Credit card processing can quietly become one of the largest variable costs in a small business. The real issue is not just the headline percentage; it is how interchange, network fees, processor markup, and fixed per-transaction charges combine on your statement. This article breaks down what those charges mean, what typical US pricing looks like, and how I would compare quotes before signing anything.

The fastest way to read a processing quote is to separate the rate from the structure

- Effective cost matters more than the advertised rate. The true number is total fees divided by card sales.

- Card-present sales are usually cheaper than keyed or online payments. Lower fraud risk usually means lower fees.

- Flat-rate pricing is simple, but not always the cheapest. It often works best for low volume or low-ticket sales.

- Interchange-plus is usually the most transparent model. It makes the processor’s markup easier to see and negotiate.

- Monthly fees and dispute costs can change the math fast. A quote that looks cheap can still be expensive once extras are added.

What those charges actually cover

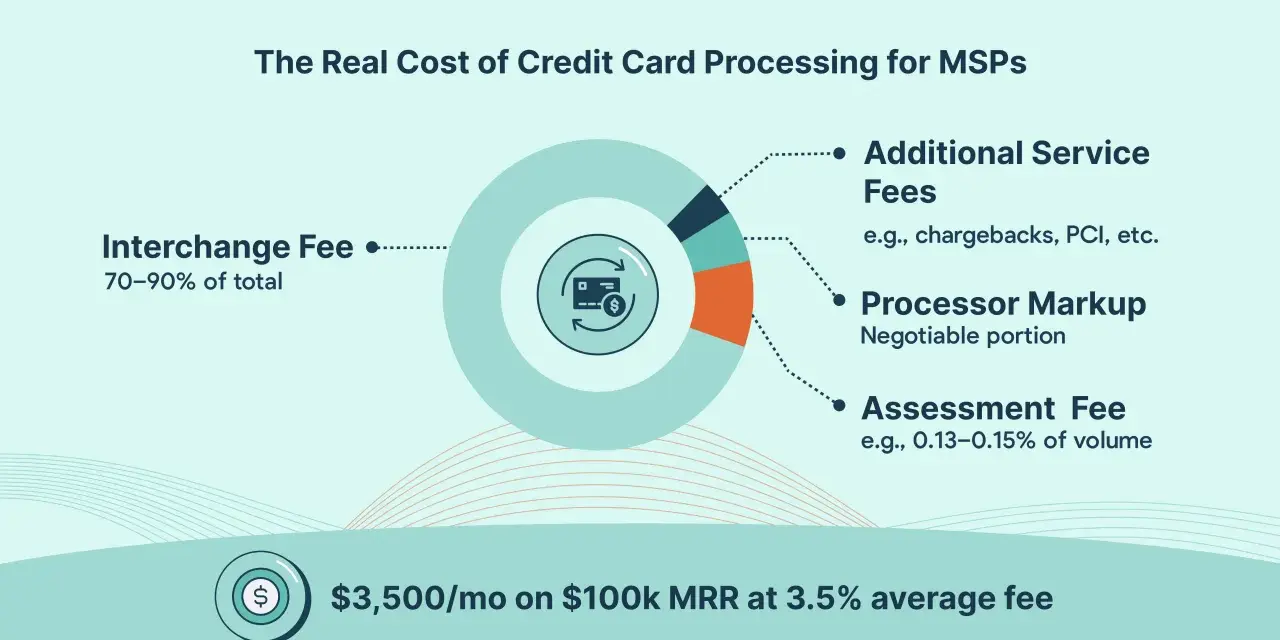

When I read a merchant statement, I treat it as three layers stacked together. Part of the money goes to the card issuer as interchange, part goes to the card network as an assessment, and part goes to the processor or merchant account provider as markup. If the sale is online, a payment gateway or platform fee may sit on top of that. In plain English, you are paying for risk, routing, fraud handling, and the infrastructure that moves the money from the customer to your bank.

