Financial fraud investigations are rarely about a single suspicious transaction. They are about reconstructing the money trail, separating error from intent, and deciding whether a control failure, a policy breach, or deliberate deception sits behind the numbers. In the United States, that work sits at the intersection of legal risk, compliance design, and evidence preservation, so the first moves matter more than most teams expect. This article breaks down how the process unfolds, what evidence actually moves a case forward, and where strong controls change the outcome.

What matters most before the first interview

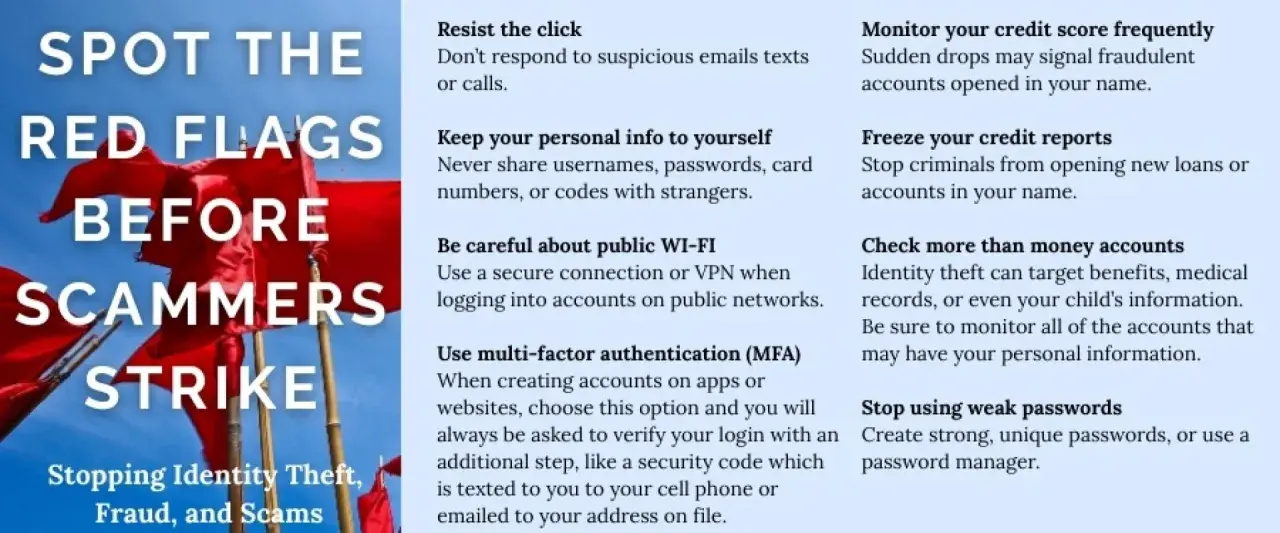

- Most cases start with a tip, audit exception, bank alert, or regulator referral, not with a confession.

- The first job is to preserve data and define scope before anyone starts “fixing” the story.

- The strongest cases usually combine accounting records, system logs, and communications, not just one type of proof.

- A credible compliance program can reduce losses, speed detection, and improve how a company is viewed if regulators get involved.

- In the latest ACFE report, 43% of frauds were detected through tips, and more than half of those tips came from employees.

- Not every suspicious matter becomes a criminal case; many end with remediation, restitution, discipline, or civil action.

What investigators are actually trying to prove

When I look at a suspected fraud matter, I usually start with three questions: what happened, who benefited, and which control failed. That sounds simple, but it keeps the case grounded. A lot of weak reviews get lost because the team jumps straight to blame before it can explain the mechanism.

In practice, the purpose is not only to confirm that money moved. It is to establish whether there was deception, whether the conduct was isolated or systemic, and whether the exposure is internal, regulatory, civil, or criminal. A clean internal mistake may call for a control fix and reimbursement. A deliberate scheme may require board-level escalation, forensic accounting, outside counsel, and possibly a referral to the SEC, DOJ, FBI, or state authorities.

I also find it useful to separate fact finding from legal theory. The facts come first. The legal label comes after the numbers, emails, approvals, and bank records line up. That order matters because a rushed theory can distort the evidence review and make the eventual report harder to defend. Once the objective is clear, the next step is to scope the matter before the evidence starts moving around.

