Startup company stock options can be one of the most misunderstood parts of a compensation package. They are not cash, they are not shares, and they are not automatically valuable just because the share count looks large. The real question is whether the vesting schedule, strike price, tax treatment, and exit path line up in a way that can turn equity into actual money.

The five things that matter before you treat equity as value

- Options give you the right to buy shares later at a fixed price, but you do not own stock until you exercise.

- A common U.S. schedule is four years of vesting with a one-year cliff, so leaving early can wipe out a large part of the grant.

- ISO and NSO grants are taxed differently, and an ISO exercise can trigger alternative minimum tax before any sale.

- The fully diluted percentage matters more than the raw share count, because dilution changes your real ownership.

- Liquidation preferences and future financing can reduce or eliminate the payout even when the company exits.

- The post-termination exercise window is often short, so timing can matter as much as upside.

What stock options actually give you

I usually start with the simplest truth: an option is a right to buy stock later, not stock you already own. The strike price, also called the exercise price, is the amount you pay per share if you decide to convert the option into common stock. If the company never grows past that strike price, the grant may have little or no economic value.

That is why options are so common in startups. They let a company conserve cash, reward people with upside, and align the team around enterprise value rather than just salary. From the employee side, the tradeoff is obvious: you are taking on risk now in exchange for a possible payout later. I think that trade is rational only when the company can explain how the grant fits into the broader compensation package, not just the headline number of shares.

One detail people miss is that the number of shares by itself tells you almost nothing. Ten thousand options at a high strike price can be worse than five thousand options at a low strike price if the first grant represents a tiny slice of the company or if dilution is likely to be heavy. The better question is always: what percentage of the company am I really being promised, and on what terms? The answer to that leads directly to vesting and timing.

