The business credit card vs personal decision is really about control: who is liable, how cleanly you can separate expenses, and whether the account helps or complicates your bookkeeping. I focus on this choice because it affects tax prep, cash flow, and governance discipline more than it affects day-to-day convenience. In 2026, the smartest answer depends less on the logo on the card and more on how your business spends, who spends it, and how much separation you want between company money and your own.

The right card depends on liability, bookkeeping, and how you spend

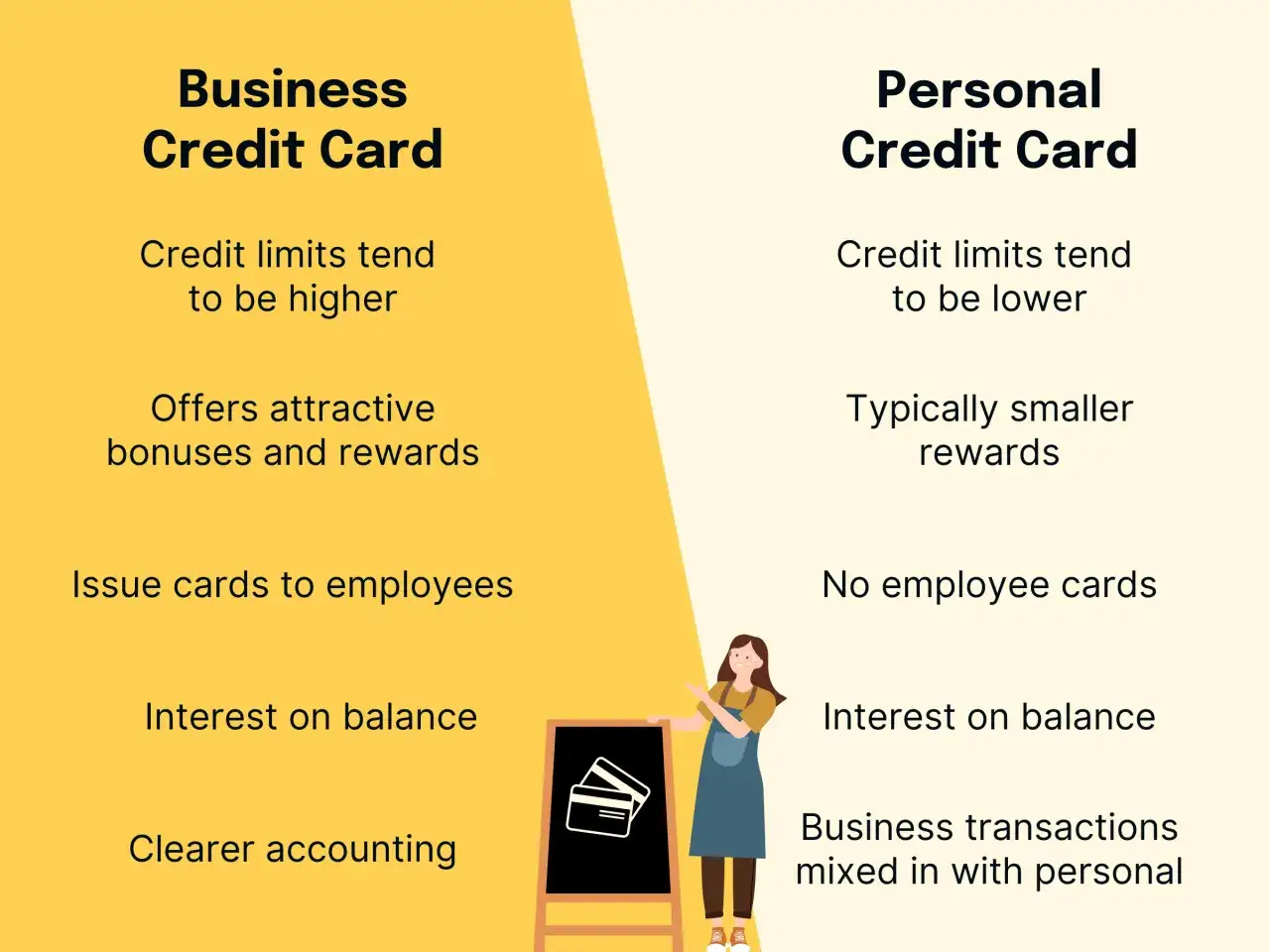

- Business cards are built for company spending and often add employee cards, spending limits, and accounting tools.

- Many issuers still review the owner’s personal credit and may require a personal guarantee.

- Personal cards can work for tiny or early-stage businesses, but the records are usually messier.

- Tax treatment depends on the expense and documentation, not on which card you used.

- If business credit matters, check whether the issuer reports to commercial bureaus.

Why this choice affects more than rewards

I see owners get distracted by points, but the real issue is boundary-setting. A separate business account makes it easier to track deductible expenses, reimburse owners, and show which charges belong to the company. The IRS says keeping business and personal accounts separate makes records easier, and it expects supporting documents such as statements and receipts.That separation matters even more if you operate through an LLC or corporation. Good governance is not just about entity paperwork; it also shows up in how consistently you handle company spending. A business card can support that discipline, while a personal card for company use can blur it quickly. Once that baseline is clear, the practical differences become much easier to judge.

