Impairment accounting is the part of U.S. GAAP that forces management to stop carrying an asset at an amount the economics no longer support. I usually treat it as a valuation and governance question first, and an entry second: identify the right unit of account, test whether the asset is still recoverable, and measure any write-down with assumptions that can survive review. That mix is what makes the topic important for finance teams, boards, and anyone reading a balance sheet with a skeptical eye.

Key takeaways on asset write-downs under U.S. GAAP

- Not every decline in value becomes an impairment; the result depends on the asset class and the specific U.S. GAAP model.

- For long-lived assets, the first question is recoverability, and that screen uses undiscounted future cash flows.

- Goodwill is tested at least annually at the reporting-unit level, while indefinite-lived intangibles can use a qualitative screen first.

- Financial assets follow the CECL model, which is an allowance for expected credit losses rather than a classic asset write-down.

- Most impairment losses under the traditional U.S. GAAP models are not reversed later, so the initial conclusion matters.

- Strong documentation, assumption support, and review discipline are as important as the calculation itself.

What impairment means in practice

At its core, the issue is simple. If the carrying amount of an asset is higher than the economic benefit the business can still recover, the balance sheet is overstated and the excess has to come off. Under U.S. GAAP, that does not mean every decline in market sentiment becomes an impairment. It means the decline has to be tied to the specific test for that asset class.

I like to think of impairment as a reset to a supportable number, not a punishment for bad quarters. The charge reduces assets and equity immediately, and it can affect debt covenants, bonus plans, sale negotiations, and investor confidence. In other words, the accounting may be non-cash, but the consequences usually are not.

Once that basic idea is clear, the next question is when the test must actually be run.

When U.S. GAAP expects a test

The timing depends on the asset. U.S. GAAP does not use one universal trigger for everything, and that is where a lot of teams go wrong.

Long-lived assets held and used

For a long-lived asset held and used, I look for events or changes in circumstances that suggest the carrying amount may not be recoverable. Think sustained operating losses, lower demand, plant closure plans, adverse regulation, or obvious obsolescence. The test is performed at the asset-group level, meaning the smallest group of assets that generates largely independent cash flows.

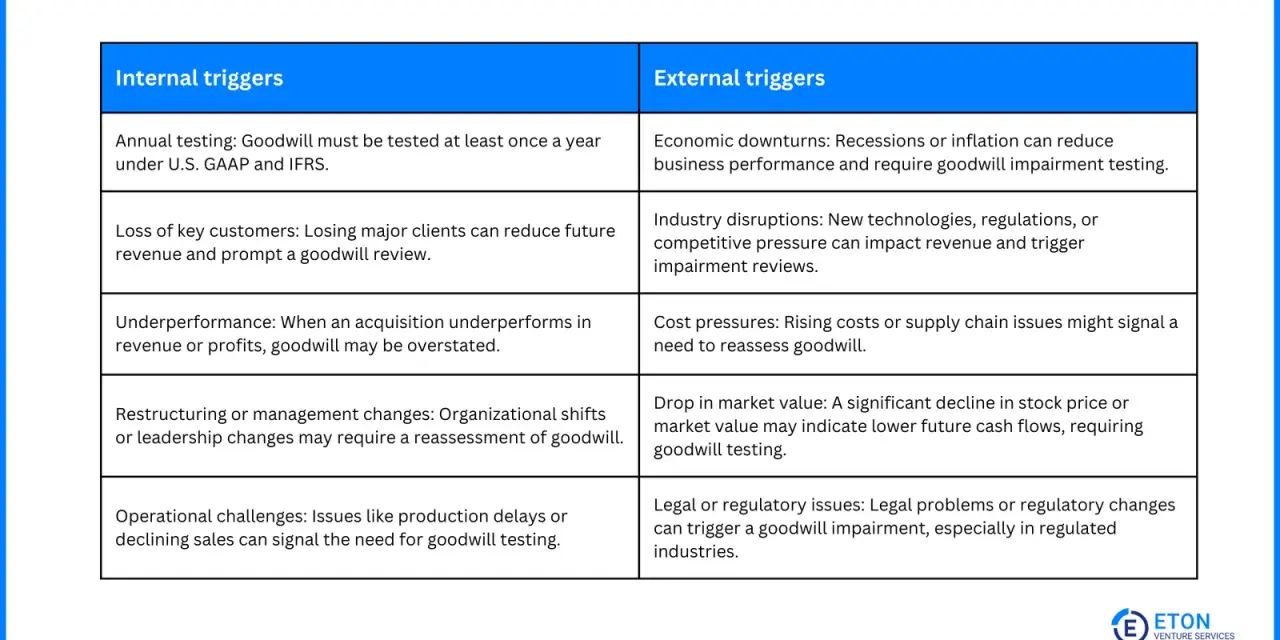

Goodwill and indefinite-lived intangibles

Goodwill is different. It is tested at least annually at the reporting-unit level, and more often if triggering events show up. Indefinite-lived intangibles follow a similar calendar discipline, although U.S. GAAP allows a qualitative screen first. If the qualitative review suggests it is not more likely than not that the asset is impaired, the company can skip the quantitative fair value test. That threshold is more than a 50 percent likelihood.

Read Also: Accounting Internal Controls - Your Guide to Stronger Finance

Financial assets and held-for-sale groups

I also separate financial assets from classic fixed-asset impairment. Amortized-cost instruments fall under the current expected credit loss model, or CECL, which recognizes expected losses rather than waiting for a traditional impairment trigger. Once a long-lived asset or disposal group is classified as held for sale, the measurement shifts again, usually to the lower of carrying amount or fair value less cost to sell.