How a case is usually opened and scoped

A good case does not begin with a dramatic interview. It begins with triage. Someone sees a red flag, an anomaly, or a complaint, and the organization has to decide whether the issue is a control gap, a bookkeeping error, or a real deception risk. In the United States, that early intake often comes from internal audit, finance, a whistleblower channel, a bank, a customer, or a regulator. The SEC’s enforcement manual, for example, shows how credible complaints and tips can be forwarded for deeper review and may open a matter under inquiry.

| Trigger | What it often signals | Immediate response |

|---|---|---|

| Tip or whistleblower report | Often the earliest and most useful signal, especially if the reporter has direct access to the process | Preserve evidence, protect identity, and avoid alerting the suspect too early |

| Audit exception | A control failure, cut-off problem, or hidden scheme inside routine activity | Reconcile the account, capture source documents, and trace the exception backward |

| Bank or card alert | Unusual transfers, account takeover activity, or unauthorized spending | Coordinate with the bank, stop further movement where lawful, and secure logs immediately |

| Vendor or customer complaint | Billing fraud, duplicate payment, ghost vendor activity, or delivery mismatch | Validate invoices, contracts, approvals, and shipment or service evidence |

| Regulator referral | Possible securities, lending, disclosure, or money-moving issues | Bring in counsel early and map all reporting obligations before interviews begin |

Once the trigger is understood, I narrow the scope fast: time period, legal entities, business units, systems, and the people who touched the transactions. That is also where privilege and chain of custody start to matter. If the team cannot show who collected a file, when it was copied, and whether it was altered, the file is a lead, not proof. That discipline becomes even more important once you move from scoping into the actual evidence trail.

The evidence trail that tends to move the case forward

Fraud cases are won or lost on details that look boring until they become decisive. The core question is simple: can you connect the transaction to the person, the purpose, and the benefit? That usually requires several layers of evidence, not just one spreadsheet.

| Evidence source | What it can show | Common weakness |

|---|---|---|

| General ledger and journal entries | Timing shifts, manual overrides, reclassifications, and unusual adjustments | Unsupported entries with no business explanation |

| Bank, wire, ACH, and card records | Where money actually went and whether it was split or redirected | Hidden intermediaries or mule accounts |

| Invoices, purchase orders, and contracts | Whether the payment had a legitimate business purpose | Mismatch between contract terms, vendor data, and payment approval |

| Email, chat, and calendar records | Coordination, intent, coaching, or concealment | Deleted threads or off-platform communications |

| Access logs and device data | Who touched the system, when, and from where | Shared credentials or gaps in logging |

| Payroll, HR, and expense data | Ghost employees, false reimbursements, and self-dealing | Weak onboarding, poor segregation of duties, or fake supporting documents |

| KYC, beneficial ownership, and crypto records | Identity trails and laundering paths | Layered accounts and hard-to-trace transfers |

The technical term that matters here is chain of custody, which is the record of how evidence was obtained, stored, transferred, and reviewed. If that chain is weak, the facts may still be useful, but the evidentiary value drops. This is also why investigation teams should avoid “cleaning up” records before capture. In my experience, preserving the mess is often more valuable than trying to produce a neat version of it. Once the evidence base is stable, the compliance picture becomes the next question.

Where compliance changes the outcome

Risk and compliance teams are not just there to react after a problem surfaces. They shape how likely the problem is to be found, how fast it is detected, and how credible the response looks if the matter reaches leadership or regulators. The DOJ’s updated guidance on corporate compliance programs is clear that there is no rigid formula. Prosecutors look at the company’s risk profile, size, industry, footprint, and controls, then ask three practical questions: is the program well designed, is it applied in good faith, and does it work in practice?

That framework is useful even if a case never leaves the company. A program that exists only on paper will not help much. A program that is actually used will. I pay close attention to risk assessment, segregation of duties, hotline design, training, monitoring, and how often management overrides the process. Those details often explain why a scheme ran for months.

