Running a business on one checking account is simple until the transactions start to blur together. Separating operating cash, payroll, taxes, and project money can make the books easier to read, reduce avoidable errors, and support cleaner internal controls. Using multiple business checking accounts can be a smart move, but only if each account has a job and the system stays disciplined.

The essentials at a glance

- Extra accounts work best when they separate real cash flows such as payroll, taxes, or project funds.

- The IRS says separate business and personal accounts make records easier to keep, and that logic matters even more once you add more than one business account.

- The FDIC insures deposits up to $250,000 per depositor, per insured bank, per ownership category, so two accounts at the same bank do not automatically mean more coverage.

- Too many accounts can create fee drag, extra transfers, and a reconciliation burden that wipes out the benefit.

- A lean setup usually starts with one operating account, one reserve account, and one optional account for payroll or a distinct workflow.

Why separate checking accounts sharpen control

I treat separate accounts as a governance tool, not just a convenience. When revenue lands in one place and every dollar has a purpose, it becomes much easier to see whether the business is actually profitable or just busy. That separation also supports segregation of duties, which simply means no single person should control every step of a money flow when the business can avoid it.

The practical gain is clarity. I can glance at an operating account and know what is available for bills, while a tax reserve or payroll account signals money that should not be spent casually. That is especially useful in businesses with recurring payroll, irregular project income, or owners who need clean draws. The IRS says separate business and personal accounts make records easier to keep, and the same logic applies when a business needs more than one internal bucket.

The limit is just as important as the benefit. A second account only helps if it changes behavior, improves visibility, or reduces error. If it simply creates another login and another statement with no real purpose, it is administrative noise. That is why I always ask the next question: when does the extra account actually earn its place?

When an extra account is useful and when it is overkill

In practice, a second or third checking account makes the most sense when the business has distinct cash flows that should not be mixed. A payroll account, a tax reserve account, and a project-specific account are common examples. I also see value in separate accounts for businesses with multiple locations, multiple partners, or different revenue streams that need their own reporting line.

| Business pattern | Another account helps when | It is probably overkill when |

|---|---|---|

| Consulting or professional services | You want to isolate tax reserves, owner draws, or client retainers | Revenue is light and the transaction volume is already easy to track |

| Payroll-heavy company | You need a clean wage funding cycle and clear withholding control | Payroll is rare and your current process already works smoothly |

| Seasonal retailer or e-commerce brand | You want to separate peak-season cash from baseline operating funds | Seasonality is mild and cash swings are small |

| Multi-location operation | Each location needs its own spending limit or reporting view | Managers do not need separate visibility |

| Partnership or LLC with multiple owners | You want cleaner approval and draw control | The owners already rely on simple, trusted reporting |

Where it usually becomes overkill is in a small business with light transaction volume and no real need for cash segregation. If the owner is still moving money manually every few days, or if the team cannot describe why the second account exists, the setup is probably too clever. I would rather see one clean, well-reconciled account than three accounts that nobody manages with discipline.

That leads naturally to the next decision: if you do add accounts, what should each one actually do?

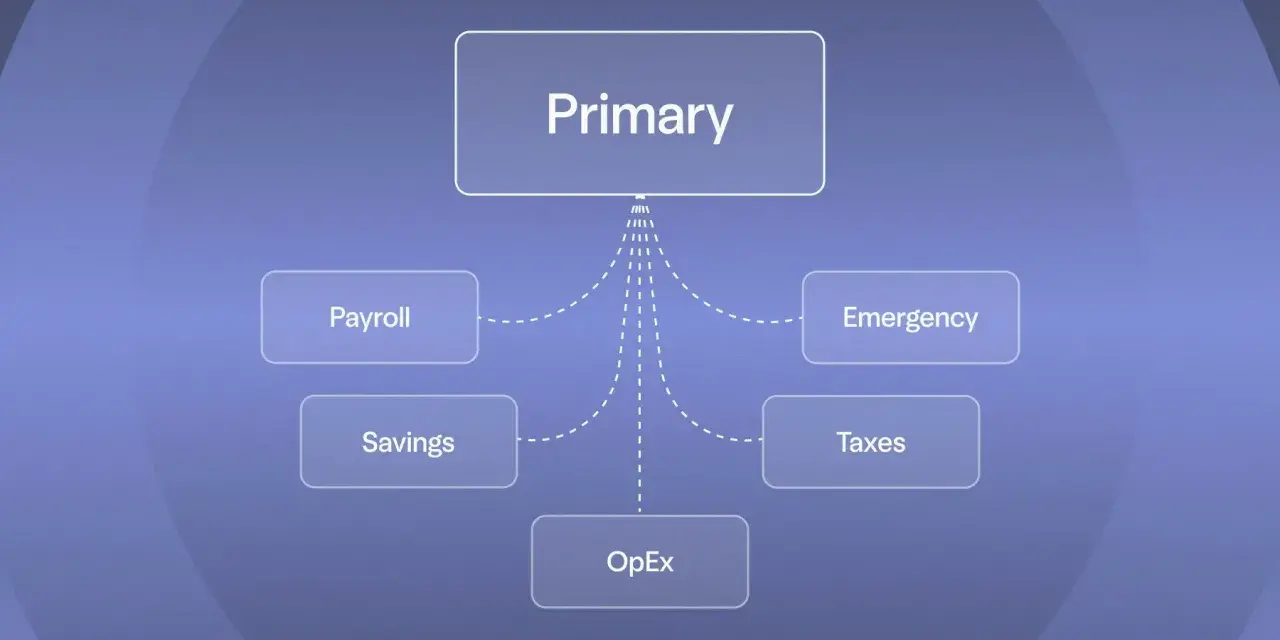

A simple structure that keeps money visible

I usually think in terms of buckets. Each bucket should have one purpose, one owner, and one clear rule for transfers. That keeps cash movement predictable and makes bookkeeping easier to audit later.

