Card processing costs can eat into margin faster than many owners expect, especially on small tickets and high-volume sales. The practical answer to can a business charge a credit card fee is yes in many U.S. situations, but only if the fee is structured as a permitted surcharge and disclosed correctly. The difference between a clean checkout policy and a compliance problem usually comes down to the payment type, the state, and how clearly the price is shown before the customer pays.

What matters before you add a card fee

- In many U.S. cases, a business can add a fee to credit card purchases, but the fee has to follow card-network rules and state law.

- Debit cards and prepaid cards are not treated the same way, and they should not be surcharged like credit cards.

- The fee is usually capped by the merchant’s actual cost of acceptance or the network’s ceiling, whichever is lower.

- Disclosure is not optional; customers should see the fee before checkout and on the receipt.

- Cash discounts and minimum purchase policies are separate tools, and sometimes they work better than a surcharge.

- Multi-state businesses need location-by-location compliance, not a single blanket rule.

The legal answer is yes, but only in specific conditions

I treat this as a conditional yes, not a blank check. A merchant can often pass some processing cost to the customer when the customer chooses to pay by credit card, but the fee has to sit inside a permitted framework. That framework usually starts with three questions: is it a credit card transaction, is the fee disclosed before payment, and does the state where the sale happens allow the practice?

The card type matters more than many owners realize. Credit cards are one category; debit cards and prepaid cards are another. Even if a terminal lets a customer press a button that says “credit,” that does not turn a debit card into a credit card for surcharge purposes. If your policy is loose here, the error shows up fast at the register and even faster in a dispute.

The other trap is the idea that any card fee can be hidden until the end. It cannot. Under U.S. fee-disclosure rules, a mandatory fee should be visible before the customer is committed, and it should appear clearly on the receipt. Once those basics are clear, the real work starts with the card-network cap.

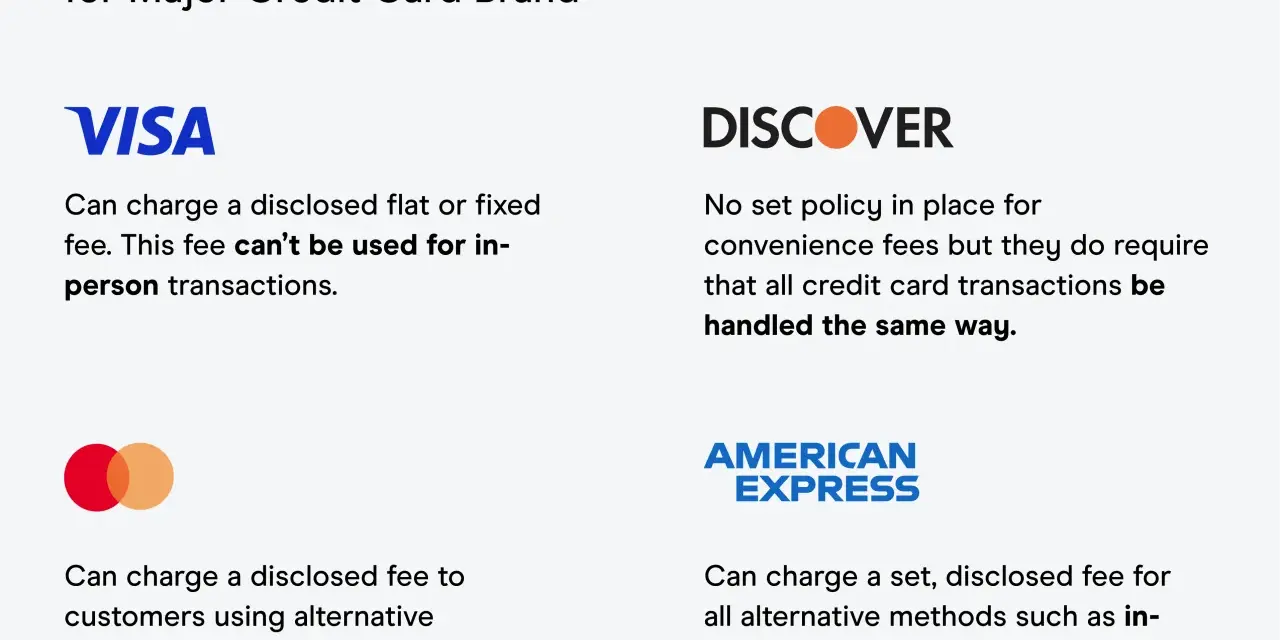

What the major card rules actually require

In practice, the major card rules are built around cost recovery, not profit. A merchant is generally trying to recover part of the merchant discount rate, which is the percentage-based cost of accepting a card through the processor. The fee should track actual acceptance cost, not whatever number feels convenient at checkout.

| Rule | What it means in practice |

|---|---|

| Credit cards only | Do not add the fee to debit or prepaid transactions. |

| Fee cap | The surcharge is capped by the merchant’s actual cost of acceptance or the network’s ceiling, whichever is lower. |

| Disclosure | Tell the customer before checkout and show the surcharge as a separate line item on the receipt. |

| Lead time | Plan for advance notice before switching the fee on. |

| Brand consistency | Apply the policy consistently within the rules of the network and the card type. |

The practical caps are not the same everywhere. One major network limits U.S. credit-card surcharges to the lower of the merchant discount rate or 3 percent. Another allows brand-level surcharges up to the lower of the merchant’s average effective discount rate or a 4 percent ceiling. That means a $100 sale with a 2.5 percent allowable surcharge can support a $2.50 fee, but a 4 percent cap does not let you exceed your actual cost if your real cost is lower.