The latest ACFE reporting gives a reason to take reporting channels seriously. It found that 43% of frauds were detected through tips, and more than half of those tips came from employees. That is not a minor statistic. It means the reporting culture is a real detection control, not a cosmetic feature. In a healthy program, a hotline is not just for HR disputes; it is one of the first lines of defense against financial misconduct.

When a matter does become serious, compliance also affects how the company is judged afterward. Voluntary self-disclosure, full cooperation, timely remediation, and proof that controls were tested and improved can materially change the conversation. That is why the best compliance teams think in terms of outcomes, not policy language. From there, the next step is recognizing the schemes and red flags most investigators actually see.

The schemes and red flags I see most often

Not every fraud case looks like a cinematic embezzlement. Many are repetitive, low-drama, and hidden in normal business flow. The patterns below show up often enough that I treat them as practical starting points, not theoretical categories.

| Scheme | Common red flags | What I would test first |

|---|---|---|

| Asset misappropriation | Missing receipts, round-dollar reimbursements, unusual access to cash, unexplained inventory shrinkage | Approve-to-pay workflow, receipt validation, physical counts, and duplicate payment testing |

| Billing fraud | Vendor master changes, same bank account across vendors, split invoices, pricing drift | Vendor onboarding records, tax IDs, bank details, and purchase order overrides |

| Payroll fraud | Ghost employees, address changes, bank account updates, overtime spikes | HR onboarding files, timekeeping logs, and authorization history |

| Financial statement fraud | Late entries, top-side adjustments, margin swings, aggressive estimates, missing support | Journal entry review, cutoff testing, and variance analysis |

| Corruption and kickbacks | Vendor concentration, unusual gifts, bid steering, conflict disclosure gaps | Procurement files, contract awards, email patterns, and related-party checks |

| Money laundering and account takeover | Rapid transfer chains, mule accounts, login anomalies, crypto hops, impersonation behavior | Transaction flow, IP and device data, KYC records, and beneficiary tracing |

Behavior matters too. In the ACFE’s latest report, 84% of fraudsters showed at least one behavioral red flag, such as financial troubles or living beyond their means. I treat that as a prompt, not proof. Lifestyle pressure does not equal guilt. But if the transactions already look strange, behavioral signals can help investigators decide where to focus first and who to interview next. The danger comes when teams confuse correlation with evidence, which leads directly to some very common mistakes.

Mistakes that weaken a good case

The biggest errors are usually procedural, not dramatic. They come from haste, politics, or the desire to “solve” the matter before the evidence is protected. I see the same failures repeatedly:

- Waiting too long to preserve email, chat, ERP, bank, and device data.

- Letting business leaders talk to witnesses before the scope is defined.

- Changing or “correcting” records before the original version is captured.

- Separating legal, compliance, finance, and HR into silos that do not share facts.

- Ignoring third-party records, especially bank data and vendor portal history.

- Using a narrative before the transaction map is complete.

- Assuming the first red flag is the whole story instead of a starting point.

The worst of these is usually the first one. If you do not preserve the trail, you may still suspect fraud, but you lose leverage. The rest of the process becomes more expensive, more fragile, and much harder to defend if the matter reaches a board committee, auditor, or regulator. That is why the first 48 hours matter so much.

The first 48 hours set the tone for the whole case

If I were brought into a live matter, I would focus on three things immediately: stop further loss, preserve evidence, and define the question. That means issuing a legal hold if appropriate, securing relevant systems, documenting access, and deciding who needs to know now versus later. The goal is not to build the perfect theory in a morning. It is to make sure the facts are still available when the theory is ready.

- Preserve records from email, chat, finance systems, shared drives, and mobile devices.

- Freeze access changes and admin privileges where the facts justify it.

- Assign one case owner so the investigation does not turn into a committee debate.

- Separate allegation review from disciplinary decisions until the facts are stable.

- Bring in outside counsel or forensic support if privilege, scale, or regulatory exposure is material.

By the time the first week ends, the organization should know what happened, what it still does not know, and whether the next step is remediation, referral, or both. That is the real value of a disciplined response: it turns a messy suspicion into a controlled process, and that is what protects both the balance sheet and the governance record.