- Interchange is the largest piece in most transactions and is usually set by the card networks and issuers rather than by your processor.

- Network assessments are smaller charges tied to the brand that handles the card.

- Processor markup is what your provider keeps for the service itself.

- Gateway fees show up more often with online or invoiced payments because the processor also has to move the transaction through a secure checkout layer.

- PCI compliance fees cover the security work of handling card data under PCI rules, and some processors charge extra for the program itself or for non-compliance.

- Refund costs can linger too, because in many systems the original processing fee is not returned when you refund a customer.

That separation matters because a low advertised rate can hide a heavy markup, and a high advertised rate may still be fair if it bundles more of the stack into one number. Once you know what is inside the total, the next decision is which pricing model fits your sales pattern.

The pricing model matters more than the headline rate

I compare processing plans by predictability and scale, not by marketing language. The model tells you whether the provider is giving you a transparent pass-through structure or wrapping everything into one easy-to-read rate.

| Pricing model | How it works | Best fit | Main trade-off |

|---|---|---|---|

| Interchange-plus | You pay interchange and network costs plus a disclosed markup. | Businesses that want transparency, meaningful volume, or room to negotiate. | Monthly bills can vary, so forecasting takes more work. |

| Flat-rate | One percentage plus one fixed fee per transaction. | Low-volume sellers, startups, and teams that want simple math. | The convenience premium can be expensive as ticket size and volume rise. |

| Tiered | Transactions are sorted into qualified, mid-qualified, or non-qualified buckets. | Occasionally useful for sales teams that want a simple pitch. | It is usually the least transparent option and the hardest to optimize. |

| Membership or subscription | You pay a monthly fee, then a lower markup on each transaction. | Higher-volume merchants that can absorb the subscription cost. | It only wins if your processing volume is high enough to justify the monthly fee. |

In practice, I see flat-rate pricing work well for businesses with modest volume and uneven sales, while interchange-plus tends to win once volume becomes stable enough to reward transparency. The same payment mix can produce very different bills under those two structures, so the next section is about anchoring expectations with current US pricing.

