ACV and ARR look similar on a dashboard, but they answer different questions. I use ACV to judge the value of a single deal on an annualized basis, and ARR to judge the strength of the recurring revenue engine as a whole. If you are pricing contracts, forecasting growth, or building a board-ready finance pack, getting that distinction right matters more than most teams admit.

The short version for finance teams

- ACV measures one contract or account on an annualized basis.

- ARR measures total recurring revenue across the business.

- ACV is better for deal quality, segment analysis, and sales motion.

- ARR is better for forecasting, valuation, and leadership reporting.

- One-time fees, implementation charges, and discounts should be handled separately from recurring revenue.

- The cleanest reporting comes from defining both metrics in writing and using the same logic every month.

ACV and ARR measure different layers of the same business

The easiest way to think about ACV vs ARR is to separate the deal view from the company view. ACV asks how much annualized value one customer contract contributes. ARR asks how much recurring revenue the whole business can reasonably expect over the next 12 months from its active subscription base.

That distinction sounds small, but it changes how I read the numbers. A high ACV can come from a few large enterprise contracts, while a strong ARR can be built from many smaller accounts. Those two businesses can look very different operationally, even if the top-line revenue is similar.

| Metric | What it measures | Best for | Main risk if misused |

|---|---|---|---|

| ACV | The annualized value of a single customer contract | Deal sizing, pricing, segmentation, sales performance | Inflating value by mixing in one-time fees or non-recurring items |

| ARR | Total recurring revenue across all active customers | Forecasting, valuation, budgeting, board reporting | Overstating stability by including revenue that is not truly recurring |

If I had to compress it into one sentence, I would say this: ACV tells me how good the deal is, while ARR tells me how healthy the business is. That difference becomes much clearer once you look at the formulas.

How I calculate each metric without distorting the story

Most confusion comes from mixing recurring revenue with everything else attached to the contract. I avoid that by separating the contract economics from the revenue metrics.

ACV on a single contract

For a three-year contract worth $48,000 in recurring fees plus a $6,000 implementation charge, I would treat the clean ACV as $16,000. The recurring portion is annualized across the contract term, but the implementation fee stays outside the recurring value because it does not repeat every year. If the goal is to understand total contract economics, that $54,000 figure belongs in TCV, not ACV.

That matters because two contracts with the same ACV can still have very different cash profiles. One may be prepaid annually, another may be billed monthly, and a third may include setup work that should not be blended into recurring value. If I blur those lines, the number stops being useful for comparison.

ARR across the business

ARR is broader and more operational. If a company has 120 customers paying $600 per month, the MRR is $72,000 and the ARR is $864,000. If expansion revenue adds $96,000 over the year and churn removes $60,000, ending ARR rises to $900,000. The point is not the exact formula in every billing system; the point is that ARR reflects the total recurring base after growth, contraction, and churn are accounted for.

In practice, I want ARR to stay clean enough that leadership can use it for planning. That means recurring only, consistently annualized, and reconciled against billing and revenue recognition data. Once you get that discipline right, the next question is not “what does the metric mean?” but “when should it drive the decision?”

Read Also: Startup Stock Options - Is Your Equity Real Value?

Edge cases worth defining in writing

- Usage-based add-ons: Include them only if they are truly recurring and predictable enough to annualize without guessing.

- Implementation or onboarding fees: Keep them out of ARR and usually out of ACV if you want comparable deal quality.

- Discounts and free months: Decide whether you annualize the effective price or the list price, then apply it consistently.

- Ramp deals: If pricing changes over time, document whether ACV reflects the average annualized value or the current-year value.

- Partial-year contracts: Normalize them carefully so a short initial term does not fake a stronger or weaker number.

I treat those edge cases as governance issues, not spreadsheet trivia. If two teams calculate the same metric differently, the board is not getting a clean signal. From there, the real question becomes which metric deserves priority in a given decision.

When ACV gives better signal than ARR

ACV is the sharper metric when I care about deal quality. It tells me whether the sales team is winning larger contracts, whether a pricing change is actually working, and whether a segment is worth the cost of serving it.

- Enterprise sales: If deals are large, complex, and relationship-driven, ACV shows whether the motion is paying off.

- Segmentation: If you are moving from SMB to mid-market or enterprise, rising ACV is evidence that the shift is real.

- Pricing tests: A higher ACV after a packaging change can validate the new offer, but only if churn does not worsen at the same time.

- Sales compensation: ACV is useful when commissions or quotas should reward contract value rather than raw volume.

Here is the practical catch: a strong ACV does not automatically mean a strong business. Ten $40,000 deals create the same ARR as two hundred $2,000 deals, but the operating model behind those two revenue engines is very different. That is why I never let ACV replace ARR; I use it to explain where ARR is coming from.

When ARR should lead the conversation

ARR is the number I put in front of leadership when the question is company health, not deal quality. It is the clearest way to show how much recurring revenue the business actually controls and whether the revenue base is expanding, flat, or contracting.

