship and follow-up, because retention is usually cheaper than acquisition.

- Use a written allocation policy for salaries, shared software, and overhead.

- Review vendor contracts for printing, mailing, gala production, and platform fees before renewal.

- Track campaign results by cohort so you can see which donors return and which do not.

- Set board-level approval thresholds for unusually large event or consulting spend.

The quickest wins usually come from cleaner processes, not heroic savings. Better data hygiene, tighter vendor scopes, and more honest internal reporting often free up more money than slashing staff or cutting donor communication. I also think organizations underestimate the value of a consistent approval chain; when everyone knows who can commit spend, the budget stops leaking through side agreements and one-off exceptions.

If I had to choose one area not to cut too aggressively, it would be stewardship. The second gift is often cheaper than the first, and repeat support is where a fundraising program starts to look like a system instead of a series of expensive resets. A nonprofit that understands this tends to spend more intelligently, even when the total budget is not large.

The decision rule I would use before the next campaign

Before approving a campaign, I would ask four questions: can I explain the cost in one sentence, can I defend the allocation method, does the effort create repeatable donor value, and can I show net revenue rather than just gross receipts. If the answer to any of those is weak, the campaign is probably too loosely managed.

That rule keeps the conversation grounded in governance instead of optics. A good fundraising program is not the one that looks cheapest on paper; it is the one that can prove it is converting money spent into durable support for the mission.

If you manage nonprofit operations, the practical takeaway is simple: classify costs honestly, document allocations consistently, and evaluate each campaign on the full return it creates. That approach is more defensible to the board, easier to audit, and far more useful than chasing a vanity efficiency number.