A charity can have strong programs and still run into trouble if the finance side is loose. Good non profit money management is less about squeezing every dollar and more about making sure cash, restrictions, and reporting all line up with mission. In practice, that means knowing what can be spent, when bills will hit, who approves transactions, and which filings keep the organization in good standing.

The strongest nonprofit finance systems protect cash, donor intent, and board oversight at the same time

- Budgeting only works when it is tied to cash flow, not just revenue on paper.

- Internal controls matter even in small teams, because weak controls are how errors and misuse start.

- Restricted gifts, board-designated reserves, and operating cash should never be treated as interchangeable.

- The board should receive a short, regular packet with budget-to-actual results, cash runway, and major risks.

- As of 2026, the IRS filing level depends on size, and federal awards of $1 million or more can trigger a single audit.

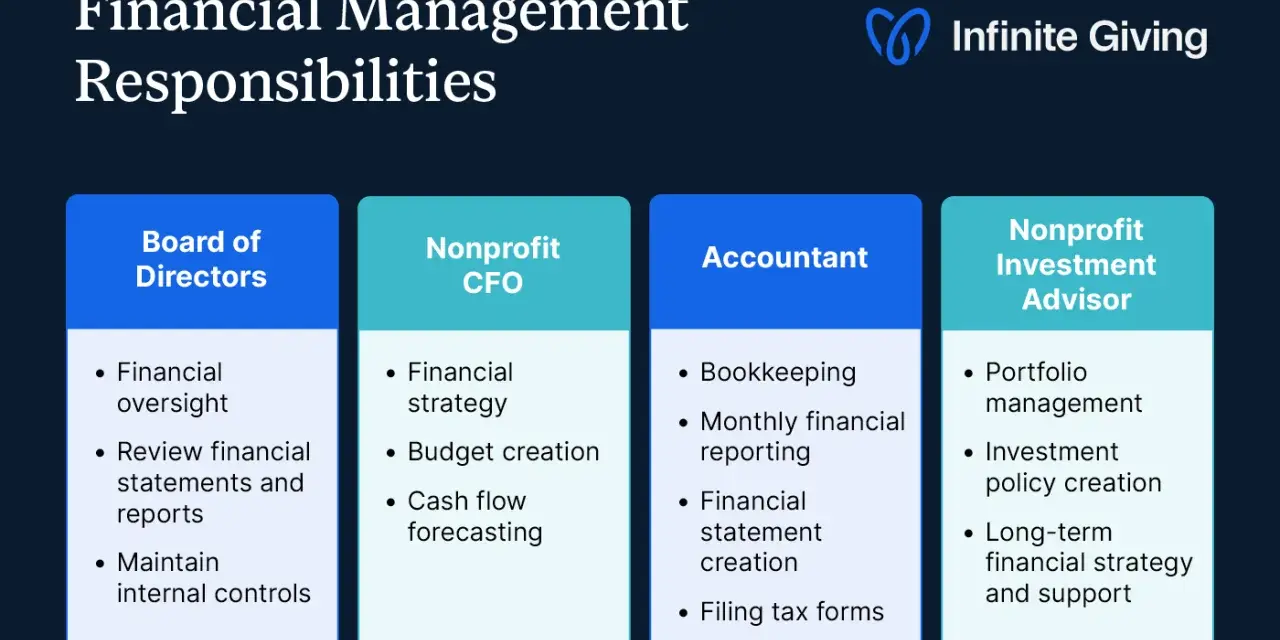

How I define strong financial management in a nonprofit

In my view, a charity runs well when money decisions answer three questions at once: can we pay the bills, are we spending donor funds the way they were intended, and do we have evidence to prove it? That is the real job behind nonprofit finance: stewardship, liquidity, and accountability. Bookkeeping records what happened; financial management decides whether the organization can keep doing mission-critical work without creating a hidden deficit.I also separate nonprofit finances into three layers. The first is transaction accuracy, meaning the books match reality. The second is operating discipline, meaning spending, hiring, and contracting follow a budget and approval process. The third is strategy, meaning leadership understands which revenue streams are dependable and which ones create risk.