What small businesses are paying in the US right now

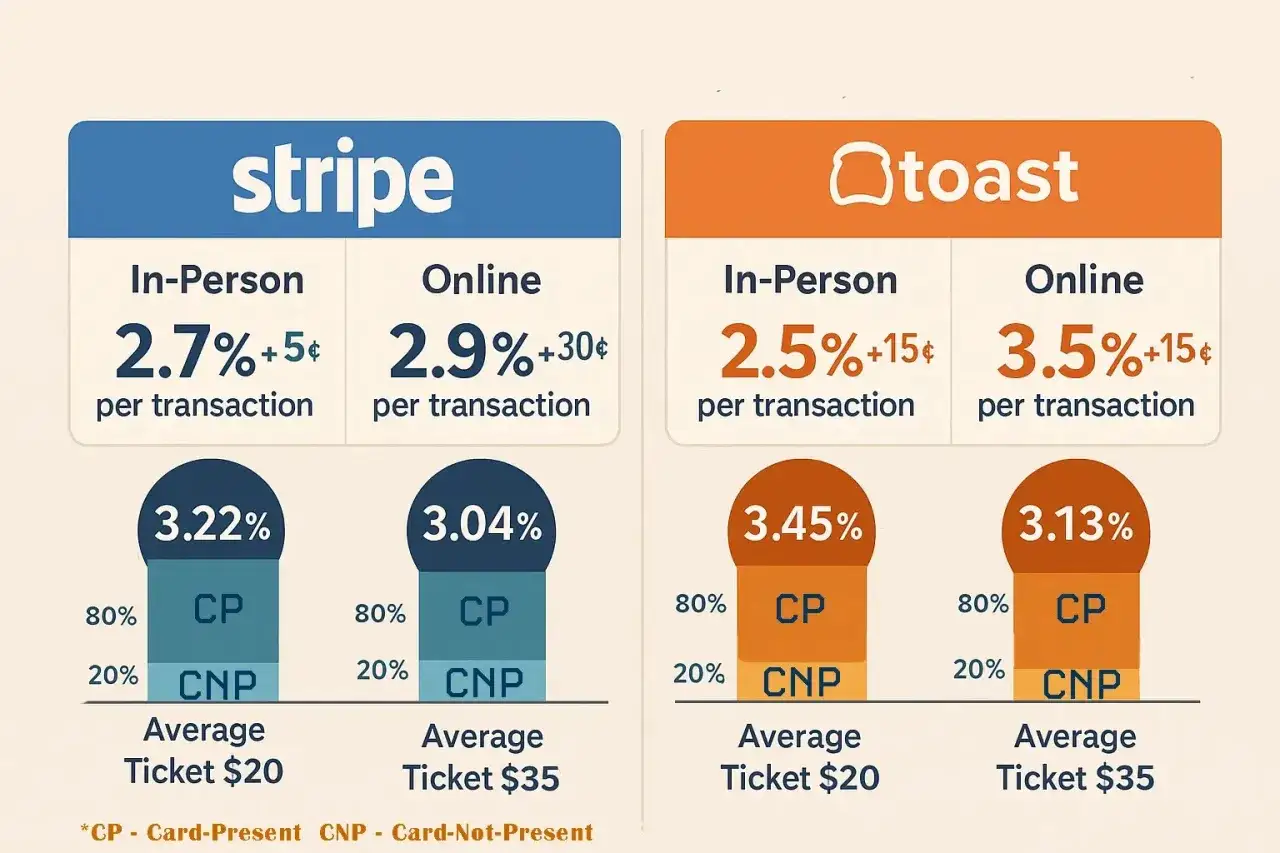

A realistic planning range for card processing is roughly 1.5% to 3.5% per transaction, but the blended total is often called the merchant discount rate, and the effective rate can drift higher once you add fixed per-sale fees, monthly charges, and dispute costs. Current US examples make that easier to see: Square lists 2.6% + 15¢ for tap, dip, or swipe and 3.3% + 30¢ for online or invoiced card payments, while PayPal’s US fee table shows 2.99% + $0.49 for standard card payments and 3.49% + $0.49 for PayPal Checkout.

| Transaction pattern | Why it usually costs what it costs | What to watch |

|---|---|---|

| Card-present retail | Lower fraud risk and faster verification usually keep pricing closer to the bottom of the range. | Look for hidden monthly fees, not just the swipe rate. |

| Online or invoice payments | Card-not-present transactions carry more fraud exposure, so the processor charges more. | Gateway, platform, or verification fees can stack quickly. |

| Keyed or manual entry | Manual entry is riskier, so the fee is often noticeably higher. | A business that keys cards often is usually leaving money on the table. |

| International or cross-border cards | Currency handling and risk controls add cost. | Watch for percentage surcharges plus conversion fees. |

The big lesson is that the same processor can be cheap for one sales channel and expensive for another. That is why I never compare quotes without running the numbers against the business’s actual monthly mix.

How to calculate your real monthly cost before you sign

The simplest formula is this: total processing cost = percentage fee + fixed per-transaction fee + monthly fees + add-ons. Once you divide that total by card sales volume, you get the effective rate, which is the number that tells the truth.

| Monthly sales pattern | Flat-rate quote: 2.6% + 15¢ | Lower-rate quote: 2.0% + 10¢ + $49 monthly fee | Cheaper option |

|---|---|---|---|

| 10 transactions at $50 each = $500 | $14.50 total | $60.00 total | Flat-rate |

| 300 transactions at $40 each = $12,000 | $357.00 total | $319.00 total | Lower-rate quote |

That example is the reason fixed fees matter so much. A plan with a monthly subscription can look worse on paper but still save money once volume is high enough, while a simple flat-rate plan can be the smarter choice when sales are light or inconsistent. If your average ticket is small, the per-transaction cents matter more; if your average ticket is large, the percentage matters more.