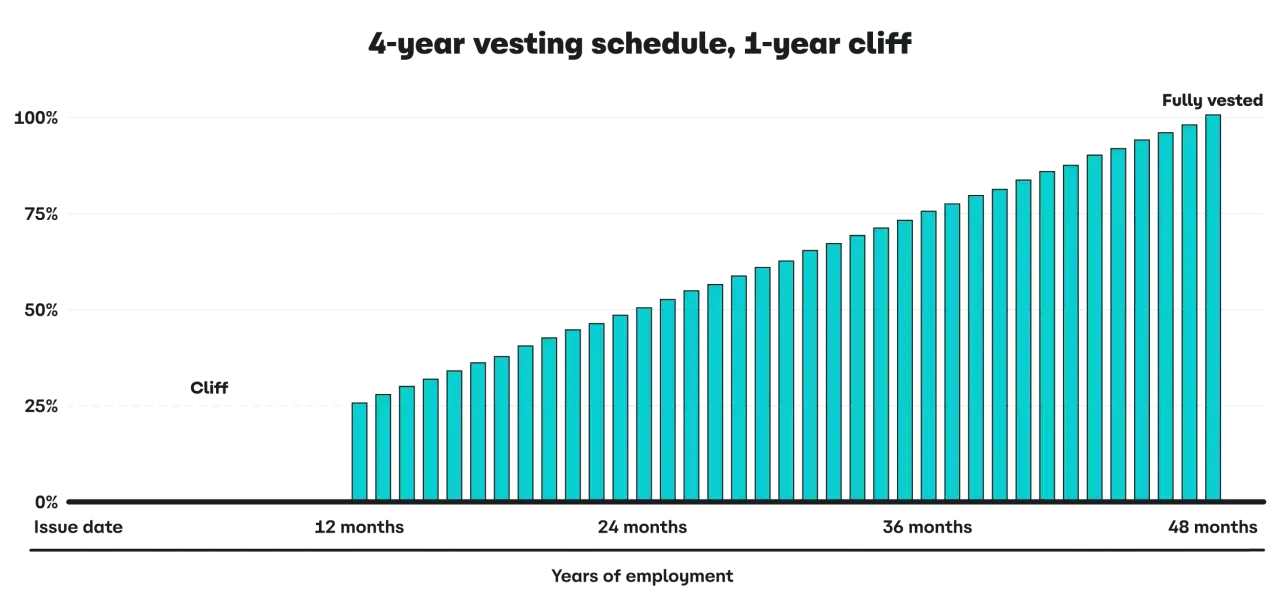

How vesting, exercise, and expiration work together

Vesting is the mechanism that turns a grant into earned equity over time. In many U.S. startups, the common pattern is four years of vesting with a one-year cliff, then monthly vesting after that. In plain English, that means you usually earn nothing if you leave before the first year, and after that you earn the grant gradually. If you leave at month 18, you are not halfway vested; you are typically at about 37.5% of a four-year schedule.

The common vesting pattern

The cliff matters because it protects the company from giving away equity to short-term hires, and it protects employees from reading too much into a grant they have not actually earned yet. If your offer says something different, read it closely. I have seen plenty of founders and recruiters describe a grant loosely, but the plan document is what controls the real economics.

What happens when you leave

Termination changes the clock fast. Many plans give you a short window, often 90 days, to exercise vested options after you leave the company. That window is not universal, but it is common enough that I treat it as a serious deadline, not a technical footnote. If you miss it, vested options can expire worthless even though you technically earned them.

That is where cash flow becomes real. If you have 20,000 options at a $2.50 strike price, exercising them costs $50,000 before tax. A lot of people discover too late that they like the upside on paper but cannot finance the purchase in practice. The next question is whether the tax rules make that cash outlay more expensive than it first appears.

Read Also: When to Apply for a Business Credit Card - Your Guide

Early exercise is useful only in specific cases

Some startups allow early exercise, meaning you buy shares before the options are fully vested. That can be useful in the right circumstances, but it is not a free lunch. You are moving cash into a risky asset sooner, and if you leave before vesting you may lose unvested shares. I treat early exercise as a planning tool, not a default recommendation.

Once vesting and exercise are clear, the real math shifts to taxes and the legal structure behind the grant.

The tax and legal rules that change the math in the U.S.

In the U.S., the SEC’s Rule 701 is the framework that usually lets private startups compensate employees with equity, and the IRS still draws the tax line between incentive stock options and nonqualified stock options. That distinction matters because the same-looking grant can lead to very different tax bills depending on how and when you exercise.

The strike price is usually set at fair market value on the grant date, often supported by a 409A valuation. That is why the option is typically not taxable when granted. The tax bill usually arrives later, at exercise or sale, depending on the type of option.

| Feature | ISO | NSO |

|---|---|---|

| Who can receive it | Employees only | Employees, consultants, and advisors |

| Tax at grant | Usually none | Usually none |

| Tax at exercise | Usually none, but AMT may apply | Ordinary income on the spread between strike and FMV |

| Tax at sale | Capital gain if holding-period rules are met | Additional gain or loss measured from the exercise basis |

| Special limits | 10-year term, $100,000 annual first-exercisable value limit, and a short post-termination exercise rule in many cases | Fewer federal option-specific limits, but the plan still controls the terms |

| Typical use | Tax-favored employee grants | More flexible grants for a broader set of contributors |

For NSOs, the taxable spread can be ugly if the company has grown quickly. If 20,000 NSOs have a $2 strike price and the fair market value at exercise is $10, the spread is $8 a share, or $160,000 of ordinary income before you sell anything. That is a large tax event to fund from your own cash. For ISOs, the risk shifts differently: you may avoid immediate ordinary income, but alternative minimum tax can still create a real bill before liquidity arrives.

Holding periods matter too. To preserve the most favorable ISO treatment, you generally need to hold the stock for at least one year after exercise and two years after grant. Sell earlier and you can trigger a disqualifying disposition, which may turn part of the gain into wage income. That is not a theoretical edge case; it is one of the most common places where employees misread the value of their grant. Tax rules are only one part of the story, though, because company structure can erase value even when the tax picture looks manageable.