That makes ARR especially useful for budgeting, hiring, runway planning, and valuation conversations. It also tells me how much confidence I should place in future periods, because recurring revenue is more dependable than one-off inflows.

| Pattern | What it usually means | What I check next |

|---|---|---|

| High ACV, low ARR | A small number of large contracts or an early-stage enterprise motion | Pipeline depth, concentration risk, sales cycle length |

| Low ACV, high ARR | A broad base of smaller customers or very strong retention | CAC efficiency, support load, net revenue retention |

| ACV rising, ARR flat | Deal size is improving, but the base is not compounding fast enough | Win rate, churn, expansion, volume of closed deals |

| ARR rising, ACV flat | The business is scaling through volume or retention, not larger contracts | Segment mix, upsell motion, margin quality |

This is where I see a lot of teams overread the wrong metric. A company can celebrate rising ACV while ARR stays stubbornly flat, and that usually means the sales motion is getting more expensive without fully compounding the base. ARR is the better anchor when you want the whole business picture. Once that is clear, the remaining risk is confusing the numbers with similar metrics that are not the same thing.

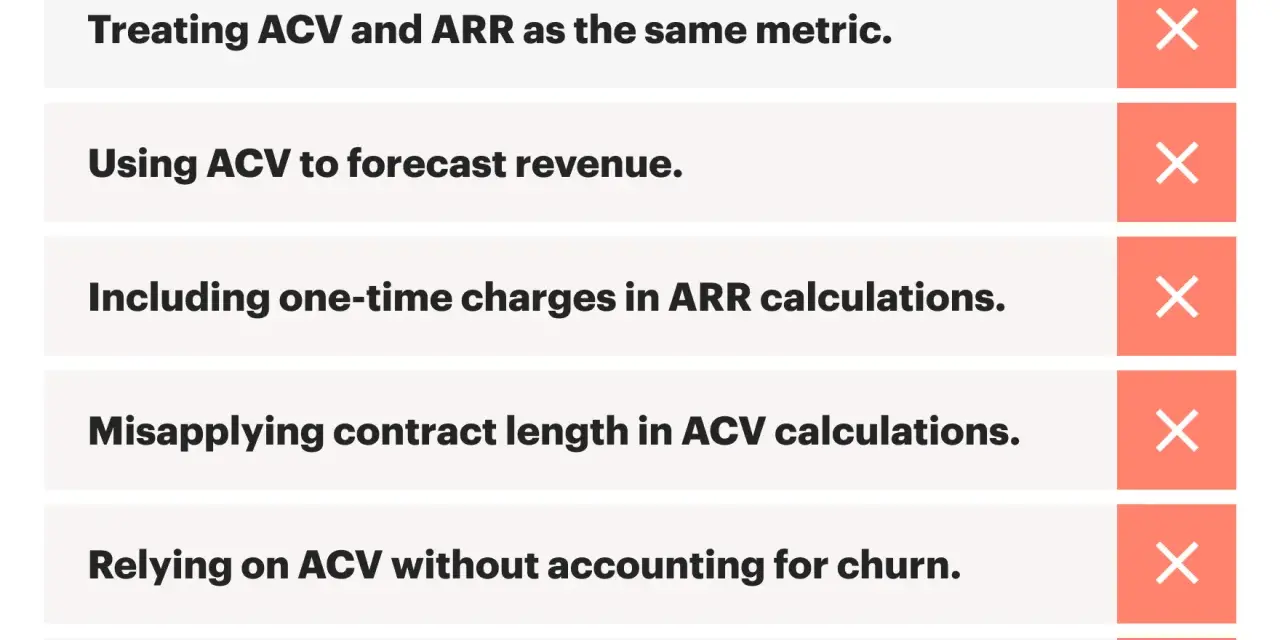

Where teams get the comparison wrong

Most bad reporting around these metrics does not come from bad math. It comes from inconsistent definitions. If I am reviewing a finance pack, these are the mistakes I look for first:

- Counting implementation fees, onboarding charges, or consulting work as recurring revenue.

- Mixing bookings, billings, and recognized revenue as if they were the same number.

- Comparing ACV across customer segments without accounting for contract term length.

- Using ARR pulled from billing data without checking renewals, downgrades, credits, or timing differences.

- Changing the formula quarter to quarter and then pretending the trend is stable.

The fix is simple, but not easy: write the definitions down and keep them stable. I want one version of ACV, one version of ARR, and one owner for how each number is maintained. That discipline turns the metrics from marketing language into something the business can actually trust.

How I use both metrics in a board pack

In a board pack, I would not force ACV and ARR to compete. I would let them do different jobs. ARR belongs in the headline section because it shows the size and momentum of the recurring base. ACV belongs in the supporting analysis because it explains whether growth is coming from bigger deals, a different customer mix, or a more effective pricing model.

- Lead with ARR as the top-line recurring revenue metric.

- Break ACV down by segment so the board can see which customer bands are working.

- Show churn, expansion, and net retention alongside ARR so the movement is not misread.

- Explain one-time fees separately so no one mistakes them for recurring strength.

If I had to choose one rule, it would be this: use ACV to explain the quality of growth and ARR to prove the existence of growth. That approach keeps the story honest and makes the next review easier to defend.

What I verify before I trust either number

Before I put either metric in a memo, a forecast, or a board deck, I check a short list of controls. If any of these are unclear, the number may still be directionally useful, but it is not ready for serious decisions.

- Are recurring and non-recurring items separated cleanly?

- Are annualized values calculated the same way across all segments?

- Are discounts, ramp terms, and free periods handled consistently?

- Are usage-based charges included only when they are stable enough to defend?

- Does the metric match what finance, sales, and leadership all believe it means?

When those answers line up, the comparison between ACV and ARR becomes genuinely useful. ACV tells me where deal quality is moving, ARR tells me whether the revenue engine is compounding, and together they give me a much more reliable view of the business than either number can provide on its own.