For a business that looks profitable on paper but keeps running into timing gaps, flexible financing can matter more than another sales push. A working capital line of credit is built for that kind of problem: it helps cover short-term operating costs, then lets you repay and draw again as cash comes in. In this article I break down how it works, when it is a smart move, what it really costs, and how to use it without turning a temporary bridge into expensive permanent debt.

The fastest way to think about it is as a reusable cash-flow bridge, not extra revenue.

- You borrow only what you need, and interest usually accrues only on the amount you draw.

- It fits recurring timing gaps such as payroll, inventory buys, rent, taxes, and slow-paying customers.

- It is usually a weak fit for equipment, acquisitions, or any project that needs long-term amortization.

- Fees, collateral, renewal terms, and minimum payments can matter as much as the headline rate.

- Lenders care about consistency, not just sales volume, so clean books and a clear repayment path matter.

What this revolving facility actually does

When I evaluate a revolving working-capital facility, I start with the basic question behind it: is the business short on cash, or short on profit? The answer matters because this tool is designed to solve a timing problem. You draw funds when bills arrive, repay them when receivables clear, and then reuse the credit again without applying for a new loan.

That structure makes sense when the business is healthy but cash is uneven. A contractor may need to pay labor and materials before a client pays a progress invoice. A distributor may have to buy inventory before the seasonal rush. A service company may need to make payroll while waiting on a few large accounts to settle.

In practical terms, I treat it as short-term liquidity support, not a substitute for permanent capital. If the business needs months or years of breathing room, a revolving line is usually the wrong instrument. Once you see it that way, it becomes much easier to judge whether the next dollar should come from credit, retained cash, or a different financing structure.

When it makes sense and when it doesn’t

The strongest use cases are the ones where the cash comes back on its own inside a predictable operating cycle. If the money leaves the business for a short period and then returns through normal operations, the line is doing exactly what it should.

- Seasonal inventory buildup - useful when you need to buy stock before demand peaks and expect sales to refill the line.

- Payroll and vendor timing - useful when payables hit before customer payments do.

- Contract mobilization - useful when you must fund labor, materials, permits, or subcontractors before the project pays out.

- Emergency repairs - useful when a cash shock would interrupt operations, but the expense itself is temporary.

The weak use cases are usually easy to spot once you strip away the urgency. If the money is for a machine that will be used over five years, a property project, an acquisition, or chronic losses that keep repeating, the line is probably masking a structural problem. That is where I see owners get into trouble: they use a flexible product for a problem that really needs term debt, equity, or an operational fix.

There is also a useful nuance here. Some businesses, especially in retail or restaurants, can operate with tighter working-capital levels because they convert sales to cash quickly. In those cases, the line is not there to patch a broken model; it is there to smooth ordinary swings. That trade-off leads naturally into the next question: how this tool compares with other ways of funding the same need.