How to judge whether the grant is worth something in the real world

When I evaluate an offer, I care far more about the fully diluted percentage than the raw share count. A cap table is the company’s ownership map on the assumption that all convertible securities and options are counted in. That is the number that tells you how much of the business you really own, not the glossy share count a recruiter may highlight.

Here are the questions I would press for before I treated the grant as meaningful compensation:

| Question | Why it matters | What I want to hear |

|---|---|---|

| What percentage of the company do these options represent on a fully diluted basis? | Raw shares can be misleading if the company keeps issuing more equity | A clear percentage, not just a share count |

| What is the strike price compared with current fair market value? | It sets the exercise cost and the starting point for upside | The strike is tied to the current 409A value |

| How large is the option pool and how much dilution is expected? | Future rounds often shrink your economic slice | A candid explanation of likely dilution |

| What liquidation preferences sit ahead of common stock? | Preferred investors get paid first in a sale | A cap-table explanation that I can actually follow |

| How long is the post-termination exercise window? | It determines how much time you have after leaving | A written number, not a vague promise |

| Is there change-of-control acceleration? | A sale may create value only if unvested equity accelerates | Clear terms, ideally with double-trigger protection for key roles |

Liquidation preferences deserve special attention. In many startups, investors hold preferred stock that gets paid before common stock does in an exit. If the sale price is modest relative to the money already invested, common shareholders can receive far less than the headline valuation suggests. I have seen exits that looked strong from the outside but produced thin returns for employees because the preference stack absorbed most of the value. That is why the company’s financing history matters just as much as its current valuation.

In short, a good grant is not just about the size of the option pool. It is about whether the company can exit at a price that clears the preference stack, leaves room for common stock, and still gives you enough after taxes and exercise cost. That leads naturally to the mistakes people make when they skip those checks.

The mistakes that make a decent offer look better than it is

- Counting raw shares instead of ownership percentage - 50,000 options can mean very different things at different companies.

- Ignoring the exercise cost - if the strike is high, the cash required to exercise can be substantial.

- Forgetting about taxes - especially on NSOs and on ISO exercises that trigger AMT.

- Assuming every exit creates a payout - preferences, debt, and dilution can leave common stock with little value.

- Missing the post-termination deadline - a short exercise window can make vested options expire before you can fund them.

- Treating verbal explanations as final - the plan document and grant notice control, not the sales pitch.

- Overestimating paper value - a high private valuation does not guarantee a liquid market or a clean exit.

I have seen people walk away from meaningful upside because they assumed they would have time to think later. In practice, the decision often arrives at the worst possible moment: right after leaving a job, right after a financing round, or right before a tax deadline. Good equity can still become bad economics if you do not have the cash, time, or information to act on it.

The best defense is a simple one: read the documents and run the numbers before you sign.

The few documents that tell you whether the upside is real

Before I rely on an equity grant, I want the plan, the grant notice, and a current cap-table snapshot. Those three items usually tell me more than a recruiting deck ever will. If the company cannot explain them clearly, I assume the grant is more speculative than advertised.

- The equity plan and grant notice - these define the legal terms, the number of options, and the vesting rules.

- Your percentage on a fully diluted basis - this is the cleanest way to understand real ownership.

- The strike price, 409A date, and expiration date - these determine cost, timing, and the option’s lifespan.

- The vesting schedule and termination exercise window - these show how long you need to stay and how quickly you must act if you leave.

- The change-of-control terms - this is where single-trigger and double-trigger acceleration can materially change value.

- The financing history and preference stack - this tells you whether common stock has a realistic path to being paid in an exit.

If those pieces make sense, the options are a real part of compensation. If they do not, I treat the grant as speculative upside, not guaranteed wealth. That is the simplest rule I use in practice, and it keeps the focus on what can actually be realized, not what looks impressive on paper.