That timing map matters because the wrong trigger test usually produces the wrong answer, even when the valuation work itself is solid.

How measurement differs across asset classes

This is where the mechanics diverge. I include credit losses here because many finance teams loosely call them impairment, even though CECL is an allowance model rather than a direct asset write-down.

| Asset class | Typical trigger or timing | How the test works | Can the loss reverse? |

|---|---|---|---|

| Long-lived assets held and used | When events or changes in circumstances suggest the carrying amount may not be recoverable | Compare undiscounted future cash flows with carrying amount; if the asset group fails recoverability, write it down to fair value | Generally no |

| Goodwill | At least annually and when triggering events occur | Compare reporting-unit fair value with carrying amount; recognize the shortfall up to the goodwill balance | No |

| Indefinite-lived intangible assets | At least annually; a qualitative screen may be used first | If the qualitative screen is not enough, compare fair value with carrying amount | No |

| Financial assets at amortized cost | Each reporting date under CECL | Record an allowance for expected credit losses based on current conditions and reasonable forecasts | The allowance can move up or down as estimates change |

| Held-for-sale disposal groups | When classified as held for sale | Measure at the lower of carrying amount or fair value less cost to sell | Value changes are updated until sale |

The key contrast is the long-lived asset recoverability screen. Under ASC 360, I first compare undiscounted future cash flows with carrying amount. If those cash flows cover the book value, the process stops, even if fair value has softened. If they do not, the impairment loss equals the excess of carrying amount over fair value. So if a plant carries $12.0 million, has undiscounted cash flows of $10.4 million, and fair value of $9.2 million, the write-down is $2.8 million.

Goodwill is more direct after the 2017 simplification: compare reporting-unit fair value with carrying amount, and recognize the shortfall up to the amount of goodwill. There is no second step that tries to rebuild the implied fair value of goodwill itself.

That difference sounds technical, but in practice it changes the size of the loss, the speed of the test, and the amount of judgment a valuation specialist has to support.

What the journal entry and P&L impact usually look like

The entry itself is usually straightforward, but the financial statement effect is broader than the journal line. For a held-and-used asset, the entry is typically debit impairment loss and credit the asset or accumulated impairment loss. For goodwill, the loss reduces goodwill directly. For CECL, the company records credit loss expense and a related allowance. Those are different mechanics, and the credit agreement or disclosure note should reflect the difference rather than blur it.

- Long-lived asset: Debit impairment loss, credit the asset or accumulated impairment loss.

- Goodwill: Debit goodwill impairment loss, credit goodwill directly.

- CECL asset: Debit credit loss expense, credit allowance for credit losses.

- Held for sale: Debit loss on measurement, credit the disposal group down to fair value less cost to sell.

On the income statement, the charge may land in operating income or in a separate impairment line depending on the asset and presentation policy. On the balance sheet, equity falls immediately. For tax, the book charge and the tax deduction often do not move in lockstep, so the deferred tax effect deserves attention before the close is finalized. I also watch debt covenants closely: calling a loss "non-cash" does not make it invisible if the covenant starts from net income, equity, or tangible net worth.

Once the entry is clear, the next risk is not the math - it is the mistakes people make while assembling it.

Common mistakes that make a file fail review

- Using the wrong unit of account: A single machine, a whole plant, and a reporting unit do not always get tested the same way.

- Mixing up the recoverability test: For held-and-used assets, discounted cash flows are not the screen; undiscounted cash flows are.

- Letting stale forecasts drive the answer: If the trigger happened in Q2, but the model still reflects Q1 optimism, the file already looks weak.

- Treating the qualitative screen as a shortcut: A qualitative conclusion is still a conclusion and needs a documented logic trail.

- Assuming losses reverse later: That is usually not true for the classic U.S. GAAP impairment models.

- Ignoring covenant and disclosure effects: A charge that looks small in isolation can still matter a lot in financing or a sale process.

Most of these errors are not valuation failures. They are process failures, which is why the control environment matters as much as the accounting memo.

Controls and governance that make the conclusion defensible

I want to see three things in a serious impairment file: a clean story about what changed, support for the assumptions, and a review trail that shows the numbers were challenged rather than accepted on trust. If management uses a qualitative assessment, the memo has to explain why the trigger risk stayed below the more-likely-than-not threshold. If management uses a quantitative model, I expect sensitivity analysis on the assumptions that can move the answer fastest, usually revenue growth, margins, discount rate, or terminal value.

For larger or public companies, this is also a governance issue. The board or audit committee does not need to build the model, but it should understand what drove the conclusion, which assumptions are most fragile, and whether a single bad quarter could turn into a material charge. When I see a major judgment with no documented challenge process, I assume the eventual audit conversation will be expensive.

The cleaner the governance trail, the easier it is to close the books without re-opening the entire story later.

What I would keep ready before year-end closes

If I were building the year-end file from scratch, I would keep a small package ready before anyone asks for it.

- A trigger log with dates, facts, and the business event that started the review.

- An asset-group or reporting-unit map that shows exactly what was tested.

- Forecasts used in the test, plus the prior version for comparison.

- A valuation memo that explains the method, the assumptions, and why the model is reasonable.

- Sensitivity analysis showing what would change the conclusion.

- Approval notes from finance, FP&A, and, when needed, the audit committee.

- Draft disclosure language if the charge is material or if the assessment was qualitative.

That package does more than support the number. It shows that the decision was made deliberately, on the right asset base, with the right model, and with enough discipline to stand up in audit, financing, or transaction diligence. Once you treat impairment accounting as a valuation and controls problem instead of a late-stage closing adjustment, the entire process becomes easier to defend.