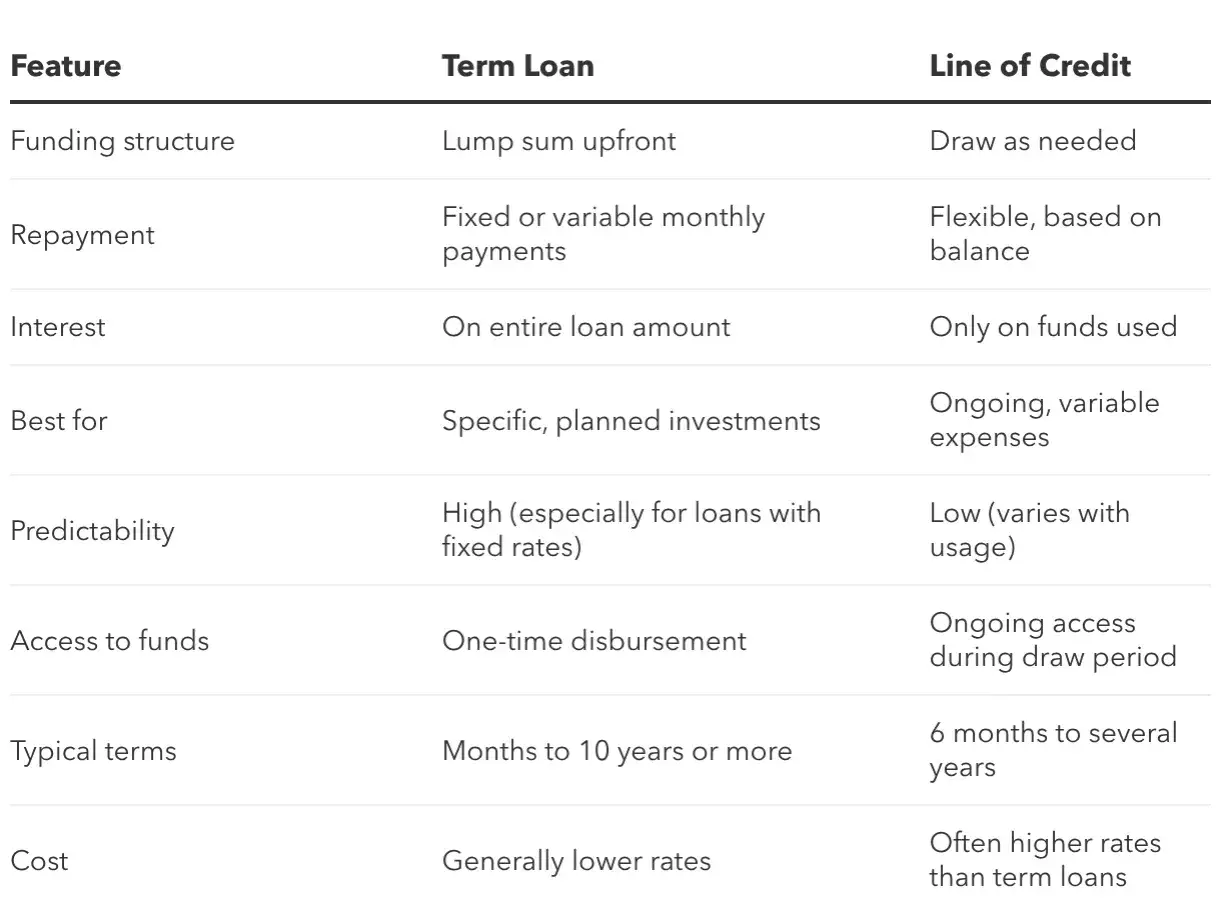

How it differs from a term loan and a business credit card

A lot of confusion disappears when you compare financing tools side by side. The headline is simple: a revolving line is for repeated draws, a term loan is for one known lump sum, and a credit card is for speed and convenience, not usually for the cheapest capital.

| Funding tool | Best for | Main trade-off |

|---|---|---|

| Revolving business line | Recurring cash-flow gaps, seasonal inventory, payroll timing, contract work | Variable pricing, renewal risk, and possible fees if you do not use it carefully |

| Term loan | One-time purchases and projects with a defined cost | Less flexible because you receive the full amount upfront and repay on a fixed schedule |

| Business credit card | Small, fast purchases and short emergency spending | Convenient, but the cost can rise quickly; card APRs often run well above typical small-business borrowing costs |

| Government-backed revolving line | Businesses that need more structure, more time, or a specialized purpose | More paperwork, more monitoring, and a slower approval process |

Two large-bank examples show how different the same basic product can be. U.S. Bank offers a revolving Cash Flow Manager line up to $250,000, with a $0 annual fee on lines greater than $50,000 and a $150 annual fee on smaller lines. Bank of America’s unsecured line page lists a $0 origination fee and a $150 annual fee that is waived for the first year. That spread is why I never compare these products by rate alone; the fee structure can change the real cost more than people expect.

Once you know the structure, the next filter is underwriting. That is where lenders decide whether your cash flow looks stable enough to support the line.

What lenders actually look at before they approve you

Most lenders are not looking for perfection. They are looking for proof that the business can convert operations into cash with enough predictability to repay what it borrows. In practice, that usually comes down to five things.

- Time in business - newer businesses can qualify in some cases, but longer operating history usually improves the odds and the terms.

- Revenue consistency - a lender wants to see whether sales are stable, seasonal, or too erratic to support regular draws and repayments.

- Credit profile - both personal and business credit still matter, especially where the owner is guaranteeing the debt.

- Debt load - if existing obligations already consume too much cash, a new line can make the squeeze worse.

- Reporting quality - clean bank statements, current financials, tax returns, and receivables aging reports help a lender trust the numbers.

I also pay attention to structure. Some lenders require a personal guarantee from owners with meaningful equity stakes. Some only offer secured lines, which means the lender can take collateral if the business defaults. Others are willing to lend on an unsecured basis, but the size is smaller and the approval bar is higher. In the real world, that means the same business may be a strong candidate for one lender and a weak one for another.

If you are preparing an application, I would have 12 months of bank statements, recent profit-and-loss reports, a balance sheet, tax returns, and any accounts-receivable or accounts-payable aging reports ready before you submit anything. That preparation becomes even more important when you want to use the line strategically instead of defensively.

How I would use it strategically without creating dependency

The best way to use a revolving line is to tie it to a specific cash-flow cycle. I like to define the use case first, then the repayment trigger, and only then the borrowing limit. That sequence keeps the line from becoming a habit.

- Set a draw limit based on the cycle - for many businesses, that means covering a 30- to 90-day timing gap, not funding open-ended spending.

- Borrow against visible inflows - use the line against invoices, booked contracts, or seasonal sales you can reasonably expect, not against hope.

- Repay from operating cash, not rescue money - the line should shrink as cash returns, not stay maxed out month after month.

- Watch for structural drift - if you keep drawing after one normal operating cycle, the issue may no longer be timing.

- Protect a backup reserve - a line is more useful when it supplements a small cash cushion instead of replacing it.

My rule of thumb is simple: if the line is still carrying a large balance after the business has had time to complete one full cash cycle, I treat that as a management signal. Either pricing is off, collections are too slow, inventory is sitting too long, or the underlying cost structure needs a reset. Credit can buy time, but it cannot fix a business model that burns cash faster than it produces it. That is why the final check should always be the document itself.

The checks I would make before signing anything

Before I would rely on any line, I would read the agreement for the details people tend to skim past. The rate matters, but the fine print decides whether the product stays flexible or becomes irritatingly expensive.

- What is the all-in cost, including annual fees, draw fees, maintenance fees, and any required balance?

- Is the rate variable, and if so, what index does it track?

- Does the lender require a personal guarantee or specific collateral?

- How often does the line renew, and what can cause a reduction or cancellation?

- What financial reporting must you provide after funding?

- How quickly can you access funds when you need them?

If I were advising a management team, I would want these points documented in the same discipline we use for any major operating decision: who can draw, when the line refreshes, how the balance is monitored, and what happens if receivables slow down. In a governance sense, that is what turns a credit product into a controlled liquidity tool rather than a vague source of pressure.

The cleanest use of a revolving line is also the most disciplined one. Treat it as a bridge between cash outflow and cash collection, keep the purpose narrow, and make sure the repayment path is visible before you draw a dollar.