There is also a simple operational point that gets overlooked: if the card fee is your workaround for small-ticket transactions, a minimum purchase amount may be a cleaner tool. The point is not to charge more wherever possible. The point is to choose the least messy option that still protects margin. Even then, local law can still override the playbook.

State law can be stricter than the network rules

This is where businesses get into trouble. A policy that works in one state may not work in the next one, and a multi-location merchant should never assume a uniform nationwide surcharge policy is safe. In New York, for example, businesses charging an extra fee for credit card purchases must show the highest total price before checkout or use a two-tiered pricing display that makes the card price and cash price clear. That is a transparency rule, not just a pricing rule.

I would read that requirement as a warning sign for any business that hides fees until the last screen or the final receipt. Even a modest percentage can become a problem if the customer does not see the total early enough to make an informed choice. Other states still have their own limits, bans, or disclosure requirements, so the legal answer is always tied to geography.

If you operate online and in physical stores, the issue gets even more specific. The same company can face different obligations depending on the merchant location, the checkout channel, and the type of payment. That is why the label you choose matters almost as much as the percentage itself.

Surcharge, cash discount, and minimum purchase are not the same thing

People often use these terms interchangeably, and that is a mistake. They solve different problems, create different customer reactions, and carry different compliance burdens. If I were designing a policy for a real business, I would separate them immediately instead of trying to force one policy to do the job of all three.

| Tool | How it works | Best fit | Main drawback |

|---|---|---|---|

| Surcharge | An extra amount is added because the customer pays with a credit card. | Direct cost recovery when the fee needs to be visible. | Can feel punitive and requires tight disclosure. |

| Cash discount | The posted price reflects the card price, and cash customers receive a lower price. | Businesses that want less checkout resistance. | Must be presented carefully so it is a real discount, not a disguised surcharge. |

| Minimum purchase | Customers must reach a small threshold before paying by credit card. | Very small transactions where processing cost is hard to absorb. | Can frustrate impulse buyers or small-ticket customers. |

A cash discount is often the easier story to tell. Customers usually accept “cash gets a lower price” more readily than “credit gets a penalty,” even when the math is similar. A convenience fee is a separate category again, and I would not treat it as a default substitute for a surcharge because the eligibility rules are narrower and more situation-specific.

Minimum purchase policies can also be useful, especially in businesses with tiny tickets where a card fee would consume too much margin. In the U.S., major card rules permit merchants to set a minimum credit-card transaction amount up to $10, but not on debit transactions. That makes it a practical, low-drama alternative when the economics are the real problem. The operating details matter, because customers only see the checkout moment.

How to roll out a fee without creating disputes

I usually recommend that businesses handle this like a mini compliance project, not a pricing tweak. The percentage is only one part of the decision. The rest is systems, language, and consistency.

- Calculate the real cost. Use your average effective merchant discount rate, not a guess or a round number from last quarter.

- Choose the right tool. Decide whether a surcharge, a cash discount, or a minimum purchase is the cleanest fit for your sales model.

- Update every customer touchpoint. Website pricing, checkout screens, point-of-entry signage, and receipts all need to tell the same story.

- Train staff on card types. Employees should know the difference between credit, debit, and prepaid cards before the policy goes live.

- Test the full checkout flow. Run an in-store transaction and an online transaction to confirm that the surcharge displays correctly and lands on the receipt as intended.

There is one rule I would not bend: if the fee is mandatory and there is no real no-fee payment alternative at the same location or platform, it belongs in the total price up front. Hiding it at the end is where businesses create the exact kind of customer complaint they were trying to avoid. If the policy is optional and clearly disclosed, the risk is much lower, but the disclosure still has to be clean.

I also like to check refund and dispute handling before launch. If a transaction is refunded, the surcharge treatment should be consistent, and staff should know how to answer customers who question the extra line item. That is the difference between a fee that runs smoothly and one that quietly generates chargebacks, emails, and front-desk conflict.

Once the mechanics are in place, the strategic question is whether the fee is worth the friction at all.

The cleanest default for 2026

For most businesses, my default is simple: do not add a credit card fee unless you have already checked the state rule, the network rule, and your checkout disclosure. If any one of those three pieces is weak, the policy is not ready. If all three line up, start with a modest, clearly disclosed setup and watch customer behavior before rolling it out broadly.

In many cases, a small price increase or a cash discount will do the same financial work with less customer resistance. That does not mean surcharging is wrong. It means surcharging should be a deliberate business decision, not an improvised response to rising processing costs. In practice, the safest businesses are the ones that can explain the fee clearly and defend it line by line.