Debit card processing looks cheap until you run the numbers at scale. The Durbin Amendment changed that economics by capping interchange on many debit transactions and by giving merchants more routing choice, which is why it still matters to pricing, margins, and payment strategy in U.S. business finance. I’m going to break down how the rule works, who it covers, where the costs really show up, and what a finance team should watch in 2026.

The short version for business readers

- The rule mainly affects debit interchange, not every part of card processing.

- The current framework still uses a $0.21 base, 0.05% of the transaction value, and a possible $0.01 fraud-prevention adjustment for covered issuers.

- Banks with less than $10 billion in assets are generally exempt from the fee cap, but routing rules still matter.

- Merchants may save on swipe fees, but the all-in benefit depends on processor markups, card mix, and online routing.

- In 2026, the smartest move is to budget with scenarios, not with a single static fee assumption.

What the amendment actually changed

At its core, the rule turned debit interchange from a mostly network-driven price into a regulated one for large issuers. Interchange is the fee a merchant’s bank pays to the cardholder’s bank for completing the transaction, and that fee is usually embedded in the merchant’s total acceptance cost. The policy also added a routing element: issuers have to support more than one unaffiliated network, so merchants are not locked into a single path for every debit transaction.

That combination matters because it changes two things at once: the size of the fee and the leverage around how the transaction is routed. In practice, I think that is the real story businesses miss. People focus on the cap, but the routing side can decide whether a merchant actually captures the savings. That leads directly to the question of how the cap works today.

How the current fee cap works in practice

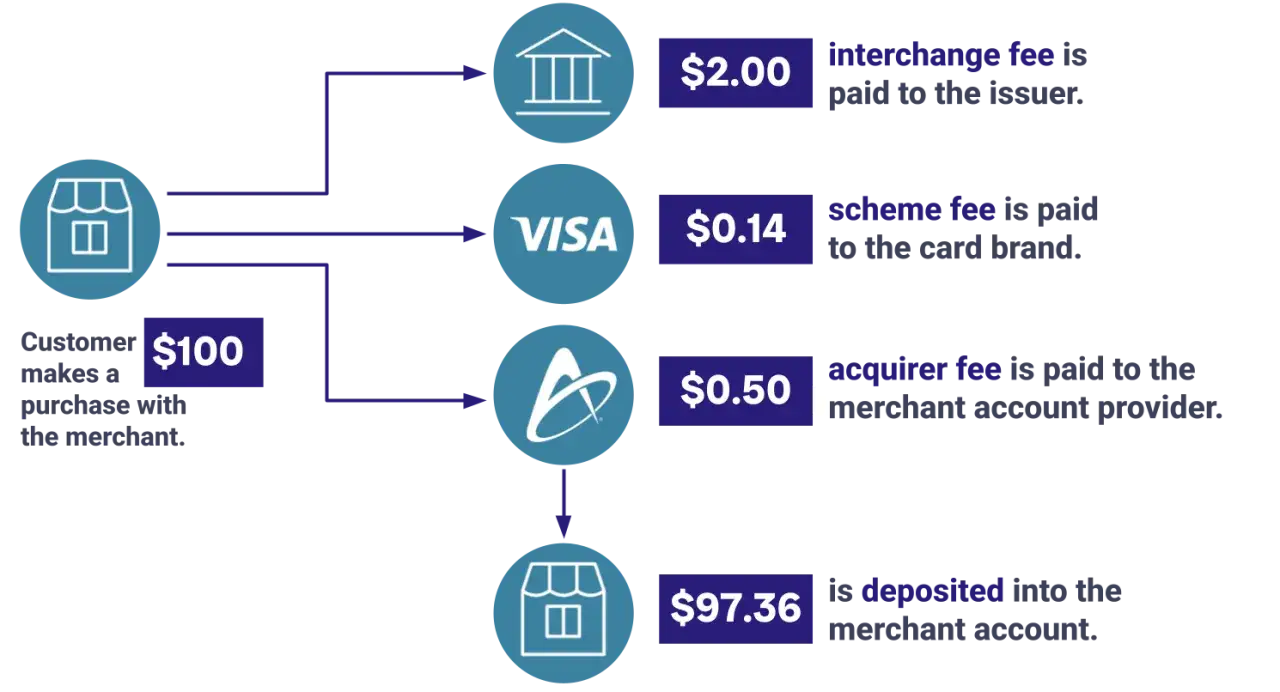

As of 2026, covered issuers generally cannot receive more than $0.21 plus 0.05 percent of the transaction value, plus a possible $0.01 fraud-prevention adjustment if they qualify. The result is not the same on every ticket size, which is why the rule matters more on higher-volume payment flows than on one-off transactions.

| Rule element | What it means | Business takeaway |

|---|---|---|

| Base component | $0.21 per covered debit transaction | Sets the floor for the interchange cap calculation |

| Ad valorem component | 0.05% of the transaction amount | Raises the fee slightly as ticket size increases |

| Fraud-prevention adjustment | $0.01 if the issuer meets the rule’s requirements | Security compliance can preserve a small amount of revenue |

| Covered issuer threshold | Generally issuers at or above $10 billion in assets | Big banks feel the cap most directly |

On a $50 debit transaction, that formula produces a maximum interchange of 24.5 cents if the fraud-prevention adjustment applies. That is still only one part of the merchant’s total payment cost, but it is the part most directly shaped by the federal rule. The next issue is who is actually in and who is out.

