This article explains what happens if you default on an unsecured business loan, including the collection steps, legal exposure, and the practical options that still exist before the account hardens. The short version is simple: “unsecured” removes collateral from the equation, but it does not remove the debt or the lender’s leverage. I am breaking it down in the order that matters most to a business owner, not a lawyer’s filing cabinet.

The real danger is escalation, not instant asset seizure

- Default usually means you missed the contract’s cure deadline or breached another loan term, not just that cash flow got tight.

- Lenders can add fees, accelerate the balance, move the file to collections, and sometimes sue for judgment.

- If you signed a personal guarantee, the owner’s personal assets can become part of the recovery strategy.

- Business credit almost always suffers; personal credit can be hit too when a guarantee or personal reporting is involved.

- Forbearance, restructuring, settlement, and bankruptcy are all possible, but timing decides how useful each one is.

What default actually means once the contract clock runs out

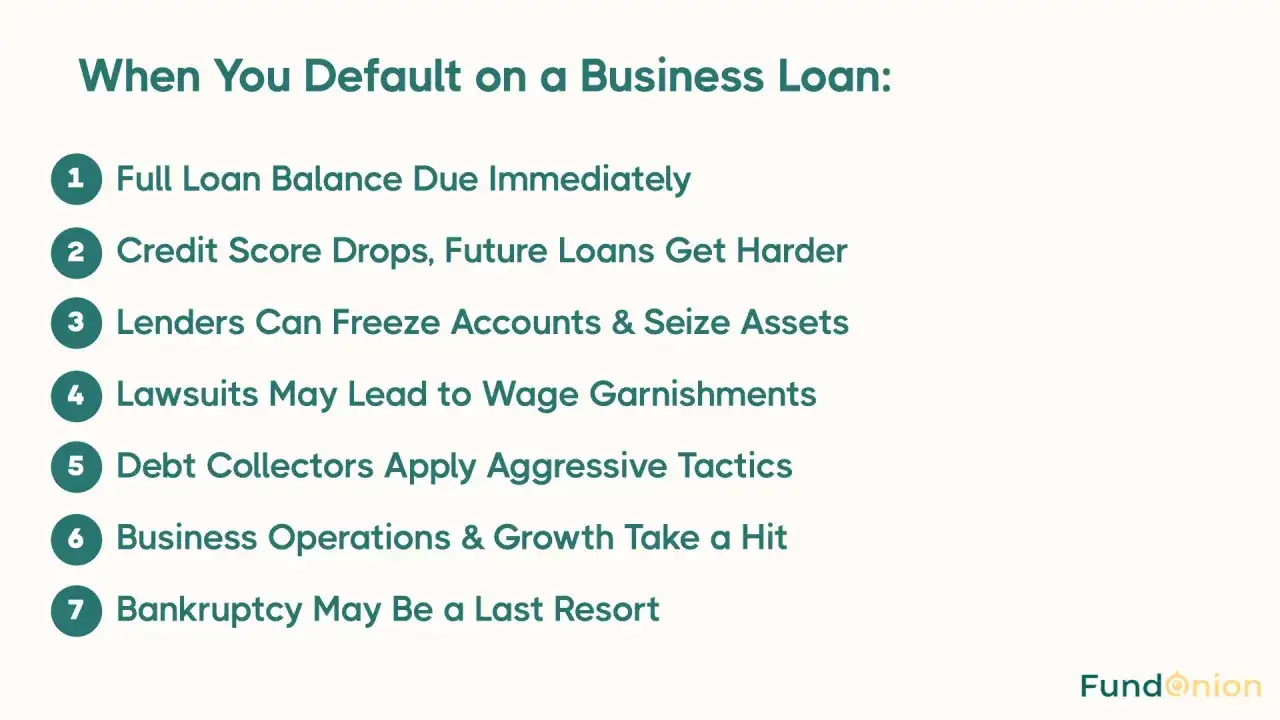

Default is not just “a missed payment.” In a business loan, the contract usually defines default broadly: a payment that stays unpaid past the cure period, a broken financial covenant, a tax lien, a lawsuit, a false statement in the application, or even a bankruptcy filing. That is why the loan documents matter more than the label on the product. Once the lender says the account is in default, it can usually add late fees, default interest, and collection costs, then accelerate the balance, which means the full remaining amount becomes immediately due.

That distinction matters because charge-off is not forgiveness. It is an accounting step that says the lender no longer expects normal repayment; it does not erase the debt. Once that happens, the next question is not whether the debt exists, but how hard the lender can press. That takes us to the collection tools lenders usually use first.

The first moves lenders usually make

Before anyone files a lawsuit, most lenders try a sequence of pressure and documentation. The exact order varies, but the pattern is familiar: reminders, demand letters, calls from internal collections, then a handoff to outside collectors or counsel if the file keeps deteriorating. The CFPB notes that the FDCPA is aimed at consumer debts, not business debts, so commercial borrowers should expect a different collection framework than the one people know from credit cards.

- They send a default notice or demand letter and ask for immediate payment or a workable proposal.

- They may freeze additional draws on a line of credit or stop advancing new funds.