| Account type | Primary role | Best use case | Watch out for |

|---|---|---|---|

| Operating account | Daily inflows and outflows | Bills, vendor payments, normal card spend, customer deposits | Do not leave tax or payroll money sitting here |

| Payroll account | Fund wages and payroll-related withdrawals | Businesses with recurring payroll or contractor batches | Do not use it as overflow cash |

| Tax reserve account | Hold estimated tax money | Quarterly federal and state reserves, sales tax, payroll tax buffers | Never treat the balance as spendable working capital |

| Project or client account | Ring-fence a specific job, contract, or grant | Construction work, retained engagements, special campaigns | Avoid tiny, inactive accounts that never get used |

| Merchant clearing account | Temporary holding for card settlements | Businesses with high card volume that sweep funds on a schedule | Move money out on a timetable so it does not become a parked float account |

In this setup, the operating account is the only place where day-to-day spending should happen. The reserve accounts exist to protect the business from its own habits, not to collect idle balances. When the role of each account is obvious, reconciliation gets faster and decisions get better. From there, the real question is whether the cost of that structure still makes sense.

Fees, bank rules, and deposit insurance change the math

Every additional checking account has a cost, even if the monthly fee is waived. There is still transfer management, statement review, user setup, debit-card control, and bookkeeping cleanup. Some banks also require minimum balances, minimum activity, or relationship thresholds to avoid service charges, so a new account should earn its keep.

The insurance piece matters too. The FDIC insures deposits up to $250,000 per depositor, per insured bank, per ownership category. That means two business checking accounts at the same FDIC-insured bank, under the same ownership category, are generally added together for coverage purposes. Moving money to another bank can expand coverage, but only if the balances and legal structure actually support that strategy.

| Setup | Insurance picture | Operational trade-off |

|---|---|---|

| One bank, same ownership category | Balances in that category are added together for coverage up to the limit | Simplest to manage, but it does not multiply insurance |

| Two FDIC-insured banks | Coverage is separate at each bank | More logins and transfers, but useful for larger cash balances |

| Different ownership category at one bank | Separate coverage may apply only if the legal category truly differs | Useful in some structures, but not a trick for a standard operating account |

My rule is simple: do not split accounts just to feel safer. Split them when the balance structure, operating risk, or reporting need justifies it. If the numbers are modest, the simplest structure is usually the best one.

Once the structure is clear on paper, the system only works if the opening and bookkeeping rules are disciplined.

How to open and organize the accounts so the books stay clean

Opening the accounts is not hard, but I would not rush it. Banks commonly ask for an EIN or, in the case of a sole proprietorship, a Social Security number, plus formation documents, ownership agreements, and any required business license. I prefer to gather that paperwork first, then open accounts with a naming convention that makes the purpose obvious to anyone who sees the ledger.

- Define the purpose of each account before you apply.

- Pick a naming convention that matches the role, not just the bank product name.

- Assign authorized users and spending permissions deliberately.

- Set a transfer schedule, such as weekly or after each payroll run.

- Reconcile every account on a fixed cadence so small errors do not compound.

- Map each bank account to one line in the chart of accounts, which is the ledger's master list of categories.

I also like to keep one written rule for transfers. For example, tax money can move out of the operating account only on a set day each week, and payroll funding happens only after the payroll register is approved. That kind of discipline turns the banking setup into a control system instead of a collection of unused accounts. Even so, there are a few common mistakes that can undo the benefit quickly.

The mistakes that make the setup messy

- Using one account for everything. It looks simpler at first, but it makes it harder to know what is available, what is reserved, and what has already been spent.

- Opening accounts without a purpose. If the account does not solve a real cash-flow or control problem, it will usually become dead weight.

- Leaving reserve money in the operating account. Money that is meant for taxes or payroll should be ring-fenced, not sitting next to discretionary cash.

- Skipping reconciliation. A separate account is only useful if the balances and transactions are reviewed regularly.

- Ignoring signer and access changes. When partners, managers, or bookkeepers change, account permissions should change with them.

- Choosing names that sound alike. If no one can tell the payroll account from the operating account at a glance, confusion will follow.

The pattern behind most of these mistakes is the same: the business creates structure on paper but never operationalizes it. I have seen that happen in companies that were trying to look organized rather than actually be organized. The better version is lean, explicit, and boring in the best way possible.

The leanest setup that still gives you control

For most small and mid-sized businesses, I would start with one operating account and one reserve account, then add a third only if payroll, tax withholding, or a project budget creates a genuine control issue. That is enough structure for most teams without turning cash management into an extra job. I do not think multiple business checking accounts are the default answer for every company; I think they are a tool that should be added only when they improve control, lower error, or protect larger balances.

If the setup creates more transfers than insight, it is too complicated. If it gives you a cleaner view of cash, cleaner books, and cleaner authority over who can move money, it is probably doing exactly what it should. Keep the purpose explicit, keep the number of accounts modest, and let the structure serve the business instead of the other way around.