Which transactions are covered and which are not

The easiest mistake is to assume every debit card payment is treated the same way. It is not. The statutory threshold is asset-based, and some card types sit outside the fee cap even when they run on debit rails.

| Category | Typical treatment | Why it matters |

|---|---|---|

| Large issuers | Subject to the interchange cap | These are the institutions whose economics changed most |

| Small issuers | Generally exempt from the fee cap | Community banks and many credit unions keep more pricing flexibility |

| Government-administered payment cards | Often exempt | Not every public-benefit or government-card transaction is capped |

| Reloadable general-use prepaid cards | Often exempt | High-volume prepaid programs may not follow the same pricing logic as bank debit |

The practical lesson is simple: do not model debit costs as one blended rate unless your data are actually blended that way. Split covered debit, exempt debit, and prepaid flows before you forecast the impact. Once you do that, the differences between merchants, banks, and consumers become much easier to see.

Why merchants and banks experience it differently

Merchants usually want lower acceptance costs. Banks, especially large debit issuers, usually see a revenue hit first. Consumers can end up somewhere in the middle because the savings do not always disappear cleanly into lower prices; sometimes they show up as different account fees, different rewards, or changes in product design.

| Stakeholder | Likely effect | What to watch in business finance |

|---|---|---|

| Merchants | Lower interchange on covered debit sales | Check whether processor markups erase part of the saving |

| Large banks and issuers | Less debit interchange revenue | Expect pressure on deposit pricing, rewards, or fee structures |

| Small issuers | Fee cap exemption, but still exposed to routing rules | Competitive pressure can spill over from larger institutions |

| Consumers | Possible price benefits, but not always visible | Watch for side effects in checking account pricing and rewards |

This is why the rule often produces second-order effects. A merchant may save on swipe fees, but a bank may respond by changing account economics. That response is not automatic, and it is not identical across institutions, which is why the real-world outcome depends on market structure rather than on the statute alone.

How finance teams should use the rule in budgeting and negotiations

I would treat the debit-fee framework as a forecasting input, not a headline talking point. If you run a merchant business, the right question is not “What is the cap?” It is “What portion of my debit volume is actually affected, and how much of that savings survives the processor contract?”

- Separate card-present and card-not-present debit volume in your reporting.

- Compare interchange, processor markup, gateway fees, and fraud tools as one bundle.

- Ask your acquirer how routing affects e-commerce and mobile debit costs.

- Rebid payment contracts if debit volume is large enough to move gross margin by meaningful basis points.

- Model both a stable-fee case and a lower-fee case so you are not surprised by policy changes.

If you are on the issuer side, the task is different. Review whether fee income, account fees, rewards, and fraud controls are balanced in a way that still supports your deposit strategy. The rule does not eliminate debit profitability, but it does make reliance on interchange a weaker long-term plan. That is why the policy debate in 2026 still matters.

Why this debit-fee rule still matters in 2026

The Federal Reserve proposed in 2023 to revise the cap methodology. In that proposal, the base component would have fallen from 21.0 cents to 14.4 cents, the ad valorem component from 5.0 basis points to 4.0 basis points, and the fraud-prevention adjustment would have risen from 1.0 cent to 1.3 cents. I treat that as a warning sign, not as a completed change: if your model assumes a static fee structure, it is already behind the policy curve.

For planning purposes, I would stress-test three things now: the current cap, a lower-cap scenario, and the possibility that routing rules become more important in online payments. That is the kind of scenario analysis that protects margins without overreacting to every policy headline. It also keeps finance teams focused on what actually changes cash flow.

What I would take away before building a pricing model

The clearest lesson is that this rule is not just about fees. It is about who has bargaining power in the payment chain, how routing affects that power, and how much of the cost actually reaches your income statement. If your business depends on debit-heavy sales, small changes in interchange can move gross margin more than people expect.

If I were reviewing a merchant or issuer model today, I would start with actual transaction data, not industry averages. That is the fastest way to see whether the payment mix, the network path, and the fee cap are helping or hurting you in practice. From there, the numbers usually tell a more useful story than the policy debate does.