If one of those layers is weak, the others start to wobble. That is why I look at cash flow next, because a budget that looks healthy on paper can still miss payroll.

The monthly cash flow rhythm that keeps bills paid

Budgets tell you what should happen over a year. Cash flow tells you whether money will be in the account when rent, payroll, grant matching, and vendor invoices arrive. A cash flow forecast is the schedule of cash coming in and cash going out, usually built by week or month. That distinction sounds basic, but it is where many charities get squeezed, especially when reimbursements arrive late or a grant is back-loaded.

| Report | What it answers | How often I want it |

|---|---|---|

| Budget vs. actual | Are we spending and earning as planned? | Monthly |

| Cash flow forecast | Will we have enough cash to pay bills on time? | Monthly, or weekly when cash is tight |

| Balance sheet | What do we own, owe, and hold in net assets at a point in time? | Monthly |

When I build a forecast, I map payroll, rent, loan payments, insurance, grant receipts, and large contract invoices across the next 12 months. If the organization depends on cost reimbursement, I also model the lag, because a 30- to 60-day delay can be the difference between healthy operations and a credit line draw. That is why cash management deserves its own cadence, not just a place inside the annual budget process.

Once cash timing is under control, the next risk is usually not math but process. That is where internal controls come in.

Internal controls that stop small errors from becoming expensive problems

Internal controls are the guardrails that keep money from being misused, lost, or quietly misrecorded. I do not think of them as red tape. I think of them as the minimum structure that lets staff move quickly without putting the organization at risk.

- Segregation of duties means the person who approves a payment should not also be the only person who enters and releases it.

- Monthly reconciliations mean bank and credit card statements are checked against the ledger every month, not whenever someone has time.

- Two-step approval keeps one person from controlling an expense from request to payment.

- Restricted access means only the right people can open accounts, move money, or change vendor details.

- Documented reimbursements create a paper trail for travel, mileage, supplies, and staff expenses.

- Exception review forces leadership to look at unusual transactions instead of trusting the monthly totals blindly.

Small nonprofits sometimes assume strong controls require a large finance team. They do not. A lean organization can still separate approval from payment, require board review above a dollar threshold, and keep a clean audit trail. I would rather see a simple control design that is actually followed than a complicated one that collapses after three busy weeks.

Controls protect the money; reserve policy tells you how much breathing room you actually have. That leads into the part many boards under-discuss.

How donor restrictions and reserves should work together

Restricted funds and reserves solve different problems, and confusing them is one of the fastest ways to create bad decisions. Under current nonprofit accounting, amounts are usually reported as net assets with donor restrictions or without donor restrictions. Net assets are the nonprofit version of equity, split by whether donor restrictions apply. A restricted grant or contribution may only be used for a program, time period, or purpose that the donor approved. That money is not general-purpose operating cash just because it sits in the bank.Board-designated reserves are different. They are usually unrestricted funds that the board has set aside for a specific internal purpose, such as emergencies, facility repairs, or a temporary revenue drop. I like reserves because they create optionality: they let management respond to delays, churn, or a surprise expense without distorting program spending.

| Reserve type | Typical use | Why it matters |

|---|---|---|

| Operating reserve | Short-term cash gaps, delayed grants, leadership transitions | Keeps services stable |

| Facilities reserve | Repairs, replacement, capital maintenance | Prevents deferred maintenance |

| Board-designated strategic reserve | New opportunities or planned transformation | Gives the board flexibility |

For most organizations, I treat three months of operating expenses as a practical floor and six months as a stronger cushion when revenue is volatile or reimbursements are slow. That is not a universal rule, but it is a realistic benchmark. The point is not to hoard cash; the point is to stop a temporary disruption from forcing bad long-term decisions.

Reserves only help if the board can see the numbers clearly and act on them, which is why reporting cadence matters so much.