For me, the cleanest comparison comes from running the last 30 days of actual sales through two quotes and checking the effective rate side by side. That takes the guesswork out of the decision and makes the next step, cost reduction, much easier.

How I would cut fees without slowing down checkout

The lowest-friction savings usually come from changing behavior, not chasing a miracle provider. A few adjustments tend to move the needle faster than others.

- Push card-present payments whenever possible. Tap, chip, or wallet payments are usually cheaper than keyed entries because fraud risk is lower.

- Use ACH for B2B invoices when the economics justify it. Bank transfer fees are often materially lower than card fees for larger invoices or recurring bills.

- Keep your statement descriptor easy to recognize. Fewer confused customers means fewer disputes, and disputes are expensive even before the chargeback fee lands.

- Fix operational causes of chargebacks. Clear shipping times, easy refund rules, and fast support reduce the kind of disputes that eat margin.

- Review add-ons every month. A $15 PCI fee is $180 a year, and a $10 statement fee is another $120 before you process a single sale.

- Match the pricing model to your ticket size. Small-ticket businesses usually care more about the fixed cents; high-ticket businesses care more about the percentage.

If you are considering surcharging or cash discounting, I would check state rules and card-network terms first. The strategy can make sense, but compliance mistakes can be more expensive than the savings.

The contract details I would read twice

Most bad processing deals do not look bad in the headline rate. They become expensive in the fine print, where the provider quietly earns back the discount through extra fees, long commitments, or rate changes.

| Clause or fee | Why it matters | What I look for |

|---|---|---|

| Early termination fee | It makes switching expensive even if the new offer is better. | No fee, or at least a short contract with a clear exit. |

| PCI non-compliance fee | A small monthly penalty can pile up if the business misses a checklist item. | Simple compliance requirements and a realistic deadline. |

| Monthly minimum | You pay up to a floor even when sales are slow. | A minimum that matches your seasonal pattern, or none at all. |

| Gateway or platform fee | Online sellers can pay this on top of the transaction rate. | A clear explanation of what the fee unlocks and whether you actually need it. |

| Chargeback fee | A single dispute can cost more than the original profit on a sale. | Know the amount before you sign; many merchants see fees in the $15 to $50 range. |

| Equipment lease or rental | Leasing hardware can cost far more than buying it outright. | Prefer owned hardware unless the rental terms are genuinely flexible. |

| Rate increase clause | A low starting rate is not useful if it can change quickly. | Written notice, caps, and a right to leave if pricing changes materially. |

When I review contracts, I look for the total cost of staying, not just the cost of signing. That lens is especially important for small businesses, because a few small fees can become a meaningful drain over a full year.

The quote that looks cheapest can still cost more

If I had to make the decision today, I would start with the business’s actual payment mix, then ask three questions: how many transactions do you run each month, what is the average ticket, and how often do you process cards online versus in person? Those three inputs decide whether a simple flat-rate plan, an interchange-plus quote, or a monthly subscription structure is the better fit.

- Low volume and low complexity usually favor flat-rate pricing because the savings from a lower markup may not beat the convenience.

- Stable volume and higher ticket sizes often favor interchange-plus or subscription pricing because the processor’s markup becomes easier to optimize.

- Online-heavy businesses should pay extra attention to gateway, fraud, and dispute costs, not just the card rate.

- B2B businesses should compare card acceptance against ACH, because not every invoice needs to be paid with a credit card.

- Cash flow-sensitive businesses should compare payout timing as well as rate, because faster settlement can be worth a slightly higher fee.

The rule I use is simple: compare the effective rate on real sales data, not the prettiest marketing quote. If you do that, the right processor usually reveals itself quickly, and you will know whether the savings are worth the complexity. That is the number I would manage month after month, because it is the one that shows what you are truly giving up to accept card payments.