- They can transfer the account to a collection agency, a law firm, or a debt buyer.

- They often request updated financial statements to see whether a workout is realistic.

- They may file suit if they believe the account will not cure voluntarily.

Many lenders would rather recover money through negotiation than through court, but once the file looks stale or disputed, the escalation can move fast. The real leverage shows up in the fine print, which is why the word unsecured deserves a closer look.

Why unsecured does not always mean untouchable

I usually read the guarantee and the remedy clause before I worry about the interest rate, because that is where the real exposure lives. The SBA points out that many unsecured business lenders still require a personal guarantee, which means the owner may be personally on the hook even when the loan is not backed by a specific piece of collateral.

| Borrower setup | What is usually at risk | Why it matters after default |

|---|---|---|

| Sole proprietorship | Business and owner assets often overlap | The lender may treat the business and the owner as one practical target for collection |

| LLC or corporation with no personal guarantee | Usually the business itself and its assets | Owner protection is better, but it is not absolute if the lender alleges misuse of the entity |

| Any loan with a personal guarantee | The guarantor’s personal assets, depending on the wording | The lender can pursue the owner directly, even if the business is a separate legal entity |

| Loan with a hidden lien or broad security language | Accounts, receivables, deposits, or other pledged business assets | The deal may be less “unsecured” than the marketing copy suggests |

The legal structure matters just as much as the loan structure. If you signed personally, the lender may be able to pursue you even if the company is an LLC or corporation. If you did not sign personally, the owner’s personal assets are usually better insulated, although courts can still look at issues like fraud, commingling, or veil piercing, which is the legal theory used to disregard the company wall when the entity was not respected. Once you know who is exposed, the next issue is how the default hits your credit and future borrowing power.

How the default damages credit and future borrowing power

A default on a business loan can follow you in two directions at once: the business side and, in some cases, the personal side. Business credit profiles can take a hit from missed payments, collection activity, and lawsuits, which makes future working capital more expensive and harder to obtain. Suppliers may tighten terms, landlords may ask for larger deposits, and lenders may shift from unsecured offers to secured deals or personal guarantees.

Personal credit can also be affected if you signed a guarantee or the lender reported the account in a way that ties back to you individually. Even when your personal file is untouched, the practical result is similar: less bargaining power, smaller credit limits, and higher pricing on the next round of financing. That is why the next step is not panic; it is deciding whether the account can still be rescued through a workout, settlement, or bankruptcy strategy.

The realistic ways out before the file hardens

Not every default has the same ending. Some businesses can stabilize quickly; others need a formal restructuring; a few need legal relief to stop the bleeding. The right move depends on whether the business is temporarily strained or structurally unable to pay. I think of the options this way: the earlier you negotiate, the more choices you keep.

| Option | Best when | Main tradeoff |

|---|---|---|

| Forbearance | The cash problem is temporary and the business can recover soon | No forgiveness; fees and interest may still build |

| Workout or restructuring | The business can repay on revised terms with lower pressure | The lender may ask for updated financials, tighter reporting, or added promises |

| Settlement | The lender wants a faster exit and you can raise cash for a lump-sum deal | The forgiven portion can create tax questions, and the credit damage usually remains |

| Bankruptcy | The debt load is too heavy and litigation risk is rising | Public, formal, and disruptive, but sometimes the cleanest legal reset |

A workout is usually the cleanest path if the company still has a real business model and a believable cash-flow plan. Settlement works better when the lender believes collection will be slow or expensive. Bankruptcy becomes more relevant when the debt is no longer the main issue and the business itself cannot absorb the pressure. The right choice is the one you can document, not the one you can only describe over the phone.

What to do in the first 48 hours after the default

The first two days matter because they shape the rest of the conversation. A lender is more likely to negotiate with a borrower who has a plan, a number, and a realistic proposal than with someone who is hoping the problem disappears on its own. I would handle it in this order:

- Read the note, the default clause, the guarantee, and the remedy section so you know exactly what was triggered.

- Calculate the arrears, late fees, default interest, and any other amounts the lender says are due now.

- Build a simple 8- to 13-week cash forecast so you know what you can actually pay.

- Send one written proposal instead of making scattered promises over the phone.

- If a lawsuit has started, treat the response deadline as non-negotiable.

- Do not sign a new guarantee, confession of judgment, or broad release until you understand what it does.

The point is not to be dramatic; the point is to keep the lender from defining the timeline for you. Once you know the numbers and the documents, you can start negotiating from facts instead of fear, and that changes the tone of the file quickly.

The two questions I would answer before paying a dollar more

The first question is whether the debt belongs only to the business or also to you personally. If you signed a guarantee, the business problem may become a household problem unless you treat it differently from the start. The second question is whether the lender is still open to a written workout or whether the file has already moved into litigation mode. That answer tells you whether you are negotiating payment terms or defending a legal claim.

My practical rule is simple: read the contract first, then talk about money. If the lender is willing to restructure, get every term in writing before you rely on it. If the debt is no longer salvageable, shift the goal from optimism to damage control, because the fastest way to make an unsecured business-loan default worse is to wait until the lender writes the next move for you.