What the board should review and how often

The board does not need to manage every invoice, but it does need enough financial literacy to exercise real oversight. The National Council of Nonprofits is right to frame financial policies as the way to clarify roles, authority, and approval steps. In practice, that means the board should know who can spend, who can sign, who can move cash, and what gets escalated before it becomes a problem.

| Frequency | What I want the board or finance committee to review |

|---|---|

| Monthly | Budget-to-actuals, cash position, unpaid bills, restricted balances, and major variances |

| Quarterly | Forecast updates, revenue concentration, reserve levels, and grant compliance issues |

| Annually | Budget approval, audit or review results, executive compensation, and policy refresh |

Budget-to-actuals is the comparison between what was planned and what actually happened. The best board questions are usually simple: Are we on track, what changed, and what decision is needed now? I also want directors to notice the shape of the revenue base. If one donor, one government contract, or one event supplies too much of the budget, the finance conversation is really a risk conversation in disguise. Revenue concentration means too much income comes from one source, and that can become fragile very quickly.

That kind of oversight works best when it is tied to filings and deadlines, not just board packets. The compliance side is where even well-run nonprofits can get careless.

Compliance checkpoints that matter in the U.S.

Nonprofit compliance is not just a tax issue; it is part of financial credibility. According to the IRS, most organizations must file an annual Form 990-series return, and the form depends on size. As of 2026, organizations with normally $50,000 or less in gross receipts generally file Form 990-N, those with under $200,000 in gross receipts and under $500,000 in assets can generally use Form 990-EZ, and larger organizations generally file the full Form 990.

| Situation | Practical rule |

|---|---|

| Gross receipts normally $50,000 or less | File Form 990-N unless another rule applies |

| Gross receipts under $200,000 and assets under $500,000 | Form 990-EZ is generally available |

| Above those thresholds | Form 990 is generally required |

| Federal awards of $1 million or more in a fiscal year | A single audit, which combines financial statement and federal compliance review, is required under federal audit rules |

| Public inspection | Annual returns must be available for public inspection for three years |

I also keep two practical reminders in mind. First, most 990-series returns are filed electronically now, so the process needs to be planned, not improvised. Second, audit requirements can come from state law, funder agreements, or federal grants, so a nonprofit should never assume that IRS filing rules are the whole compliance picture.

Once those deadlines are mapped, the recurring mistakes become easier to spot. And in my experience, the mistakes are usually more boring than dramatic.

The mistakes that quietly damage nonprofit finances

The biggest finance problems I see rarely start with fraud. They start with habits that seemed harmless. A charity can survive one sloppy month; it usually cannot survive a year of sloppy assumptions.

- Using the annual budget as if it were a live forecast. Fix it by updating projections every month.

- Mixing restricted and unrestricted cash mentally. Fix it with a separate ledger view and clear donor-condition tracking.

- Waiting until year-end to reconcile. Fix it with monthly closes and exception review.

- Approving expenses without a threshold. Fix it with a written approval matrix, a table that shows who can approve which dollar amounts.

- Ignoring full cost. Fix it by pricing programs with indirect costs, the shared overhead needed to run the organization, included.

- Letting one funding source dominate. Fix it by watching concentration risk and building reserves before you need them.

I would rather see a boring monthly close than a dramatic year-end scramble. Clean process looks unglamorous, but it is what keeps the mission from being interrupted by avoidable financial shocks.

That is also the logic I would use if I were starting a finance system from zero, because the first version should be simple enough to survive real life.

If I were setting this up from scratch

If I were building a nonprofit finance function from day one, I would focus on four things before adding anything fancy: a monthly close, a rolling cash forecast, written approval rules, and a board packet that directors can actually read. A monthly close is the routine of locking the books, reconciling accounts, and producing reports each month. Those four pieces solve most of the practical problems that show up in small and mid-sized charities.

- Set one chart of accounts, the account structure behind the ledger, so program, management, fundraising, restricted funds, and reserve activity are separated cleanly.

- Build a 12-month cash forecast and update it on a fixed schedule.

- Write financial policies for approvals, reimbursements, credit cards, grants, reserves, and document retention.

- Give the board a short reporting pack with budget-to-actuals, cash runway, key risks, and any compliance deadlines.

When those basics are stable, everything else becomes easier: fundraising decisions are clearer, board conversations are sharper, and the organization has a better chance of staying mission-focused even when revenue is uneven.