How business and personal cards differ in practice

| Factor | Business card | Personal card | Why it matters |

|---|---|---|---|

| Intended use | Company expenses such as software, ads, travel, shipping, and inventory | Household and consumer spending | Using the right tool makes it easier to keep records clean |

| Approval | Often asks for business details and still checks the owner’s personal credit | Usually based on consumer credit and personal income | Many business cards still lean on the owner’s credit profile |

| Liability | Often includes a personal guarantee, even though the card is for the business | Personally liable by default because it is your consumer account | Neither card automatically removes the owner from the hook |

| Credit reporting | May report to commercial bureaus; some issuers also report certain activity to consumer bureaus | Reports to consumer bureaus | This affects whether the account helps your business file, your personal file, or both |

| Expense controls | Often includes employee cards, limits, receipt capture, and accounting integrations | Usually fewer business controls | These tools matter once more than one person spends on behalf of the company |

| Rewards | Often tuned to business categories such as shipping, ads, office spend, or travel | Often tuned to personal categories such as dining, groceries, and travel | The best earn rate is the one that matches your actual spend pattern |

| Tax admin | Usually easier to isolate business charges and support substantiation | Usable, but can be harder to separate from personal spending | Clean substantiation matters more than the card label itself |

| Cost structure | Can have annual fees, but may justify them with controls and business features | Can also have fees, but benefits are usually consumer-focused | Price should be measured against the features you will actually use |

The important point is not that one is always cheaper or safer. It is that business cards are designed to keep company spend observable, while personal cards are designed around consumer use. That design choice drives most of the trade-offs. From there, the next question is when the business version is actually worth it.

When a business card is the stronger move

I usually recommend a business card when the company has enough moving parts that manual tracking starts to break. In those cases, the card is not just a payment method; it becomes part of the finance system.

- You have recurring business categories. If the same types of charges appear every month, a business card makes reconciliation much cleaner.

- You need more than one cardholder. Employee cards and custom spending limits matter as soon as someone besides the owner starts buying on behalf of the business.

- You want cleaner month-end close. Receipt capture, export tools, and accounting integrations reduce the time spent sorting charges later.

- You want to build business credit. That can be useful for future financing, but I would only choose for this reason if I knew how the issuer reports.

- You want better governance discipline. Separate business spending helps owners, managers, and accountants see what the company is actually doing.

There is also a practical tax advantage in the background: when company purchases stay in one place, you are less likely to miss deductions or mix in personal charges by accident. That is why business cards make the most sense once the company has enough volume or enough people involved to justify a more structured setup. The opposite case is where a personal card can still be rational.

When a personal card can still make sense

A personal card is not automatically wrong for business spending. It can be the practical choice when the company is tiny, the volume is low, or you do not yet qualify for a strong business card. I see this most often with freelancers, solo consultants, and side businesses that are still proving their revenue pattern.

- Your business is still small. If you make only a handful of purchases each month, a personal card can be workable.

- You already have a strong consumer card. If the rewards, protections, and credit line are excellent, that may outweigh the inconvenience for limited business use.

- You need a simple short-term bridge. Some owners use a personal card while they wait for stronger business cash flow or better eligibility.

- You are very disciplined about records. If you tag every charge and reconcile every month, the setup can stay manageable.

Even then, I would keep a separate ledger and save every receipt. The IRS expects business expenses to be supported by records, and the card type does not turn a personal expense into a deductible one. If you take this route, the next section matters even more, because the fine print is where the real surprises live.

The fine print that changes the outcome

Most bad decisions here come from assumptions, not from the card itself. I usually watch for four mistakes.

- Assuming business cards remove personal responsibility. Many small-business cards still include a personal guarantee, so the owner remains liable if the account goes unpaid.

- Assuming every business card builds business credit. Reporting is issuer-specific. Some cards help your business file, some affect both files, and some do less than owners expect.

- Chasing rewards before structure. A rich points bonus is not much help if the card has poor controls, weak reporting, or a fee structure that does not match your spend.

- Mixing personal and company charges. Once that starts, month-end close gets slower and the paper trail gets weaker.

I treat those checks as non-negotiable because they affect liability and reporting, not just points. Once they are clear, the choice becomes much easier to make. That is why I reduce the decision to a simple rule set.

A simple decision framework for 2026

- Choose a business card if you need separation, employee controls, recurring company spend, or a path toward business credit.

- Choose a personal card only if business spending is limited, simple, and easy to document.

- Check reporting before applying if building business credit matters to you.

- Compare real costs, not headline perks by weighing annual fees, rewards categories, and the time saved on bookkeeping.

- Match the card to your operating model rather than forcing one account to cover both household and company spending.

In practice, I think the best card is usually the one that matches your administrative reality. If your business is still lean, a personal card can be a temporary bridge. If your operation is growing, the business card usually pays for itself in control and clarity.

The habits that make either card work better

The card itself matters less than the system around it. I have seen good cards fail because the owner never built a repeatable process, and I have seen ordinary cards work well because the books were disciplined.

- Reconcile charges every month instead of waiting until tax season.

- Keep digital copies of receipts for travel, meals, supplies, and equipment.

- Set spending rules for anyone who has access to the card.

- Review the annual fee and rewards mix once a year to see whether the card still fits.

- Move business spending off a personal card as soon as the business has enough volume to justify separation.

A clean card setup does not just make accounting easier. It helps you make better decisions about cash flow, deductibility, and financial control, which is exactly where a business owner should spend attention.